Answered step by step

Verified Expert Solution

Question

1 Approved Answer

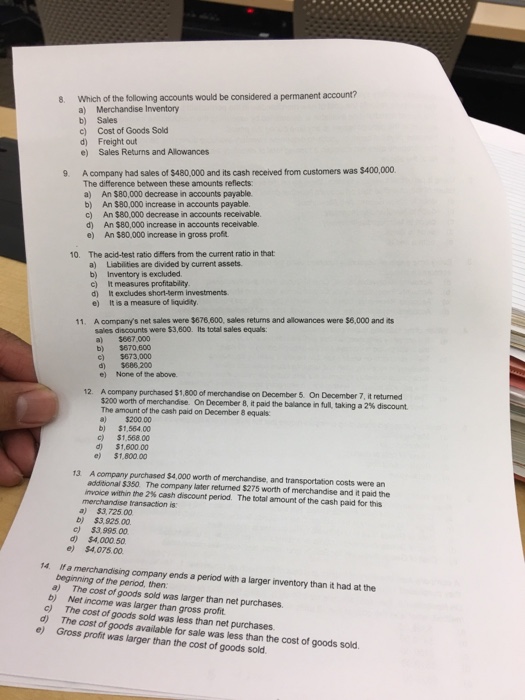

Which of the following accounts would be considered a permanent account? Merchandise Inventory Sales Cost of Goods Sold Sales Returns and Allowances A company had

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

New Horizons In The Field Of Management Audit As A Tool For Improving The Overall Management Of Enterprises A Guideline For Good Governance

Authors: Mohammed Sakhawat Hossain

1st Edition

3639194454, 978-3639194456