Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Which of the following statements describes an action of the agent that would be legal but not within the rules of the industry code of

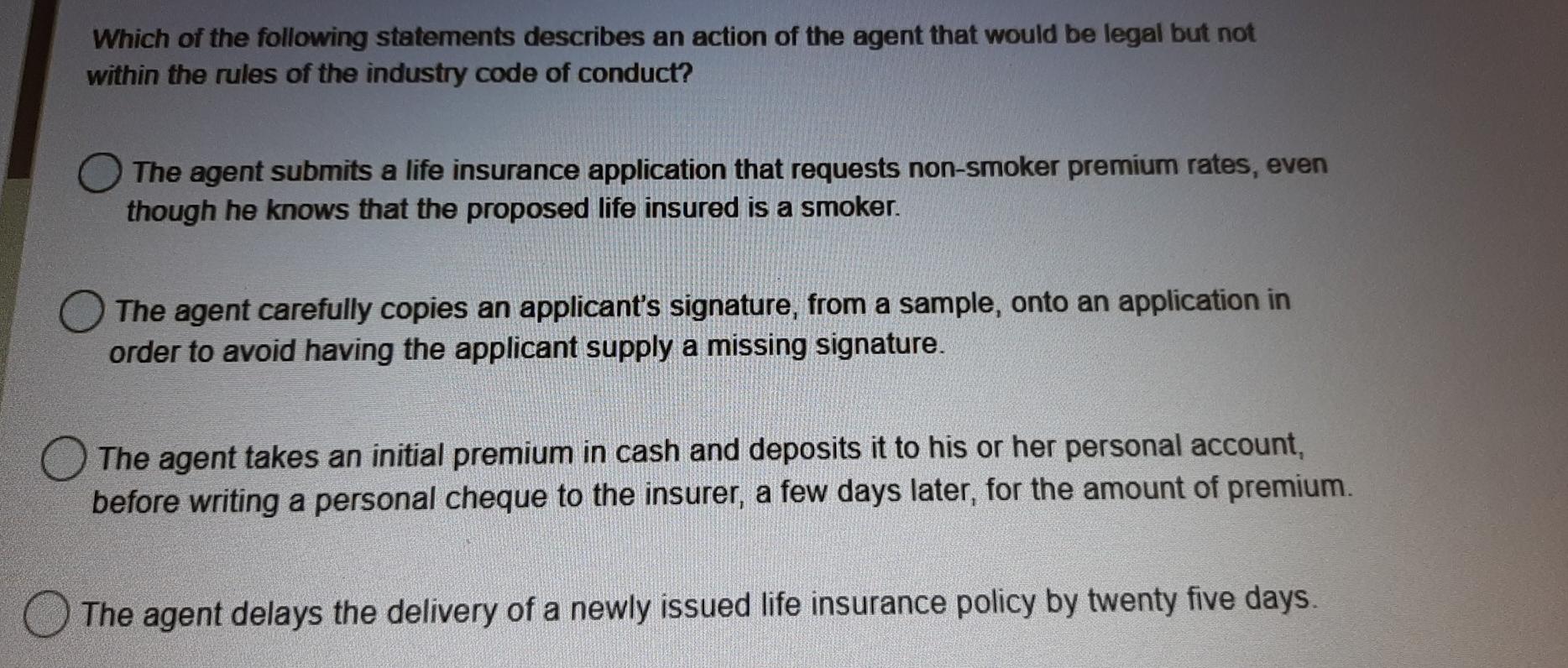

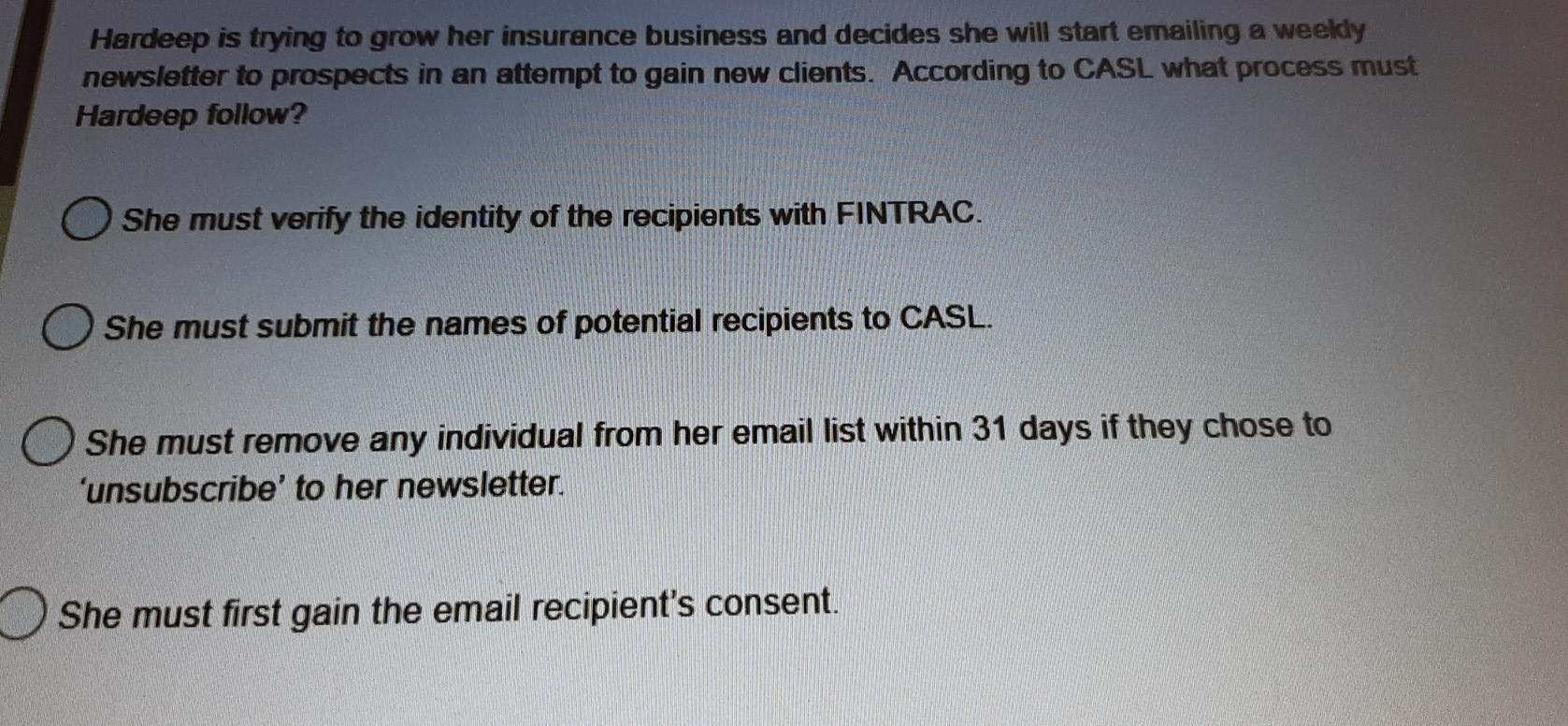

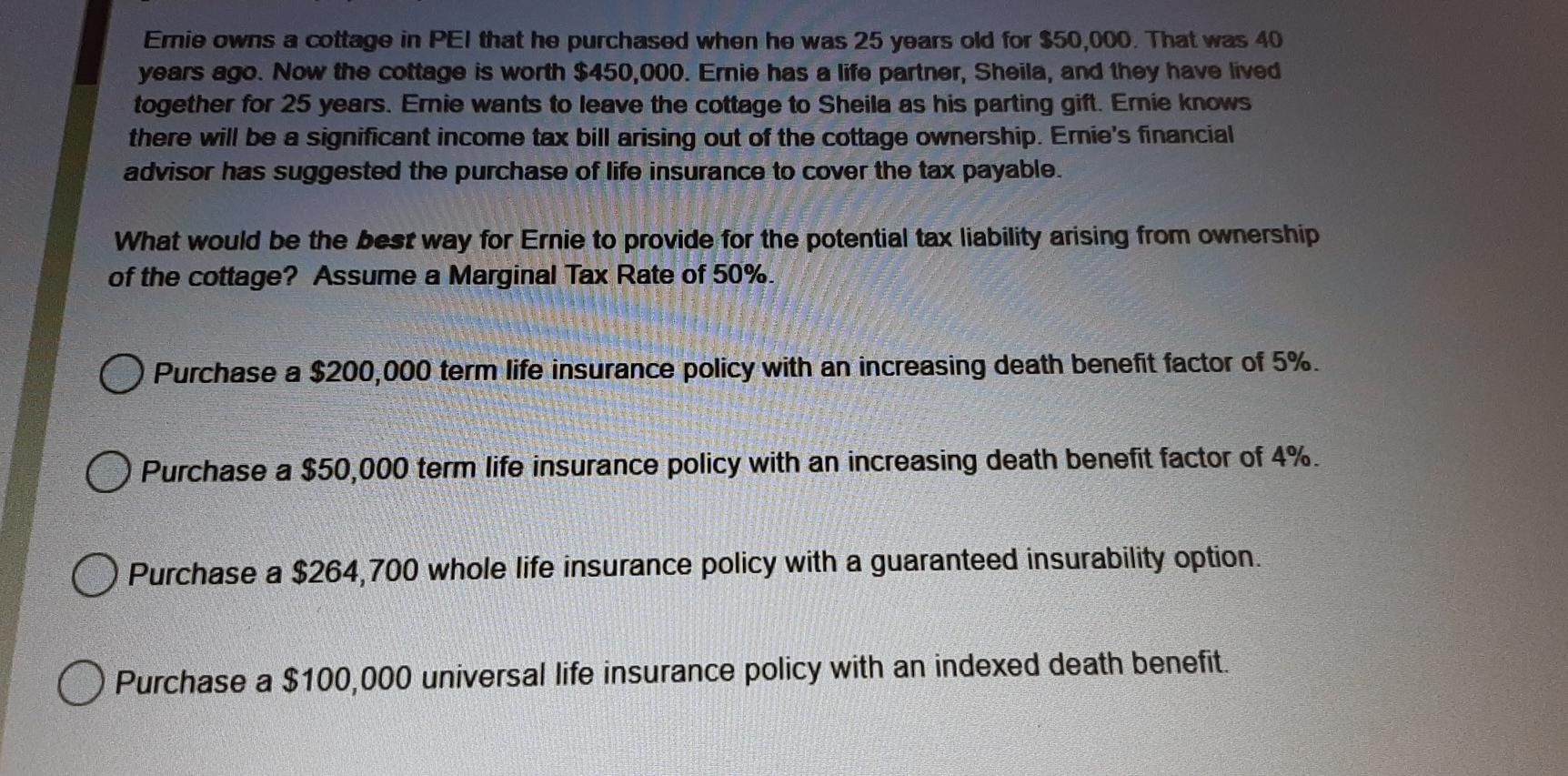

Which of the following statements describes an action of the agent that would be legal but not within the rules of the industry code of conduct? The agent submits a life insurance application that requests non-smoker premium rates, even though he knows that the proposed life insured is a smoker. The agent carefully copies an applicant's signature, from a sample, onto an application in order to avoid having the applicant supply a missing signature. The agent takes an initial premium in cash and deposits it to his or her personal account, before writing a personal cheque to the