Answered step by step

Verified Expert Solution

Question

1 Approved Answer

What must be done mathematically to compute and get the dollar amounts for Manufacturing costs, Other Operating costs, and Operating income representing both April and

What must be done mathematically to compute and get the dollar amounts for Manufacturing costs, Other Operating costs, and Operating income representing both April and May

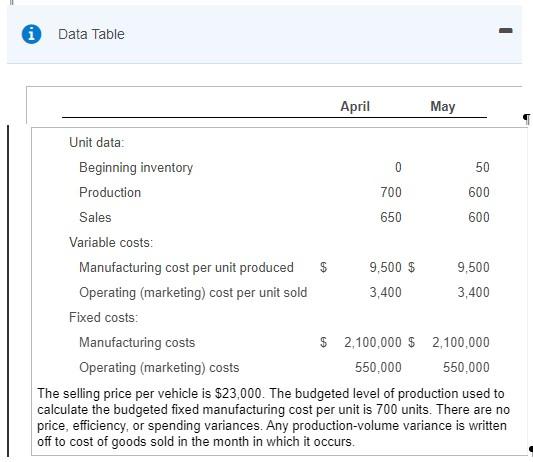

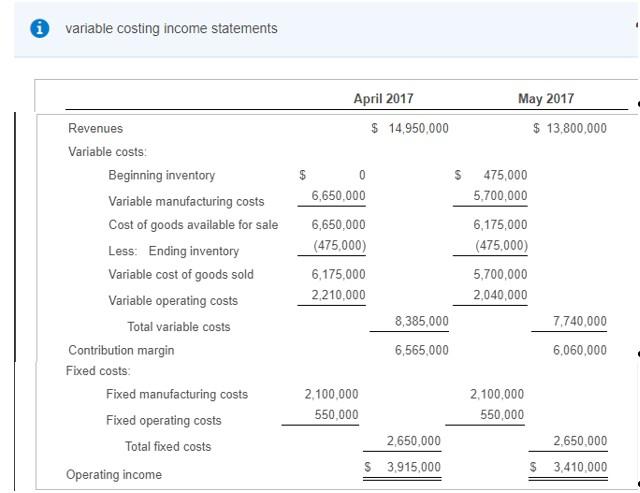

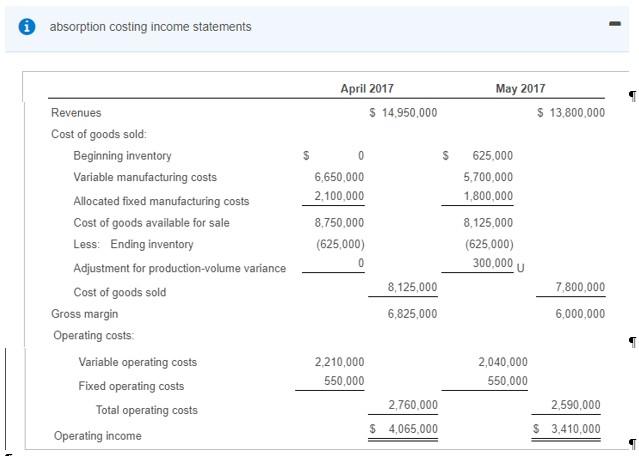

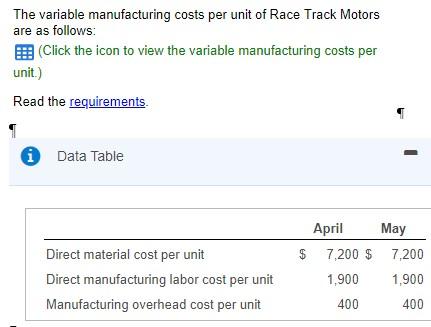

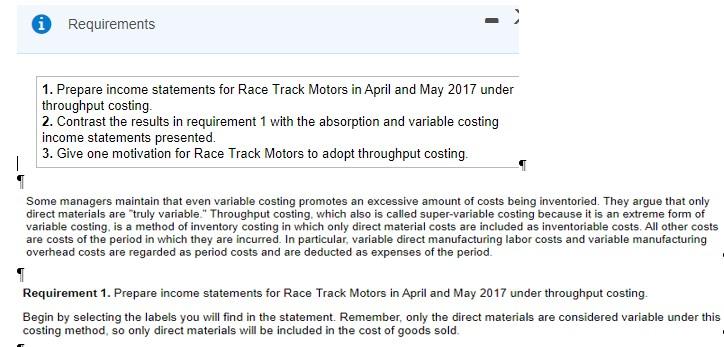

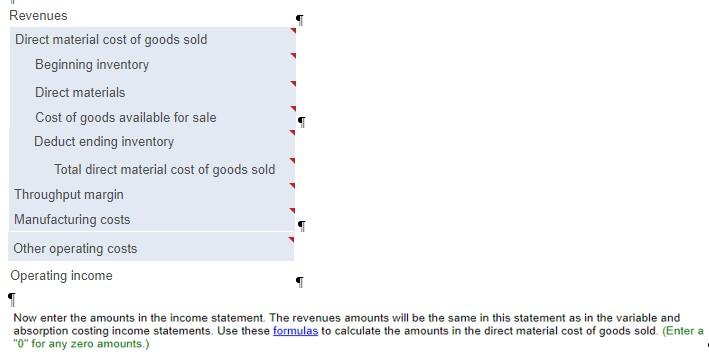

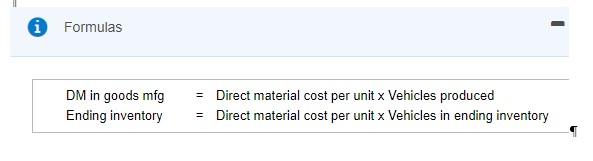

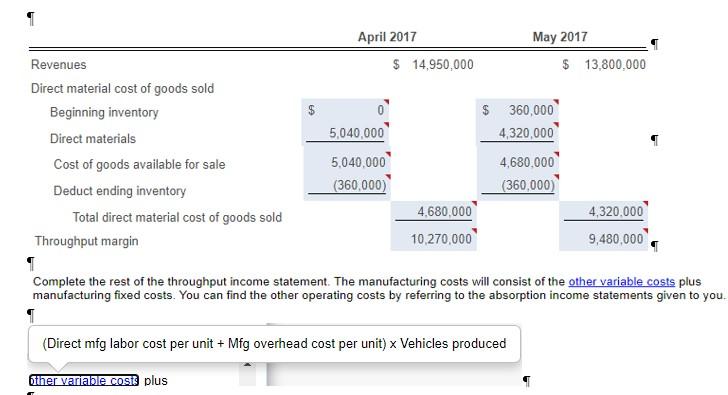

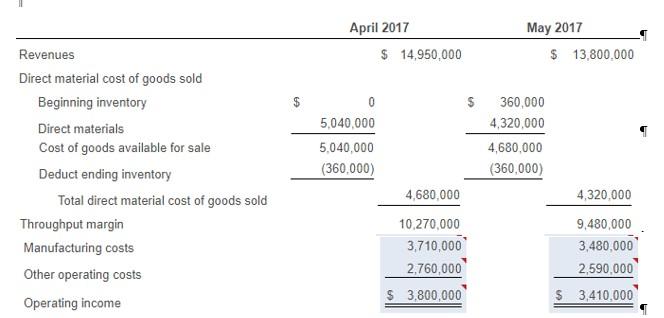

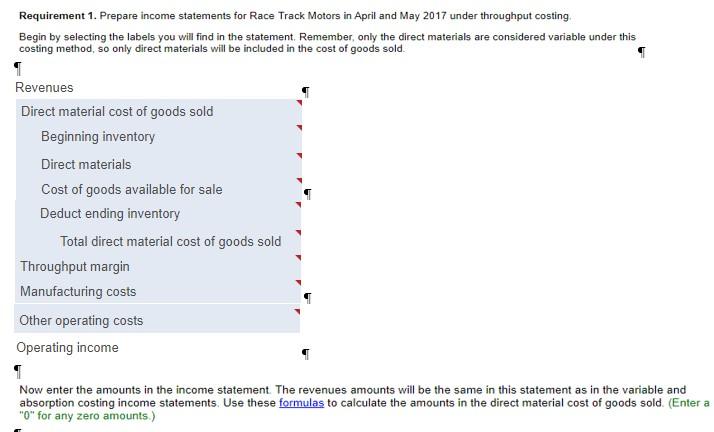

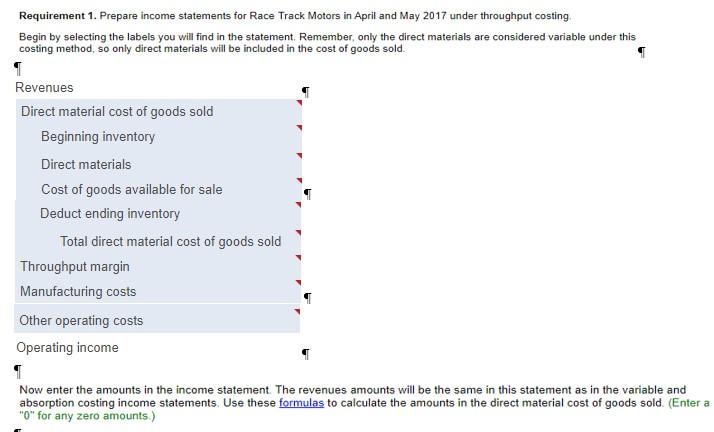

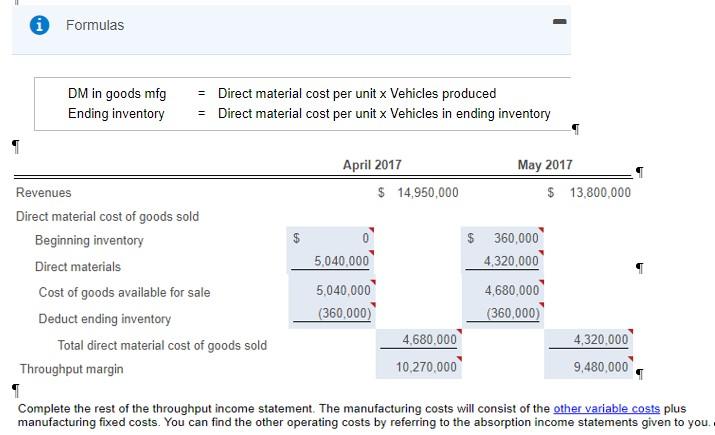

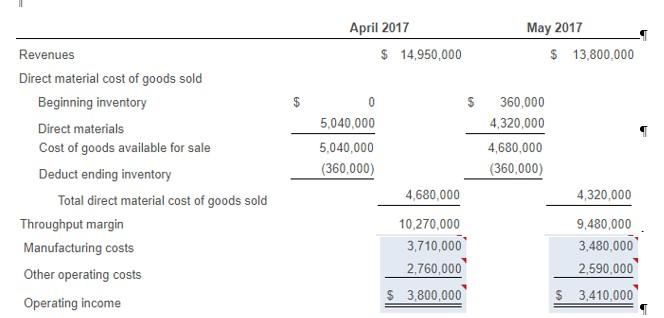

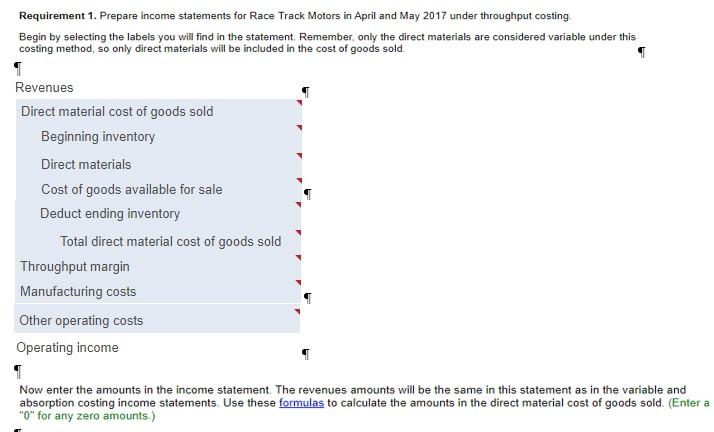

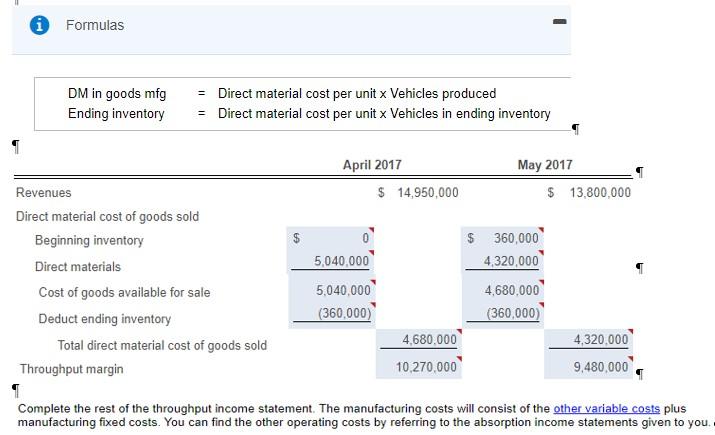

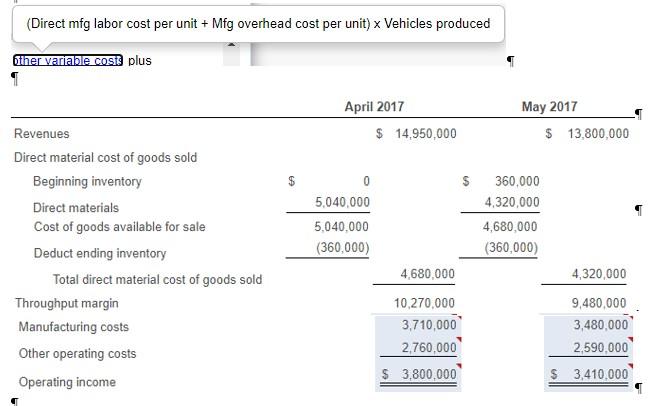

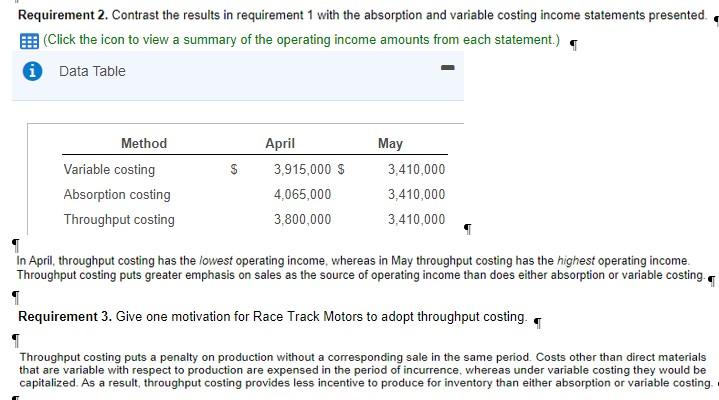

E9-22 (similar to), Race Track Motors assembles and sells motor vehicles and uses standard costing. Actual data and variable costing and absorption costing income statements relating to April and May 2017 are as follows: (Click the icon to view the data.) (Click the icon to view the variable costing income B Click the icon to view the absorption costing income statements.) i Data Table - April May Unit data: Beginning inventory 0 50 Production 700 600 Sales 650 600 Variable costs: Manufacturing cost per unit produced $ 9.500 $ 9,500 Operating (marketing) cost per unit sold 3,400 3,400 Fixed costs: Manufacturing costs $ 2,100,000 $ 2,100,000 Operating (marketing) costs 550,000 550,000 The selling price per vehicle is $23,000. The budgeted level of production used to calculate the budgeted fixed manufacturing cost per unit is 700 units. There are no price, efficiency, or spending variances. Any production-volume variance is written off to cost of goods sold in the month in which it occurs. variable costing income statements April 2017 May 2017 $ 14,950,000 $ 13,800,000 $ $ 0 6,650,000 