Why did Marvel have to file for bankruptcy? What is your assessment of Perelman's proposed restructuring plan - the one proposed in January 1997, not

Why did Marvel have to file for bankruptcy?

What is your assessment of Perelman's proposed restructuring plan - the one proposed in January 1997, not the one "floated" to analysts in November 1996.

Why is Perelman willing to invest in a company with negative equity value?

Will the solution solve the problems that caused Marvel to file for bankruptcy in the first place? Why? Or why not?

What are the alternatives and are any of them attractive to Perelman who is still in control of the firm? Are the creditors likely to approve the plan? Why? Or why not?

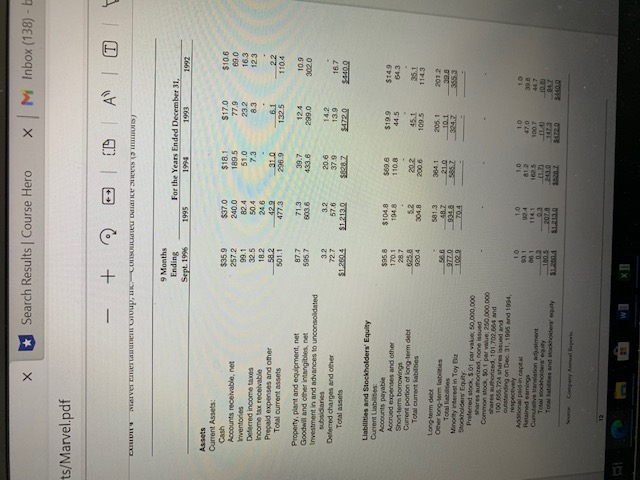

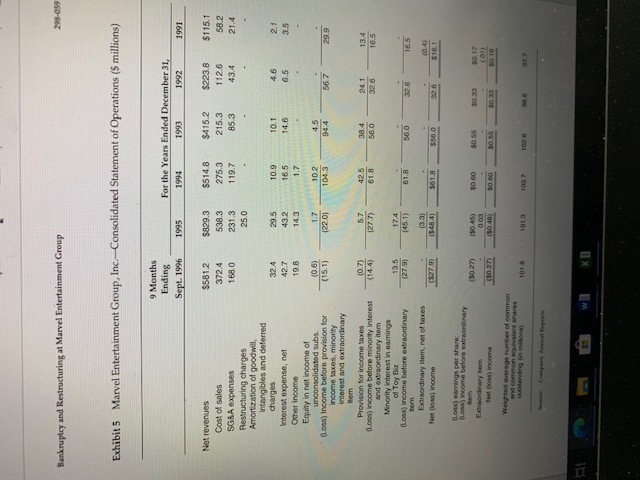

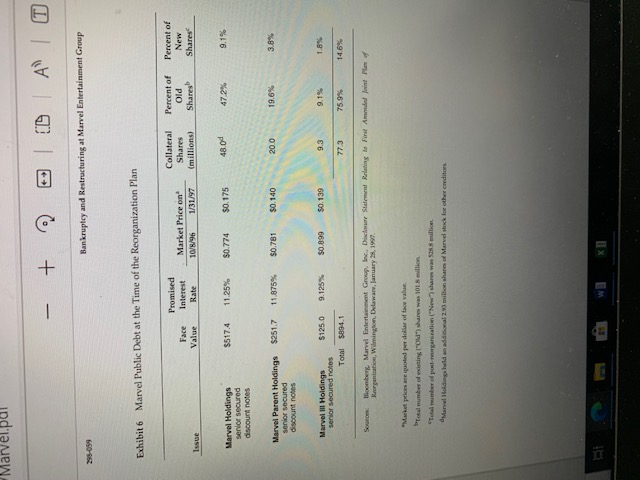

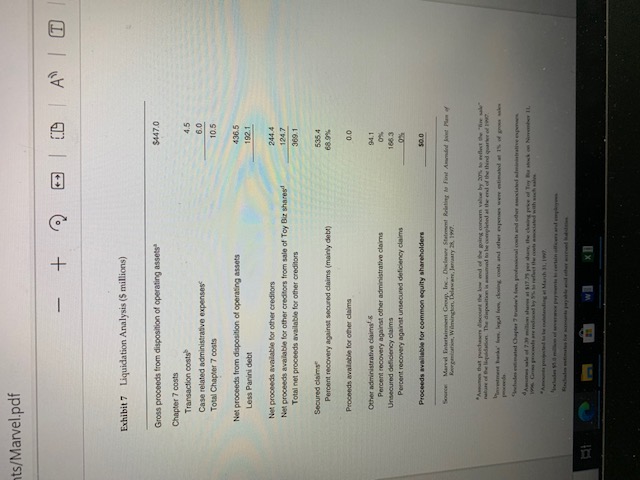

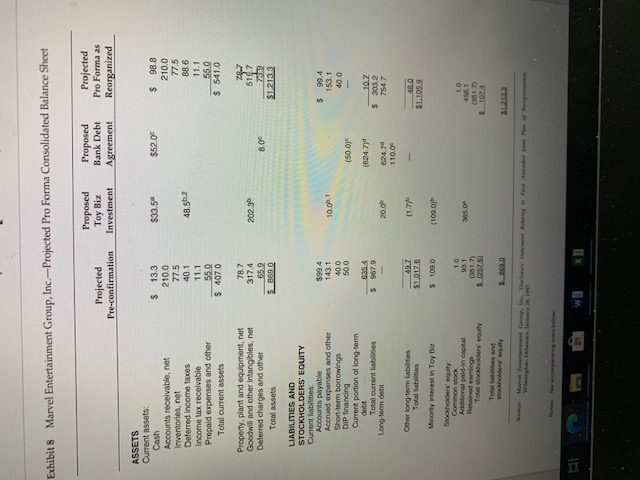

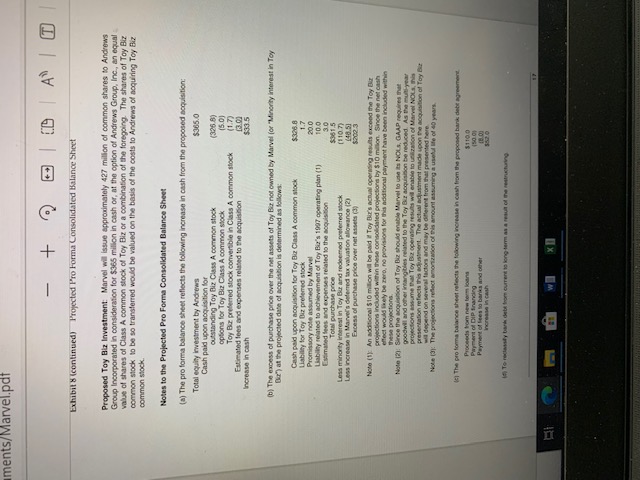

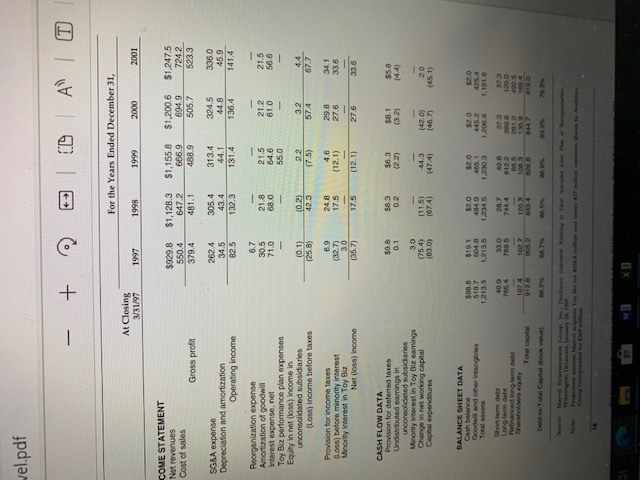

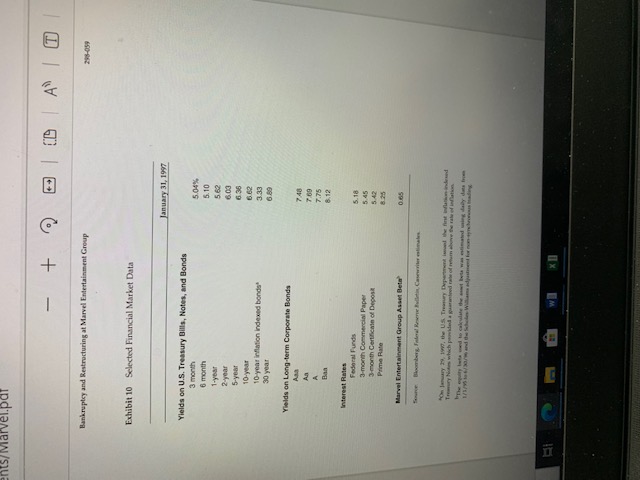

nents/Marvel.pai + | |A | | JASON AUERBACH Bankruptcy and Restructuring at Marvel Entertainment Group Not since the big retailing bankruptcies of the early 1990s has so much money been lost on Wall Street. Everyone is screaming murder. -Wall Street trader On January 28, 1997, one month after filing for Chapter 11 bankruptcy, Marvel Entertainment Group, Inc. (Marvel) filed its plan of reorganization with the United States Bankruptcy Court in Wilmington, Delaware. According to the plan, Ronald Perelman, Marvel's largest shareholder, would recapitalize the company by investing $365 million in exchange for 427 million newly issued shares. Perelman would then own 80% of the reorganized company's equity while public debtholders would receive 15% of the equity in exchange for debt with a face value of $894 million. Carl leahn, one of the many "vulture investors" who had purchased deeply discounted Marvel bonds with the hope of profiting on the reorganization, considered Perelman's plan an "unconscionable attempt to maintain control of Marvel at all costs" and was threatening to vote against it.? Perelman's spokesman responded by saying that Icahn's comments were "... slightly disingenuous and patently ridiculous." Based on the comments coming from both sides, it looked like the confirmation process might be a long and bruising one. Currently, the bankruptcy court had scheduled the confirmation hearing for March 7. 1997, at which time the interested parties would vote on the proposed reorganization plan. The question facing Carl Icahn and other debtholders was whether to accept Perelman's plan, reject it in favor of their own plan, or sell their bonds before the confirmation hearing. Perelman, on the other Linds Sandler, "Marvel Investors Find the Perila In Perelman's Superhero Plan," The Wall Street Journal, Novernber 15, 1997, p Cl. The quote refers to the numerous retailing bankruptcies including Campeau Corporation (1/90), Ame (4/My), Carter Howbry Lake (2/91% Hills (1/97) and Macy's (1/21 2-Bon Tholders File Motion to Take Control of Firm," The Wall Street Joumal, January 14. 