insurer, a few days later, for the amount of premium. The agent delays the delivery of a newly issued life insurance policy by twenty five days. Hardeep is trying to grow her insurance business and decides she will start emailing a weekly newsletter to prospects in an attempt to gain new clients. According to CASL what process must Hardeep follow? She must verify the identity of the recipients with FINTRAC. She must submit the names of potential recipients to CASL. She must remove any individual from her email list within 31 days if they chose to unsubscribe' to her newsletter. She must first gain the email recipient's consent. Emie owns a cottage in PEl that he purchased when he was 25 years old for $50,000. That was 40 years ago. Now the cottage is worth $450,000. Ernie has a life partner, Sheila, and they have lived together for 25 years. Ernie wants to leave the cottage to Sheila as his parting gift. Ernie knows there will be a significant income tax bill arising out of the cottage ownership. Emie's financial advisor has suggested the purchase of life insurance to cover the tax payable. What would be the best way for Ernie to provide for the potential tax liability arising from ownership of the cottage? Assume a Marginal Tax Rate of 50%. O Purchase a $200,000 term life insurance policy with an increasing death benefit factor of 5%. Purchase a $50,000 term life insurance policy with an increasing death benefit factor of 4%. Purchase a $264,700 whole life insurance policy with a guaranteed insurability option. Purchase a $100,000 universal life insurance policy with an indexed death benefit

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foreign Finance In Continental Europe And The United States 1815-1870

Authors: D.C.M. Platt

1st Edition

041538205X, 9780415382052