6,650,000 (475,000) 6.175,000 2.210,000 475,000 5,700,000 6,175,000 (475.000) 5,700,000 2,040,000 Revenues Variable costs: Beginning inventory Variable manufacturing costs Cost of goods available for sale Less: Ending inventory Variable cost of goods sold Variable operating costs Total variable costs Contribution margin Fixed costs Fixed manufacturing costs Fixed operating costs Total fixed costs Operating income 8,385,000 7,740,000 6,565,000 6,060,000 2,100,000 550,000 2,100,000 550,000 2,650,000 2.650,000 $ 3.915,000 $ 3,410,000 i absorption costing income statements April 2017 $ 14,950,000 May 2017 $ 13,800,000 $ 0 6,650,000 2,100,000 8.750,000 (625,000) 0 625,000 5,700,000 1,800,000 8,125,000 (625,000) 300,000 Revenues Cost of goods sold Beginning inventory Variable manufacturing costs Allocated fixed manufacturing costs Cost of goods available for sale Less: Ending inventory Adjustment for production-volume variance Cost of goods sold Gross margin Operating costs Variable operating costs Fixed operating costs Total operating costs Operating income 8,125,000 6,825,000 7,800,000 6,000,000 2.210,000 550,000 2,760,000 $ 4,065,000 2,040,000 550.000 2,590,000 $ 3,410,000 The variable manufacturing costs per unit of Race Track Motors are as follows: B (Click the icon to view the variable manufacturing costs per unit.) Read the requirements Data Table Direct material cost per unit Direct manufacturing labor cost per unit Manufacturing overhead cost per unit April May $ 7,200 $ 7,200 1,900 1,900 400 400 Requirements 1. Prepare income statements for Race Track Motors in April and May 2017 under throughput costing. 2. Contrast the results in requirement 1 with the absorption and variable costing income statements presented. 3. Give one motivation for Race Track Motors to adopt throughput costing. Some managers maintain that even variable costing promotes an excessive amount of costs being inventoried. They argue that only direct materials are truly variable" Throughput costing, which also is called super-variable costing because it is an extreme form of variable costing, is a method of inventory costing in which only direct material costs are included as inventoriable costs. All other costs are costs of the