1907, p. Bi. Floyd Morris, "1 Financier Cross Swords Over Marvel," The New York Time, December 28, 194 p. 41. Produce Benjamin C. Daly aral Jown Aunbuch jutla 197) propanal this cast. This case was developed from published phones and hart W X I+ + CD | A | T hand, had to determine whether the debtholders were just posturing or were, in fact, serious about voting against the plan. History of Marvel Entertainment Group In 1939, an entrepreneur named Martin Goodman started the comic book business which today is known as Marvel Comics. He became famous for creating a number of superheroes including Captain America, who fought against the Germans during World War II Over time, Marvel illustrators created more than 3,500 comic characters including The Fantastic Four, Daredevil, The Incredible Hulk, The X-Men, Thor, and Spider-Man. Ron Perelman, known for his successful takeover of Revlon and his unsuccessful takeover of Gillette, bought Marvel in January 1989 for $62.5 million, financed with only $10.5 million of equity. Through his MacAndrews & Forbes holding company and several subsidiary holding companies, Perelman owned a wide range of businesses including Revlon (an international cosmetics company). Coleman (an outdoor recreation equipment company), First Nationwide Bank (a California-based savings and loan association), Consolidated Cigar (a cigar company), and the Andrews Group (an entertainment and publishing holding company) (see Exhibit 1). Although this holding company structure was complex, it provided Perelman with both legal and financial protection, From a legal perspective, limited liability at the subsidiary level protected the holding companies from financial liability in default situations. From a financial perspective, consolidation allowed the holding companies to share net operating losses across firms because they typically owned at least 80%% of the subsidiaries, the minimum level required by the Internal Revenue Service (185). According to a tax analyst at Lehman Brothers, Perelman "... knows how to exploit net operating losses better than anyone." Another analyst commented: [In 1996, his companies] is. generated more than $600 million in profits, yet a careful reading of their financial statements suggests they paid little or nothing in taxes to the US. government. Through skillful use of holding companies and tax laws, Perelman's people have become expert at minimizing his tax bill. If not for such handiwork, his companies would have probably owed somewhere in the neighborhood of $200 million to the Treasury last year." The Rise and Fall of Marvel Entertainment Group In addition to being known as a shrewd financier, Perelman had a reputation for buying and reviving underperforming companies. After buying Marvel, he quickly eliminated unprofitable lines of business and streamlined operations. In its first year under Perelman's control, Marvel's net income increased from $2.4 million to $54 million, while revenues increased from $645 million to 451 8 million. Eighteen months later, he sold 43 million shares to the public at a price of $16 50 per share a split adjusted price of $2 06. He used the proceeds to repay 536.5 million of acquisition debt and to pay a cash dividend of $372 million to his holding company. The dividend alone amount quadrupled his initial equity investment in the span of less than two years; the return, counting his remaining 653. ownership position, was almost 16 times his original investment, Commenting on Aug 3. IPA. P. 57 WBankruptcy and Restructuring at Marvel Entertainment Group what