Answered step by step

Verified Expert Solution

Question

1 Approved Answer

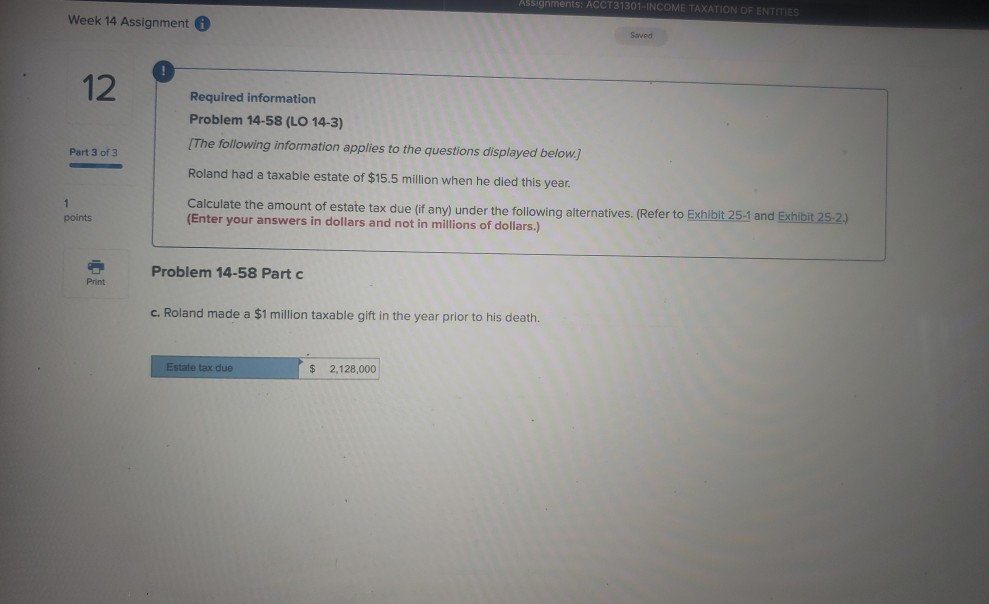

Week 14 Assignment Required information Problem 14-58 (LO 14-3) (The following information applies to the questions displayed below. Part 2 of 3 Roland had a