period in which they are incurred. In particular, variable direct manufacturing labor costs and variable manufacturing overhead costs are regarded as period costs and are deducted as expenses of the period. Requirement 1. Prepare income statements for Race Track Motors in April and May 2017 under throughput costing Begin by selecting the labels you will find in the statement. Remember, only the direct materials are considered variable under this costing method so only direct materials will be included in the cost of goods sold. Revenues Direct material cost of goods sold Beginning inventory Direct materials Cost of goods available for sale Deduct ending inventory Total direct material cost of goods sold Throughput margin Manufacturing costs Other operating costs Operating income Now enter the amounts in the income statement. The revenues amounts will be the same in this statement as in the variable and absorption costing income statements. Use these formulas to calculate the amounts in the direct material cost of goods sold (Enter a "O" for any zero amounts.) Formulas DM in goods mfg Ending inventory = Direct material cost per unit x Vehicles produced = Direct material cost per unit x Vehicles in ending inventory CA 1 April 2017 May 2017 Revenues $ 14,950,000 $ 13.800.000 Direct material cost of goods sold Beginning inventory $ 360,000 Direct materials 5,040,000 4,320,000 Cost of goods available for sale 5,040,000 4,680,000 Deduct ending inventory (360,000) (360,000) Total direct material cost of goods sold 4.680,000 4,320,000 Throughput margin 10,270,000 9,480,000 1 Complete the rest of the throughput income statement. The manufacturing costs will consist of the other variable costs plus manufacturing fixed costs. You can find the other operating costs by referring to the absorption income statements given to you. (Direct mfg labor cost per unit + Mfg overhead cost per unit) x Vehicles produced other variable cost plus April 2017 $ 14,950,000 May 2017 $ 13,800.000 0 5,040,000 5,040,000 (360,000) Revenues Direct material cost of goods sold Beginning inventory Direct materials Cost of goods available for sale Deduct ending inventory Total direct material cost of goods sold Throughput margin Manufacturing