Answered step by step

Verified Expert Solution

Question

1 Approved Answer

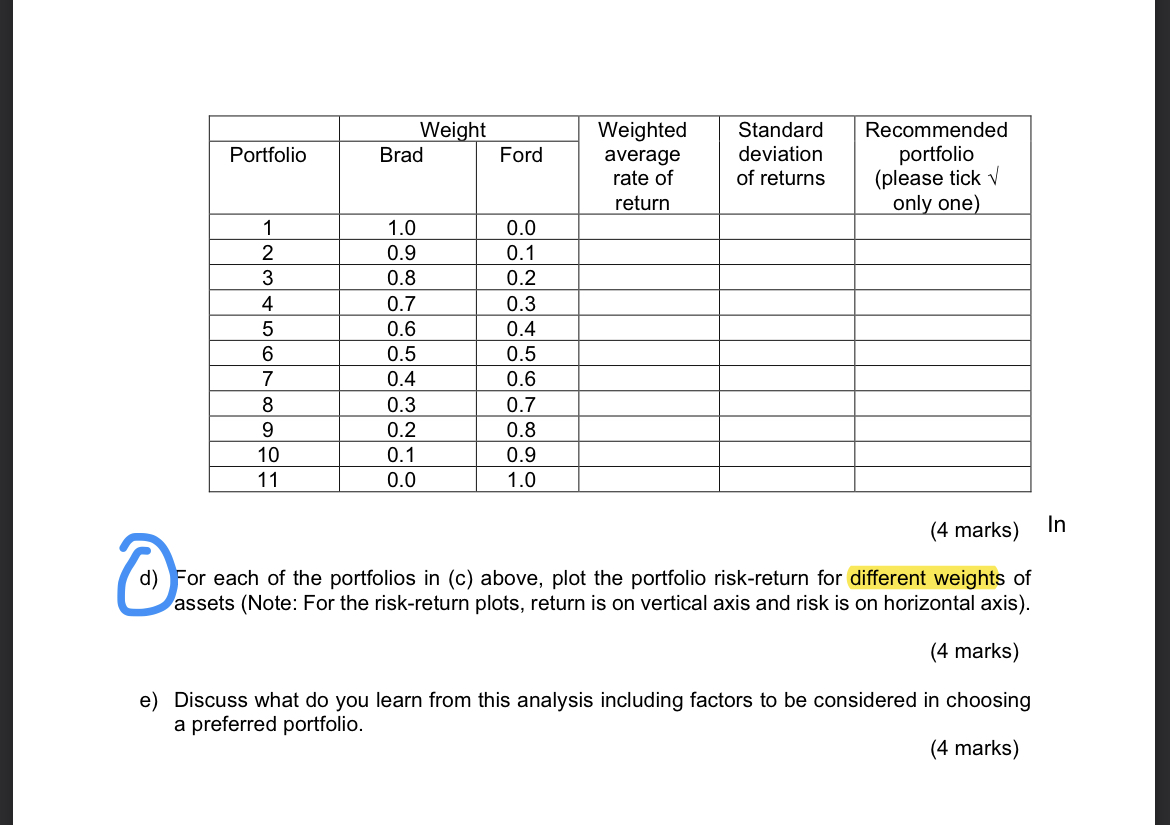

Weig hted Standard Recommended Portfolio Brad Ford average deviation portfolio rate of of returns (please tick 1! return only one) 1 1.0 0.0 | 2

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Strategic Management

Authors: Richard Lynch , Oliver Barish Barish , Vinh Sum Chau , Charles Thornton , Karl S. R. Warner

10th Edition

1529672554, 978-1529672558