WHAT IS PART C ??? PLEASE HELP ME

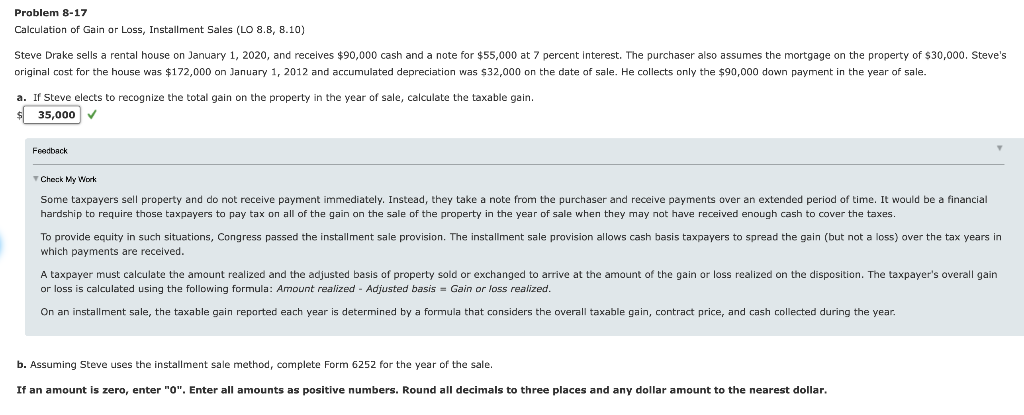

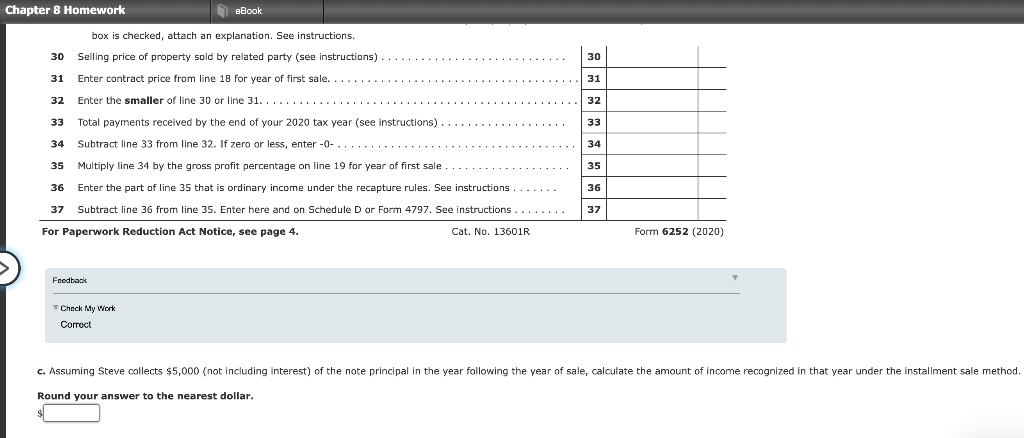

Problem 8-17 Calculation of Gain - Loss, Installment Sales (LO 8.8, 8.10) Steve Drake sells a rental house on January 1, 2020, and receives $90,000 cash and a note for $55,000 at 7 percent interest. The purchaser also assumes the mortgage on the property of $30,000. Steve's original cost for the house was $172,000 on January 1, 2012 and accumulated depreciation was $32,000 on the date of sale. He collects only the $90,000 down payment in the year of sale. a. If Steve elects to recognize the total gain on the property in the year of sale, calculate the taxable gain. $ 35,000 Feedback Check My Work Some taxpayers sell property and do not receive payment immediately. Instead, they take a note from the purchaser and receive payments over an extended period of time. It would be a financial hardship to require those taxpayers to pay tax on all of the gain on the sale of the property in the year of sale when they may not have received enough cash to cover the taxes. To provide equity in such situations, Congress passed the installment sale provision. The installment sale provision allows cash basis taxpayers to spread the gain (but not a loss) over the tax years in which payments are received. A taxpayer must calculate the amount realized and the adjusted basis of property sold or exchanged to arrive at the amount of the gain or loss realized on the disposition. The taxpayer's overall gain or loss is calculated using the following formula: Amount realized - Adjusted basis = Gain or loss realized. On an installment sale, the taxable gain reported each year is determined by a formula that considers the overall taxable gain, contract price, and cash collected during the year. b. Assuming Steve uses the installment sale method, complete Form 6252 for the year of the sale. If an amount is zero, enter "O". Enter all amounts as positive numbers. Round all decimals to three places and any dollar amount to the nearest dollar. Chapter 8 Homework eBook box is checked, attach an explanation. See instructions. 30 Selling price of property sold by related party (see instructions) 31 Enter contract price from line 18 for year of first sale. 30 31 32 Enter the smaller of line 30 or line 31. ... 32 33 Total payments received by the end of your 2020 tax year (see instructions). 33 34 Subtract line 33 from line 32. If zero or less, enter -0- 34 35 36 35 Multiply line 34 by the gross profit percentage on line 19 for year of first sale.... 36 Enter the part of line 35 that is ordinary income under the recapture rules. See instructions .... 37 Subtract line 36 from line 35. Enter here and on Schedule D or Form 4797. See instructions ........ For Paperwork Reduction Act Notice, see page 4. Cat. No. 13601R 37 Form 6252 (2020) Feedback Check My Work Correct C. Assuming Steve collects $5,000 (not including interest) of the note principal in the year following the year of sale, calculate the amount of income recognized in that year under the installment sale method, Round your answer to the nearest dollar