Answered step by step

Verified Expert Solution

Question

1 Approved Answer

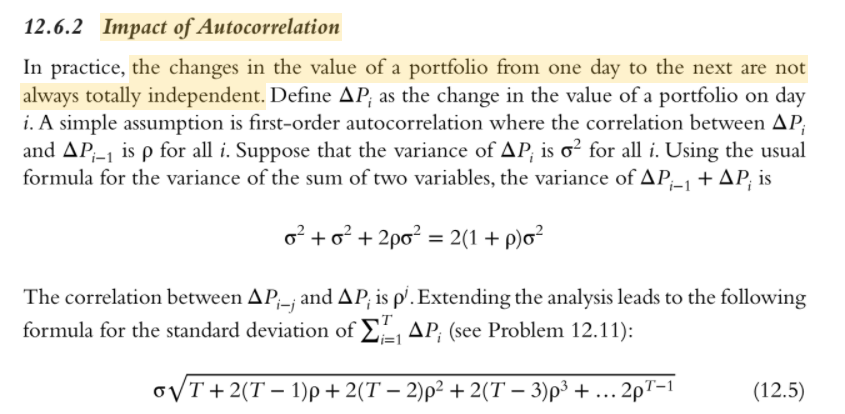

What were the steps taken to get from the first equation to the expression that's being multiplied by sigma ? 12.6.2 Impact of Autocorrelation In

What were the steps taken to get from the first equation to the expression that's being multiplied by sigma ?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Climate Mathematics Theory And Applications

Authors: Samuel S P Shen, Richard C J Somerville

1st Edition

1108750184, 9781108750189