Question

What are the book to tax differences for the below listed partnership? Also, complete Form 1065. General Information August Easter and Grace Jackson own Notorious

What are the book to tax differences for the below listed partnership? Also, complete Form 1065.

General Information

August Easter and Grace Jackson own Notorious B.B.Q. (NB), a limited partnership. NB sells a variety of rubs, sauces, and accessories for grilling and smoking meat. NB was formed on August 18, 2019 and operates out of Kansas City, Missouri. August is a general partner, manages the operations of the business, and holds 60% profits, loss, and capital interests. Grace is a limited partner, is as an investor only, and holds the remaining 40% profits, loss, and capital interests.

Following is additional information related to NB:

- Office Location: 543 BBQ Lane, Kansas City, MO 64119

- Employer Identification Number: 99-8888777

- Business activity code: 445290

- Augusts address and social security number: 123 Ribs Lane, Kansas City, MO 64158, and his social security number is 123-12-1234.

- Graces address is 789 Brisket Ave., Kansas City, MO 64114, and her social security number is 987-98-9876.

- August is the partnership representative, and his phone number is (816) 100-1000.

Financial Information

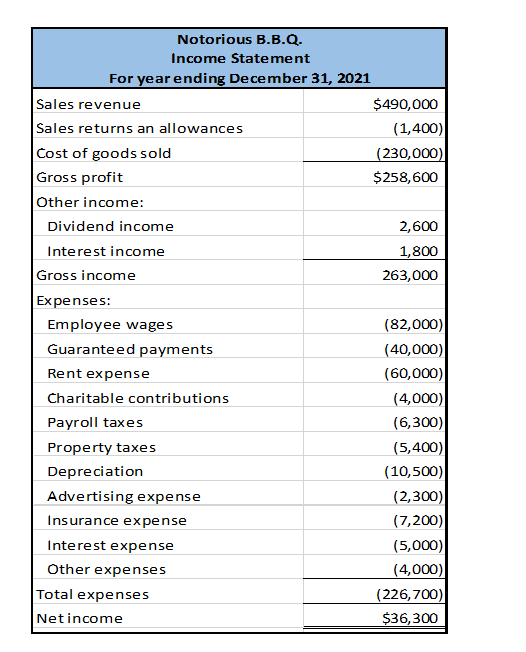

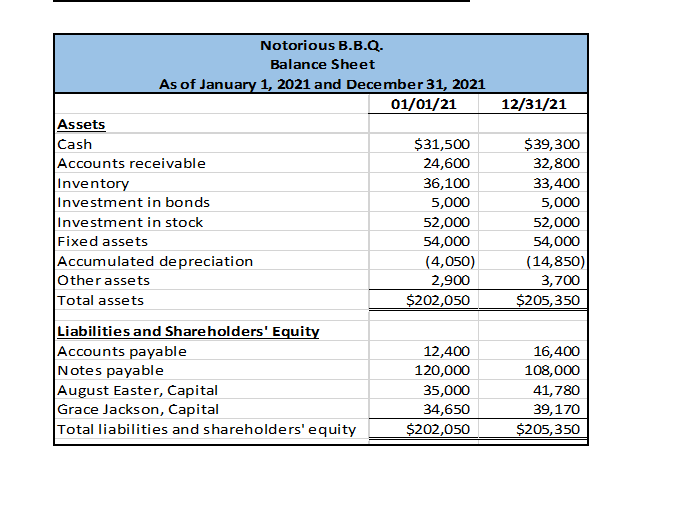

Following is pertinent information related to NBs financial activities in 2021:

- NB uses the accrual method of accounting and has a calendar year-end.

- income, $300 was from a Kansas City bond and $1,500 was from a bank account.

- All guaranteed payments were made to August for services provided to the partnership.

- On December 15, 2021, NB distributed $15,000 to August and $10,000 to Grace.

- The charitable contribution made during the year was paid in cash.

- The $5,000 interest expense was related to the notes payable. The note payable is a business loan and is nonrecourse debt. (Note: The debt is NOT qualified nonrecourse financing.)

- Included in the other expenses amount was a property tax penalty in the amount of $540 that was assessed when NB failed to pay its property tax on time.

- The partnership uses the FIFO inventory method and values its inventory at lower of cost or market. In addition, UNICAP rules of 263A do not apply and there was no change in determining quantities, cost, or valuations between opening and closing inventory.

- August, as general partner, is legally responsible for paying NBs accounts payable if the partnership fails to do so.

- NB did not have any current year fixed asset purchases. In 2019 and 2020, all fixed assets purchased were fully depreciated using bonus depreciation.

- For the purposes of the Qualified Business Income Deduction, the unadjusted basis of qualified property immediately after acquisition is $54,000.

- Assume that NB did not make any payments that would require it to file Form(s) 1099

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting principles and analysis

Authors: Terry d. Warfield, jerry j. weygandt, Donald e. kieso

2nd Edition

471737933, 978-0471737933