Question

Weston Corporation manufactures auto parts for two leading Japanese automakers. Nancy Evans is the management accountant for one of Weston's largest manufacturing plants. The plant's

Weston Corporation manufactures auto parts for two leading Japanese automakers. Nancy Evans is the management accountant for one of Weston's largest manufacturing plants. The plant's general manager, Chris Sheldon, has just returned from a meeting at corporate headquarters where quality expectations were outlined for 2014. Chris calls Nancy into his office to relay the corporate quality objectives that total quality costs will not exceed 10% of total revenues by plant under any circumstances. Chris asks Nancy to provide him with a list of options for meeting corporate headquarters' quality objective. The plant's initial budgeted revenues and quality costs for 2014 are as follows:

| Revenue | 5,100,000 |

| Quality costs: | |

| Testing of purchased materials | 48,000 |

| Quality control training for production staff | 7,500 |

| Warranty repairs | 123,000 |

| Quality design engineering | 72,000 |

| Customer support | 55,500 |

| Materials scrap | 18,000 |

| Product inspection | 153,000 |

| Engineering redesign of failed parts | 31,500 |

| Rework of failed parts | 27,000 |

Prior to receiving the new corporate quality objective, Nancy had collected information for all the plant's possible options for improving both product quality and costs of quality. She was planning to introduce the idea of reengineering the manufacturing process at a one-time cost of $112,500, which would decrease product inspection costs by approximately 25% per year and was expected to reduce warranty repairs and customer support by an estimated 40% per year. After seeing the new corporation objective, Nnancy is reconsidering the reengineeing idea.

Nancy returns to her office and crunches the numbers again to look for other alternatives. She concludes that by increasing the cost of quality control traning for production staff by $22,500 per year, the company would reduce inspection costs by 10% annually and reduce warranty repairs and customer support costs by 20% per year as well. She is leaning towards only presenting this latter option to Chris because this is the only option that meets the new corporate quality objective.

Requirement 1 is given: categorize the quality costs into the four categories; prevention costs, appraisal costs, internal failure costs, and external failure costs. Prepare an Excel worksheet which, for each category, computes the ratio of budgeted costs to budgeted revenues for 2014. Indicate whether the quality costs meet the quality cost objective.

SHOW ALL WORK AND PROVIDE CORRECT ACCOUNTING FORMAT!!

1.) Requirement 2: prepare an Excel worksheet that shows the two-year outcome for each of the options. Your worksheet should be in good form with explanatory notes.

2.) Requirement 3: discuss the IMA Statement of Ethical Professional Practice regarding the disclosure of both alternatives to Chris Sheldon, specifically addressing the qualities of competence and credibility.

3.) Prepare a memo from Nancy to Chris in good form outlining her work on the two options and discussing the advantages and disadvantages of each option. Include an explanation from Nancy about why she is including discussion of the option to re-engineer the manufacturing process even though this option does not meet the quality objective set by management. Include as attachments to your memo your worksheets for requirements 1 and 2.

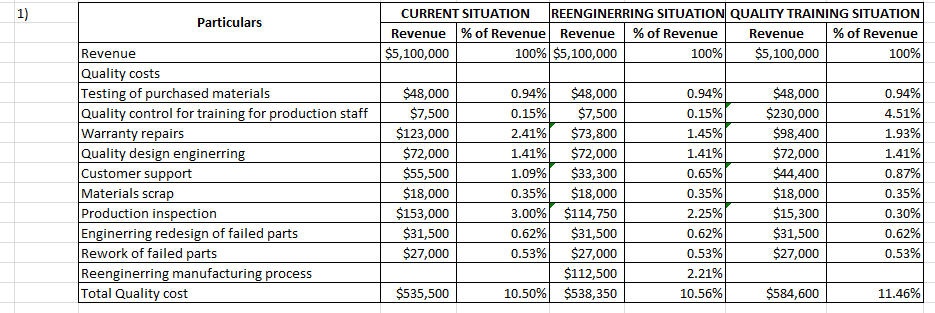

CURRENT SITUATION REENGINERRING SITUATION QUALITY TRAINING SITUATION Particulars Revenue of Revenue Revenue 9% of Revenue Revenue 9% of Revenue 100% 100,000 100% $5,100,000 100%, $5,100,000 Revenue Quality costs S48,000 0.94% $48,000 0.94% SA8,000 0.94% Testing of purchased materials S,500 0.15% S7500 0.15%r $230,000 4.51% Quality control for training for production staff 241% S73800 1.45% S98400 1.93% $123,000 Warranty repairs 1.41% $72,000 1.41% $72,000 1.41% $72,000 Quality design enginerring 1.09% SE 3300 0.65% S44400 0.876 $55,500 Customer support 0.35% S18,000 0.35% $18,000 035% $18,000 Materials scrap $153,000 3.00% $114,750 Production inspection 02% $31,500 $31,500 $31,500 Enginerring redesign of failed parts 23% $27,000 0.53% $27,000 0.53% $27,000 Rework of failed parts 2.21%I $112,500 Reenginerring manufacturing process Total Quality cost $535.500 10.50% $538,350 10.56% $584,600 11.46%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Level Audit Q And A 2014

Authors: ACA Simplified

1st Edition

1500852538, 978-1500852535