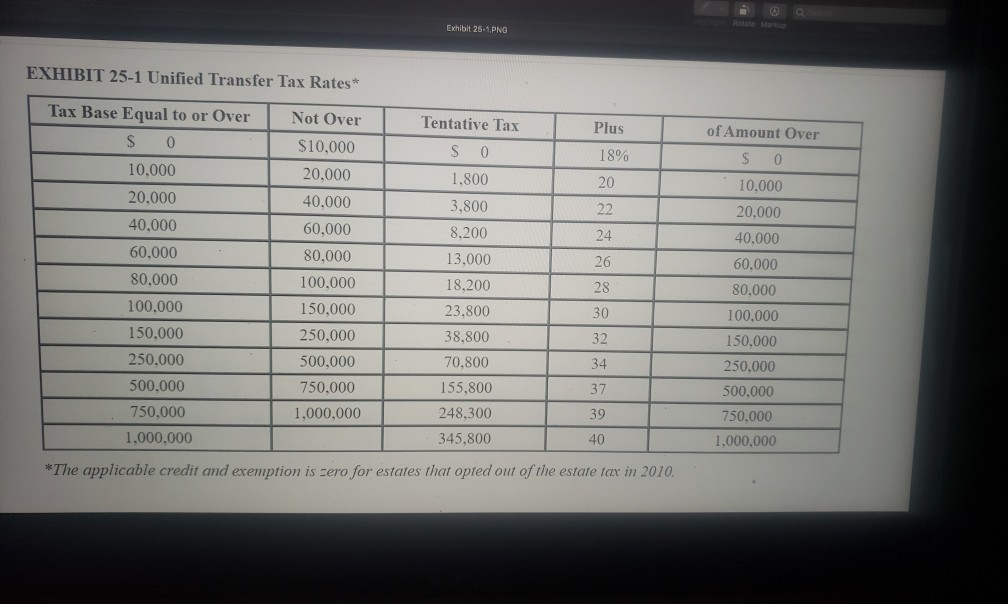

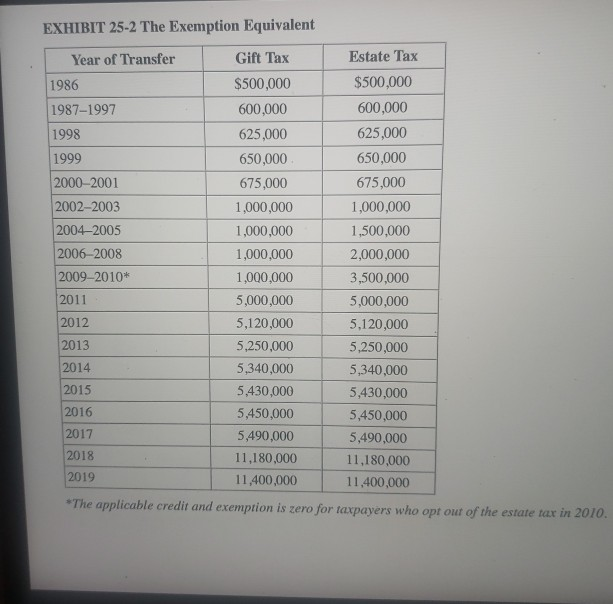

Week 14 Assignment Required information Problem 14-58 (LO 14-3) (The following information applies to the questions displayed below. Part 2 of 3 Roland had a taxable estate of $15.5 million when he died this year. Calculate the amount of estate tax due (if any) under the following alternatives. (Refer to Exhibit 25:1 and Exhibit 25-2) (Enter your answers in dollars and not in millions of dollars.) points Sipped Problem 14-58 Part b b. Roland's prior taxable gifts consist of a taxable gift of $1.5 million in 2005. Estate tax due Assignments: ACC131301-INCOME TAXATION OF ENTITIES Week 14 Assignment Saved 12 Required information Problem 14-58 (LO 14-3) The following information applies to the questions displayed below.) Part 3 of 3 Roland had a taxable estate of $15.5 million when he died this year. Calculate the amount of estate tax due (if any) under the following alternatives. (Refer to Exhibit 25-1 and Exhibit 25-2) (Enter your answers in dollars and not in millions of dollars.) points Problem 14-58 Part Print c. Roland made a $1 million taxable gift in the year prior to his death. Estate tax due $ 2,128,000 HEM Exhibit 25-1.PNG EXHIBIT 25-1 Unified Transfer Tax Rates* Tax Base Equal to or Over S 0 10.000 20.000 40,000 60.000 80.000 100,000 150,000 250,000 500.000 750,000 1,000,000 Not Over $10,000 20.000 40,000 60,000 80.000 100.000 150,000 250,000 500,000 750,000 1,000,000 Plus 18% 20 22 24 26 Tentative Tax S 0 1.800 3,800 8,200 13,000 18,200 23,800 38,800 70,800 155,800 248,300 345,800 of Amount Over $ 0 10,000 20,000 40,000 60,000 80,000 100.000 150,000 250.000 500,000 750,000 1,000,000 30 34 37 39 40 *The applicable credit and exemption is zero for estates that opted out of the estate tax in 2010. EXHIBIT 25-2 The Exemption Equivalent Year of Transfer Gift Tax 1986 $500,000 1987-1997 600,000 1998 625,000 1999 650,000 2000-2001 675,000 2002-2003 1,000,000 2004-2005 1,000,000 2006-2008 1,000,000 2009-2010* 1,000,000 2011 5,000,000 2012 5,120,000 5,250,000 2014 5,340,000 5,430,000 2016 5,450,000 2017 5,490,000 2018 11,180,000 2019 11,400,000 Estate Tax $500,000 600,000 625,000 650,000 675,000 1,000,000 1,500,000 2,000,000 3,500,000 5,000,000 5,120,000 5,250,000 5,340,000 5,430,000 5,450,000 5,490,000 11,180,000 11,400,000 2013 2015 *The applicable credit and exemption is zero for taxpayers who opt out of the estate tax in 2010. Week 14 Assignment Required information Problem 14-58 (LO 14-3) (The following information applies to the questions displayed below. Part 2 of 3 Roland had a taxable estate of $15.5 million when he died this year. Calculate the amount of estate tax due (if any) under the following alternatives. (Refer to Exhibit 25:1 and Exhibit 25-2) (Enter your answers in dollars and not in millions of dollars.) points Sipped Problem 14-58 Part b b. Roland's prior taxable gifts consist of a taxable gift of $1.5 million in 2005. Estate tax due Assignments: ACC131301-INCOME TAXATION OF ENTITIES Week 14 Assignment Saved 12 Required information Problem 14-58 (LO 14-3) The following information applies to the questions displayed below.) Part 3 of 3 Roland had a taxable estate of $15.5 million when he died this year. Calculate the amount of estate tax due (if any) under the following alternatives. (Refer to Exhibit 25-1 and Exhibit 25-2) (Enter your answers in dollars and not in millions of dollars.) points Problem 14-58 Part Print c. Roland made a $1 million taxable gift in the year prior to his death. Estate tax due $ 2,128,000 HEM Exhibit 25-1.PNG EXHIBIT 25-1 Unified Transfer Tax Rates* Tax Base Equal to or Over S 0 10.000 20.000 40,000 60.000 80.000 100,000 150,000 250,000 500.000 750,000 1,000,000 Not Over $10,000 20.000 40,000 60,000 80.000 100.000 150,000 250,000 500,000 750,000 1,000,000 Plus 18% 20 22 24 26 Tentative Tax S 0 1.800 3,800 8,200 13,000 18,200 23,800 38,800 70,800 155,800 248,300 345,800 of Amount Over $ 0 10,000 20,000 40,000 60,000 80,000 100.000 150,000 250.000 500,000 750,000 1,000,000 30 34 37 39 40 *The applicable credit and exemption is zero for estates that opted out of the estate tax in 2010. EXHIBIT 25-2 The Exemption Equivalent Year of Transfer Gift Tax 1986 $500,000 1987-1997 600,000 1998 625,000 1999 650,000 2000-2001 675,000 2002-2003 1,000,000 2004-2005 1,000,000 2006-2008 1,000,000 2009-2010* 1,000,000 2011 5,000,000 2012 5,120,000 5,250,000 2014 5,340,000 5,430,000 2016 5,450,000 2017 5,490,000 2018 11,180,000 2019 11,400,000 Estate Tax $500,000 600,000 625,000 650,000 675,000 1,000,000 1,500,000 2,000,000 3,500,000 5,000,000 5,120,000 5,250,000 5,340,000 5,430,000 5,450,000 5,490,000 11,180,000 11,400,000 2013 2015 *The applicable credit and exemption is zero for taxpayers who opt out of the estate tax in 2010

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Security Audit And Control Features SAP ERP

Authors: Isaca

4th Edition

1604205806, 978-1604205800