appeared to be the darling of Wall Street, Donald Drapkin, vice chairman of MacAndrews & Forbes, said, "We've never disappointed investors in a public offering." Perelman set out to build a diversified youth entertainment company using the comic book business as a foundation. He accomplished the diversification by acquiring other entertainment companies. First, he acquired Fleer, the second largest manufacturer-after Topps Company-of sports and entertainment trading cards, in July 1992 for $285 million, a 12%% premium over the current market price. In March 1993, Perelman acquired a minority position in Toy Biz, a designer and retailer of children's toys, in exchange for an exclusive, perpetual, royalty-free license to use all of Marvel's characters. Then, in July 1994 he acquired the Panini Group, an Italian producer of sports and entertainment stickers, for $150 million. While he was actively diversifying outside of Marvel's core comic book business, Perelman was also attempting to consolidate the comic book industry. In the early 19905, Marvel was the leading publisher of comic books, followed closely by DC Comics and Archie Comics. During 1994, Marvel acquired four other comic book publishers including Harvey Comics and Malibu Comics, Marvel also changed its distribution strategy to concentrate on comic book specialty stores rather than subscriptions or the traditional mainstream retailers such as newsstands and convenience stores. Because sales to specialty stores were final (te., they could not return unsold comic books), they yielded higher margins. As this strategy began to succeed, Marvel's stock price began to rise, peaking in November 1993 at 534 75 per share for a total market value of $3 3 billion (see Exhibit 2). Given the strength of Marvel's stock price, Perelman saw an opportunity to increase his ownership of Marvel Entertainment Group above the 80 level that would allow him to incorporate Marvel into the MacAndrews & Forbes holding company for tax purposes. Through a tender offer and open market repurchases, the Andrews Group acquired more than 20 million shares, thereby boosting its consolidated ownership to 806% To finance the repurchases, Perelman issued debt through three different Andrews Group holding companies (see Exhibits 1 and ?). First, Marvel Holdings issued $5174 million of zero coupon series secured notes yielding 11 15%%, The cash proceeds from this offering were $246 6 million and the debt why secured by 480 million Marvel shares. Marvel Parent Holdings then baued $151.7 million of zero coupon senior secured notes yielding 11875% This offering produced $1449 million in cash and was socared by 20.0 million Marvel shares. Finally, Marvel Ill Holdings issued $125 million in senior secured notes yielding 9.125%. The interest payments on these bonds would be made from revenues received through las sharing agreements between Marvel and Marvel III Holdings, Like the other two issues, this debt was secured by Marvel shares- in this case, 93 million suing All thieve issues were scheduled to mature in April 1978 Perriman used this firuncial strategy of equity backed debt throughout MacAndrews & Forbes In fact, he issued $1 7 billion of share collateralized bonds in 1943 alone for Marvel, Revlon, and Coleman." This debt was like margin loans in that it was secured by Marvel's equity rather than