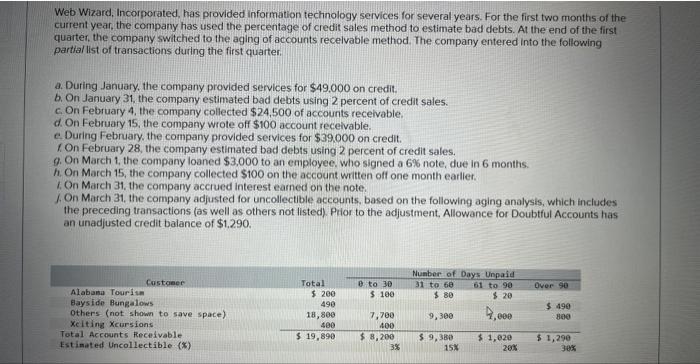

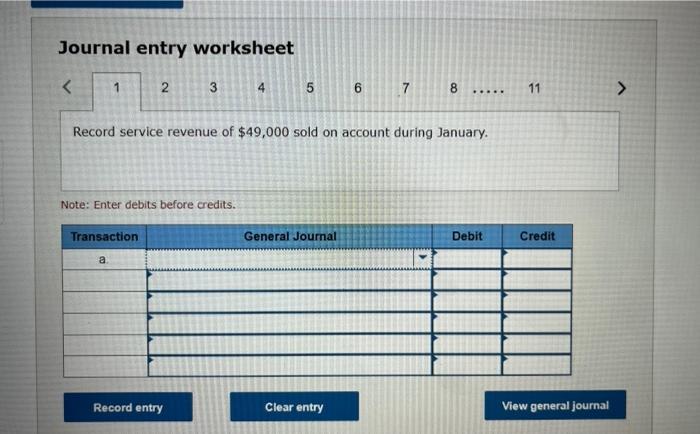

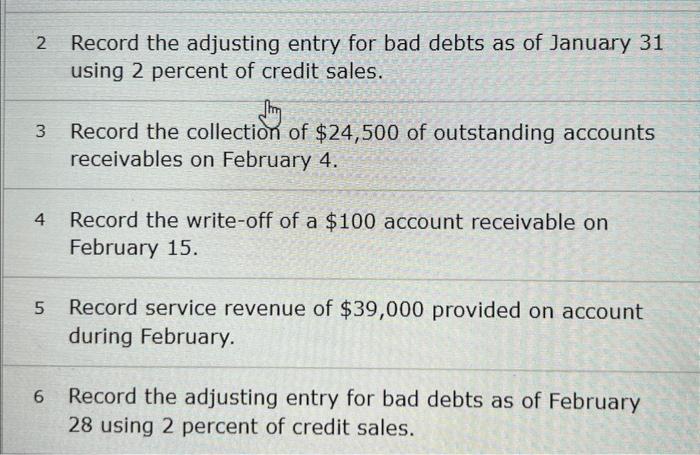

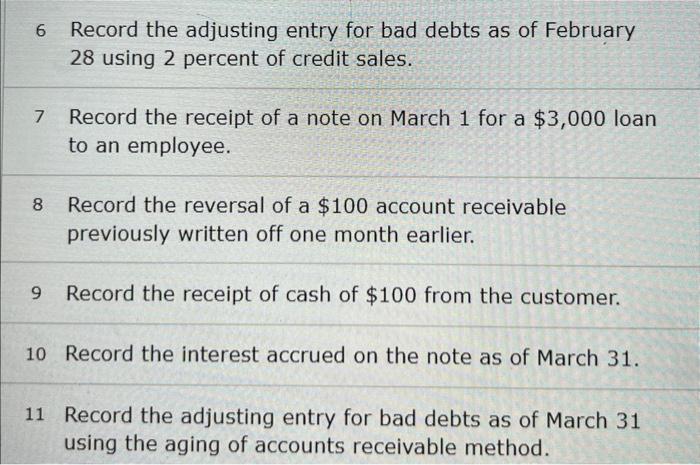

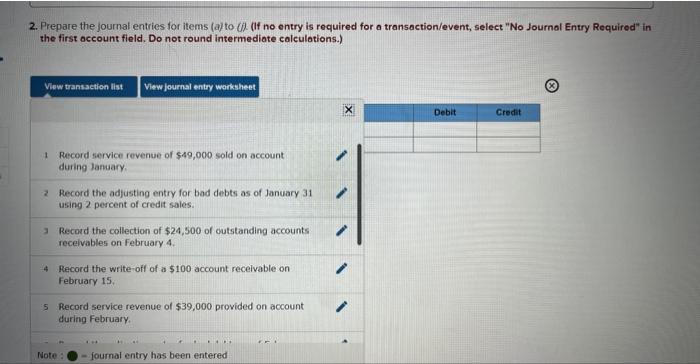

Web Wizard, Incorporated, has provided information technology services for several years. For the first two months of the current year, the company has used the percentage of credit sales method to estimate bad debts. At the end of the first quarter, the company switched to the aging of accounts recelvable method. The company entered into the following partial list of transactions during the first quarter. a. During January, the company provided services for $49.000 on credit. b. On January 31 , the company estimated bad debts using 2 percent of credit sales. c. On February 4 , the company collected $24,500 of accounts receivable. d. On February 15, the company wrote off $100 account recelvable. e. During February, the company provided services for $39.000 on credit. f. On February 28, the company estimated bad debts using 2 percent of credit sales. 9. On March 1, the company loaned $3,000 to an employee, who signed a 6% note, due in 6 months. h. On March 15, the company collected $100 on the account written off one month earller. 1. On March 31, the company accrued interest earned on the note. f. On March 31, the company adjusted for uncollectible accounts, based on the following aging analysis, which includes the preceding transactions (as well as others not listed). Pior to the adjustment, Allowance for Doubtful Accounts has an unadjusted credit balance of $1,290. Journal entry worksheet 7 Record service revenue of $49,000 sold on account during January. Note: Enter debits before credits. 2 Record the adjusting entry for bad debts as of January 31 using 2 percent of credit sales. 3 Record the collection of $24,500 of outstanding accounts receivables on February 4. 4 Record the write-off of a $100 account receivable on February 15. 5 Record service revenue of $39,000 provided on account during February. 6 Record the adjusting entry for bad debts as of February 28 using 2 percent of credit sales. 6 Record the adjusting entry for bad debts as of February 28 using 2 percent of credit sales. 7 Record the receipt of a note on March 1 for a $3,000 loan to an employee. 8 Record the reversal of a $100 account receivable previously written off one month earlier. 9 Record the receipt of cash of $100 from the customer. 10 Record the interest accrued on the note as of March 31. 11 Record the adjusting entry for bad debts as of March 31 using the aging of accounts receivable method. 2. Prepare the journal entries for items (a) to (i) (If no entry is required for a transaction/event, select "No Journol Entry Required" in the first account field. Do not round intermediate calculations.) 1 Record service revenue of $49,000 sold on account during January. 2 Record the adjusting entry for bad debts as of January 31 using 2 percent of credit sales. 3 Record the collection of $24,500 of cutstanding accounts receivables on February 4. 4. Record the write-off of a $100 account recelvable on February 15. 5 Record service revenue of $39,000 provided on account during February