Answered step by step

Verified Expert Solution

Question

1 Approved Answer

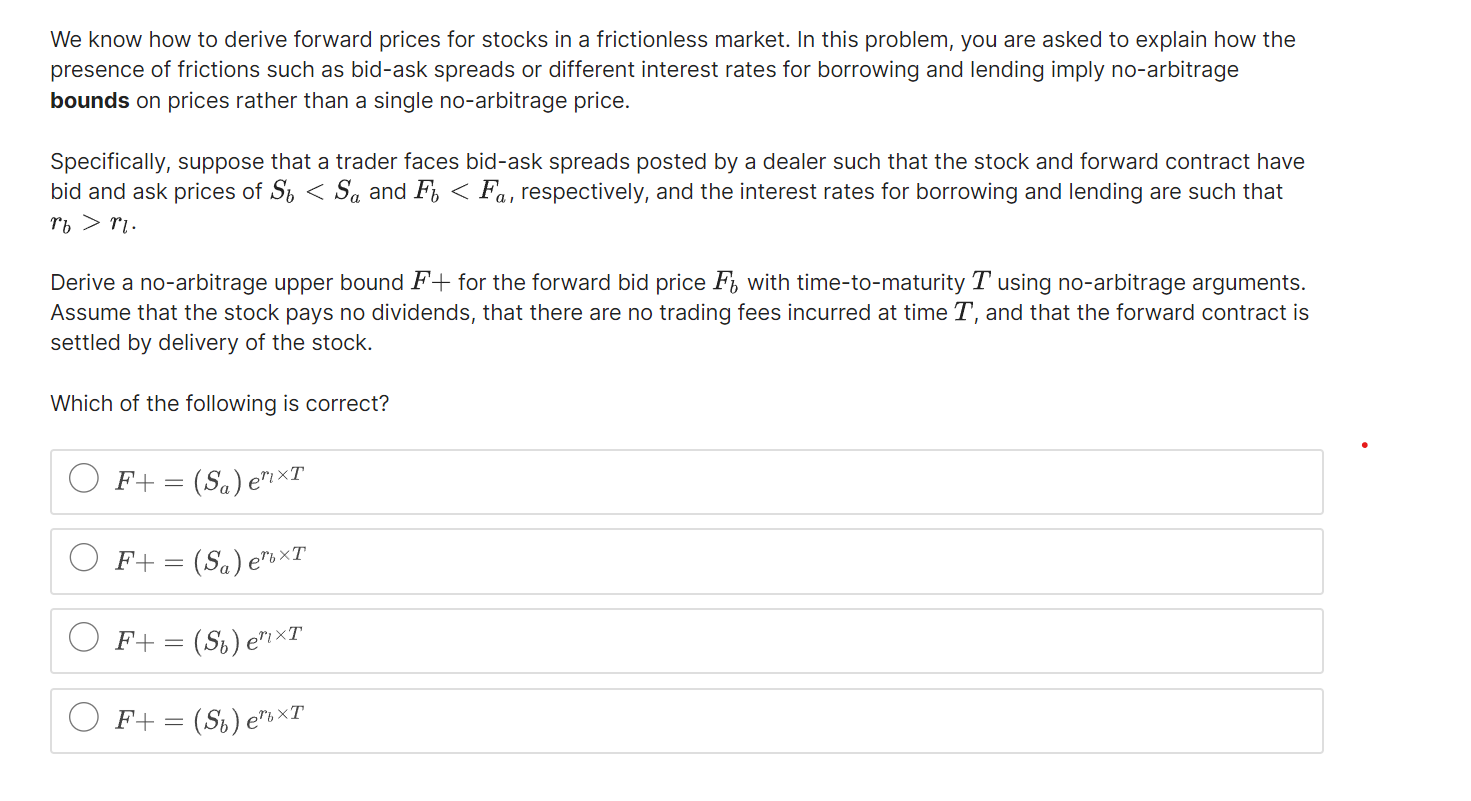

We know how to derive forward prices for stocks in a frictionless market. In this problem, you are asked to explain how the presence of

We know how to derive forward prices for stocks in a frictionless market. In this problem, you are asked to explain how the presence of frictions such as bid-ask spreads or different interest rates for borrowing and lending imply no-arbitrage bounds on prices rather than a single no-arbitrage price. Specifically, suppose that a trader faces bid-ask spreads posted by a dealer such that the stock and forward contract have bid and ask prices of Sb

We know how to derive forward prices for stocks in a frictionless market. In this problem, you are asked to explain how the presence of frictions such as bid-ask spreads or different interest rates for borrowing and lending imply no-arbitrage bounds on prices rather than a single no-arbitrage price. Specifically, suppose that a trader faces bid-ask spreads posted by a dealer such that the stock and forward contract have bid and ask prices of SbStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mortgage Ripoffs And Money Savers

Authors: Carolyn Warren

1st Edition

0470097833, 978-0470097830