its assets or operating cash flows. Nevertheless, with the stock price trading above $3500 per share, the 73 million shares of collateral had a value of more than $1.9 billion, well above the lace value of $314.1 million W X+ 298-039 Bankruptcy and Reitrecturing at Marvel Entertainment Group Shortly after the third issuance, however, Marvel's core businesses began to falter. Marvel's CEO Scott Sassa summed it up this way: "When the business turned, it was like everything that could go wrong did go wrong." The decline in sales was driven largely by disappointed collectors who had viewed comic books as a form of investment. For years, Marvel had capitalized on the speculative frenzy of collectors by increasing the number of monthly titles from 45 to some 140 and doubling prices from $1.50 to $300 per comic book." But collectors stopped buying in 1994 after failing to realize significant returns, causing sales to fall 19% across all distribution channels. The company had pandered "an to the speculative excesses of collectors, turning out pricey comics with fancy covers while neglecting their core readers," said Harry DeMott, a CS First Boston analyst covering Marvel.10 Jim Shooter, Marvel's former Editor in-Chief and a current competitor, was more critical. He said that Marvel had been "strip-mining the company" for years. ! Just as the comic book market began to tum south, so too did the trading card market due to strikes in both professional baseball and hockey. In addition to collector apathy stemming from the strikes, trading cards increasingly had to compete with other forms of entertainment. Jill Krutick, a Smith Barney analyst covering Marvel who had recently slashed her comings estimates, remarked that ". little boys have found alternative means of entertainment, such as video games "i Finally, as in the comic book market, speculators who were active purchasers in the early 1990 stopped buying after failing to realize significant returns. In total, trading card sales would fall by more than W's over the next two years. Because of declining revenats and missed profit estimates, Marvel's stock price began to fall. After Marvel reported a 33%% drop in first quarter net income for 1995, "Short on Value," an investment newsletter, recommended it as an attractive stock to sell short Despite the problems, Perelman continued building his entertainment company, In March 1995, Marvel acquired SkyBox International Inc, a maker of trading cards, for $150 million. The SkyBar acquisition provided an opportunity to buy an undervalued asset, to expand Marvel's presence in the trading card business, and to realize operational synergies with Fleer. Marvel paid a 25% premium to acquire SkyBox and financed the acquisition with $190 million of additional debt. Four months later, in July 1945, SMP downgraded the holding company debt from B to , noting that "... Marvel's warnings from baseball and hockey cards have fallen while the company has added debt to make acquisitions " Morcover, they predicted that Marvel might need to restructure its debt in the next 12-18 months. Following the SkyBlox acquisition, Marvel had, indeed, become a diversified entertainment company. As of year end 1595, It had six principle lines of business, four of which were approximately equal in she+ 1. Sports and Entertainment Cards (224% or revenuesk sold