costs Other operating costs Operating income $360,000 4,320,000 4,680,000 (360,000) 4,680,000 10,270,000 3,710,000 2,760,000 $ 3,800,000 4,320,000 9,480,000 3,480,000 2,590.000 $ 3,410,000 Requirement 1. Prepare income statements for Race Track Motors in April and May 2017 under throughput costing Begin by selecting the labels you will find in the statement. Remember, only the direct materials are considered variable under this costing method, so only direct materials will be included in the cost of goods sold. Revenues Direct material cost of goods sold Beginning inventory Direct materials Cost of goods available for sale Deduct ending inventory Total direct material cost of goods sold Throughput margin Manufacturing costs Other operating costs Operating income Now enter the amounts in the income statement. The revenues amounts will be the same in this statement as in the variable and absorption costing income statements. Use these formulas to calculate the amounts in the direct material cost of goods sold. (Enter a "O" for any zero amounts) Requirement 1. Prepare income statements for Race Track Motors in April and May 2017 under throughput costing Begin by selecting the labels you will find in the statement. Remember, only the direct materials are considered variable under this costing method, so only direct materials will be included in the cost of goods sold. Revenues Direct material cost of goods sold Beginning inventory Direct materials Cost of goods available for sale Deduct ending inventory Total direct material cost of goods sold Throughput margin Manufacturing costs Other operating costs Operating income Now enter the amounts in the income statement. The revenues amounts will be the same in this statement as in the variable and absorption costing income statements. Use these formulas to calculate the amounts in the direct material cost of goods sold. (Enter a "O" for any zero amounts) i Formulas DM in goods mfg Ending inventory = Direct material cost per unit x Vehicles produced = Direct material cost per unit x Vehicles in ending inventory April 2017 $ 14,950,000 May 2017 $ 13,800,000 $ 5,040,000 Revenues Direct material cost of goods sold Beginning inventory Direct materials Cost