Answered step by step

Verified Expert Solution

Question

1 Approved Answer

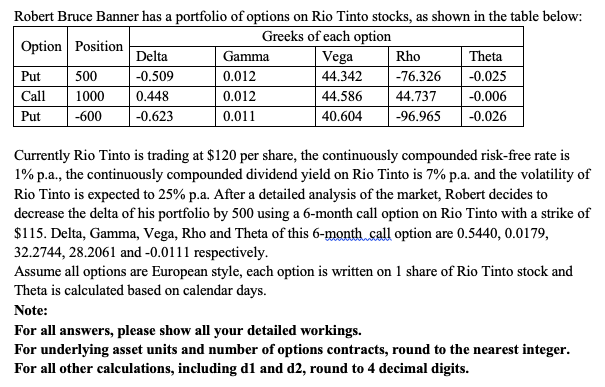

What view on Rio Tinto stock would justify Roberts decision to decrease the delta of his portfolio? Compute the Delta, Gamma, Vega, Rho and Theta

- What view on Rio Tinto stock would justify Roberts decision to decrease the delta of his portfolio?

- Compute the Delta, Gamma, Vega, Rho and Theta (using calendar days) of Roberts overall option position after trading the additional 6-month call options. Then, explain in plain English the meaning of each computed Greek letters.

- After trading the 6-month call options, Robert shorts 67 shares of Rio Tinto to make his portfolio delta neutral. If the share price of Rio Tinto decreased to $119 instantly, what should Robert do to keep his portfolio delta neutral? What are the risks of a delta neutral position?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Pricing And Hedging Financial Derivatives A Guide For Practitioners

Authors: Leonardo Marroni, Irene Perdomo

1st Edition

1119953715, 978-1119953715