picture cards depicting professional athletes and other entertainment figures through its Fleer and SkyBox subsidiaries; 2. Toys (21.7% of revenues) designed, manufactured, and distributed children's toys based on Marvel characters through its Toy Biz subsidiary; 3. Children's Activity Stickers (207%): sold sports and entertainment stickers worldwide through its Panini subsidiary; 4. Publishing (1784): published comic books; 5. Confectionery (10.9%) manufactured confectionery products-primarily gum; 6. Consumer Products and Licensing (6.4%): licensed characters for merchandise. Although diversification was, in theory, supposed to protest against downturns, Marvel lost $495 million in 1995, mainly due to the losses in its comic book and publishing segments. To address its declining profitability, Marvel announced a restructuring plan in early 199% consisting of layoffs, imination of unprofitable comic book titles, Improved editorial content, and consolidation of operations. " Even with the restructuring Marvel reported a loss of $27.9 million through the first Three quarters of 1996. Exhibits 4 and 5 show Marvel's balance sheet and income statements Moreover, it reported losses in three of its four largest divislore: comic books, trading cards, and retrillinment stickers. During the summer, Perelman bought an additional one million shares at 51000 per share. Is On October 5, 1996, Marvel announced that it would violate specific bank loan covenants dur to decreasing revenue and profits. Following the armourcomment, Moody's downgraded Marvel's public debt causing the price of the zero coupon bonds to fall by more than 41% (for Exhibit j)." One month later, on Thursday, November 8, 1906, Howard Gittis, vice chairman of Andrews Group, called Fidelity Investments and Putnam Investments, two of the largest institutional holders of Marvel's public debt, and asked them what they would like to see in a restracturing plan. The next day, the two firms sold more than 570 million of Marvel bonds at a price of $037 per dollar of face value. When a spokesman for the Andrews Group announced the details of the proposed restrictioning plan four days Later, Marvel's stock price fell by 41% and its zero coupon bands feil by more than 505, to 50.18. Reporters later asked representatives of both companies why the sold the bands when they did. A spokeswoman at Putnam responded, "(Wel received various bids ... that were attractive,"while a spokeswoman at Fidelity responded, "We'd been selling since early October." The sales saved the companies approximately $14 million in extra losses W x ts/Marvel.pdf + Perelman's Initial Restructuring Plan Perelman's restructuring plan contained three parts. First, the Andrews Group would invest $350 million in Marvel in exchange for 410 million new Marvel shares to ensure it maintained 80% control. Thus, the new shares would be valued at 50.85, compared to a price of $4.625 for the existing shares the day before the announcement, the existing shares closed at $2.75 on the day of the announcement. Second, Marvel would acquire Toy Biz, a company that made toys based on Marvel characters. Marvel already owned 26.7% of Toy Biz and would use the cash investment to buy the remaining outstanding shares at a 32%% premium and some of the insiders' shares at market prices. There were two reasons to acquire Toy Biz: it had close business connections to Marvel and provided a large fraction of Marvel's revenue, and it generated approximately $60 million of cash flow per year which could be used to service Marvel's debt as well as offset more than $100 million of net operating losses (NOIs). Without 80% ownership of Marvel, Andrews Group could not use the NOLs. Finally, the public debtholders would exchange debt with a face value of $594.1 million for equity in the newly recapitalized firm. Specifically, they would seize their collateral shares and hold 14.6% (/73 cullion shares) of the new shares face Exhibit 6) In contrast, Marvel Entertainment Group would repay its secured creditors (consisting primarily of banks) and its unsecured creditors (cocaisting primanly of suppliers and employees) in full Ever since Perelman proposed the restructuring plan, so-called "vulture investors", including Carl leahn, had been buying the public debt. Icahn, who made his name in the 1980s with takeovers of Trans World Airlines, Interco, Southland, USX, Texaco, and several other companies, bought approximately 25% of the bonds at prices ranging from 20 to 12 cents per dollar of face value." One analyst described leshn this way. "His trend is to look for companies that are having trouble that he can turn around. He's been very successful. To an extent, it's the money, but it's the game more than anything ... Carl's always liked to rattle [ management's] cages .. . I think he gets a charge out of that ..." On December 10, 1996, Carl leahn sent a letter to the Andrews Group proposing an alternative restructuring plan consisting of a $350 million cash infusion through a rights offering. His plan. however, did not include the Toy Biz acquisition. In the letter, kahn indicated that he would not "appart Perelman's proposed restructuring plan and vowed to fight him in bankruptcy court. Publicly, Icahn said, "It is patently clear that Ron Perelman has adopted this course in realise a windfall profit for herself at the expense of those to whom he owes a fiduciary responsibility."?: In response, Perelman representatives warned that Marvel would be forced to file for bankruptcy unless the boredholders agreed to the plan in its current form. When it became clear that the bor Sholders were not going to give in, Marvel and its three primary holding companies filed for bankruptcy on December ?, 10 Soft Size, Marvel's CLO. sold, "We would have preferred tore- capitalize Marvel without having to peck the aid of the court, but the actions and positions taken by the bondholders prevented that approach, Calling Ledopen, Te w x+ + + Bankruptcy and Restructuring at Marvel Entertainment Group 390-059 Marvel in Bankruptcy Although Marvel and its holding companies filed separate bankruptcy petitions, the interlocking nature of the cases made it possible that the bankruptcy court might consolidate them into a single process. Whereas Perelman wanted to keep the cases separate so the public debtholders would not have a say in restructuring Marvel Entertainment Group (the operating company), Icahn and the public debtholders wanted to consolidate the cases so they could play an active role in restructuring it. In fact, the bankruptcy trustee appointed leahn as the chairman of the creditor committee in early January, a signal the public debtholders would be involved with the