of goods available for sale Deduct ending inventory Total direct material cost of goods sold Throughput margin $ 350,000 4,320,000 4,680,000 (360,000) 5,040,000 (360.000) 4.680.000 10,270,000 4,320,000 9.480,000 Complete the rest of the throughput income statement. The manufacturing costs will consist of the other variable costs plus manufacturing fixed costs. You can find the other operating costs by referring to the absorption income statements given to you. April 2017 $ 14,950,000 May 2017 $ 13,800.000 $ 0 5,040,000 5.040,000 (360.000) 360,000 4,320,000 4,680,000 (360,000) Revenues Direct material cost of goods sold Beginning inventory Direct materials Cost of goods available for sale Deduct ending inventory Total direct material cost of goods sold Throughput margin Manufacturing costs Other operating costs Operating income 4,320,000 4,680,000 10,270,000 3,710,000 2,760,000 $ 3,800,000 9,480,000 3,480,000 2,590,000 $ 3,410,000 Requirement 1. Prepare income statements for Race Track Motors in April and May 2017 under throughput costing Begin by selecting the labels you will find in the statement. Remember, only the direct materials are considered variable under this costing method, so only direct materials will be included in the cost of goods sold. Revenues Direct material cost of goods sold Beginning inventory Direct materials Cost of goods available for sale Deduct ending inventory Total direct material cost of goods sold Throughput margin Manufacturing costs Other operating costs Operating income Now enter the amounts in the income statement. The revenues amounts will be the same in this statement as in the variable and absorption costing income statements. Use these formulas to calculate the amounts in the direct material cost of goods sold. (Enter a "O" for any zero amounts) i Formulas DM in goods mfg Ending inventory = Direct material cost per unit x Vehicles produced = Direct material cost per unit x Vehicles in ending inventory April 2017 $ 14,950,000 May 2017 $ 13,800,000 $ 5,040,000 Revenues Direct material cost of goods sold Beginning inventory Direct materials Cost of goods available for sale Deduct ending inventory Total direct material cost of goods sold Throughput margin $ 350,000 