Answered step by step

Verified Expert Solution

Question

1 Approved Answer

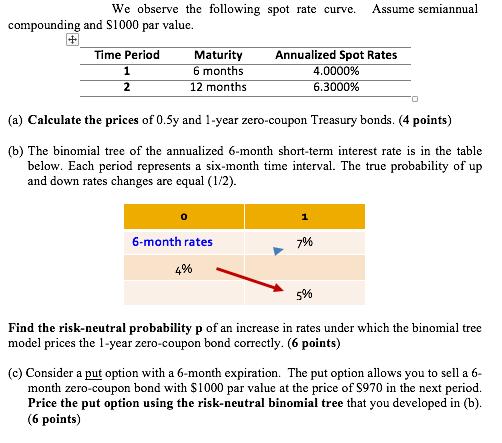

We observe the following spot rate curve. Assume semiannual compounding and $1000 par value. Time Period 1 2 Maturity 6 months 12 months (a)

We observe the following spot rate curve. Assume semiannual compounding and $1000 par value. Time Period 1 2 Maturity 6 months 12 months (a) Calculate the prices of 0.5y and 1-year zero-coupon Treasury bonds. (4 points) (b) The binomial tree of the annualized 6-month short-term interest rate is in the table below. Each period represents a six-month time interval. The true probability of up and down rates changes are equal (1/2). 6-month rates Annualized Spot Rates 4.0000% 6.3000% 4% 7% 5% Find the risk-neutral probability p of an increase in rates under which the binomial tree model prices the 1-year zero-coupon bond correctly. (6 points) (c) Consider a put option with a 6-month expiration. The put option allows you to sell a 6- month zero-coupon bond with $1000 par value at the price of $970 in the next period. Price the put option using the risk-neutral binomial tree that you developed in (b). (6 points)

Step by Step Solution

★★★★★

3.39 Rating (158 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Accounting

Authors: Susan S. Hamlen, Ronald J. Huefner, James A. Largay III

2nd edition

1934319309, 978-1934319307