4,320,000 4,680,000 (360,000) 5,040,000 (360.000) 4.680.000 10,270,000 4,320,000 9.480,000 Complete the rest of the throughput income statement. The manufacturing costs will consist of the other variable costs plus manufacturing fixed costs. You can find the other operating costs by referring to the absorption income statements given to you. (Direct mfg labor cost per unit + Mfg overhead cost per unit) x Vehicles produced other variable cost plus April 2017 $ 14,950,000 May 2017 $ 13,800,000 0 5,040,000 5,040,000 (360,000) 360,000 4,320,000 4,680,000 (360,000) Revenues Direct material cost of goods sold Beginning inventory Direct materials Cost of goods available for sale Deduct ending inventory Total direct material cost of goods sold Throughput margin Manufacturing costs Other operating costs Operating income 4,680,000 10,270,000 3,710,000 2,760,000 $ 3,800,000 4,320,000 9,480,000 3,480,000 2,590,000 $ 3,410.000 Requirement 2. Contrast the results in requirement 1 with the absorption and variable costing income statements presented (Click the icon to view a summary of the operating income amounts from each statement.) * Data Table $ Method Variable costing Absorption costing Throughput costing April 3,915,000 $ 4,065,000 3,800,000 May 3,410,000 3,410,000 3,410,000 In April, throughput costing has the lowest operating income, whereas in May throughput costing has the highest operating income Throughput costing puts greater emphasis on sales as the source of operating income than does either absorption or variable costing. Requirement 3. Give one motivation for Race Track Motors to adopt throughput costing. Throughput costing puts a penalty on production without a corresponding sale in the same period. Costs other than direct materials that are variable with respect to production are expensed in the period of incurrence, whereas under variable costing they would be capitalized. As a result, throughput costing provides less incentive to produce for inventory than either absorption or variable costing

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Guidelines For Auditing Process Safety Management Systems

Authors: CCPS Center For Chemical Process Safety

2nd Edition

0470282355, 978-0470282359