restructuring. By filing for bankruptcy, Marvel became eligible for Debtor-In-Possession (DIP) financing. Perelman arranged for $100 million in DIP financing from Chase Manhattan Bank to "ensure Marvel had sufficient liquidity to pay all current and expected trade and employee obligations and to meet all of its operating and investment needs during the reorganization process."What was unique about this loan was the fact that it was contingent upon Perelman remaining in control and would immediately come due in the event of a change in control. According to standard bankruptcy procedure, Marvel's management had an exclusive 120-day period in which to propose a reorganization plan. The bondholders immediately challenged this provision claiming that Perelman had "a negligible economic interest in Marvel" because he had pledged the shares to the bondholders as collateral. Given their ownership of the collateral shares, the bondholders argued that they, not Perelman, should have the right to propose the first reorganization plan. The bankruptcy court, however, enforced the automatic stay by rejecting the bondholders' motion One month after filing for bankruptcy, Marvel announced its preliminary financial results for 1946. It expected to report a loss of approximately $425 million for the year largely due to a write off of goodwill associated with its trading card business. The non-cash charge of $370 would reduce stockholders" equity to negative $245 million. Marvel's Amended Reorganization Plan To assist with the reorganization plan, Perelman hired Bear Steams & Company. After a month of financial analysis and legal work, Marvel filed an amended reorganization plan with the bankruptcy count on January 28, 1997. Much to the bondholders' chagrin, it was virtually identical to the first plan albeit with some minor changes, Rather than investing $350 million to buy 410 million now thanes, Perelman was now proposing to invest $365 million to buy 427 million new shares the average price would will be KINS per share compared to a current market price of 5300 per share According to Bear Steam, "the current market price of Marvel's common stock (did) not reflect thes/Marvel.pdf + 290-059 Bankruptcy and Restructuring at Marvel Entertainment Group reorganization value of Marvel."* CS First Boston provided a fairness opinion to Marvel's board in support of the Andrews Group investment.7 As part of its review, Bear Stearns conducted three sets of analysis. First, as required under Chapter 11, it prepared a liquidation analysis to show that Marvel was worth more as a going concern than it would be under a Chapter 7 liquidation (the "best interests test," see Exhibit 7). According to the liquidation scenario, Marvel debtholders (primarily banks) would recover approximately 70 cents on the dollar while the holding company debtholders and equityholders would get nothing. Second, Bear Stearns prepared an analysis of Marvel as a going concern without the Toy Biz acquisition. Bear, Stearns estimated that the total enterprise value was between $520 and $660 million. Given Marvel's projected net indebtedness of $725 million as of March 31, 1997, the equity would again be worthless. Finally, Bear Stearns prepared financial projections for the company as a going concern assuming Marvel acquired Toy Biz (Exhibits 8, 9, and 10 contain financial projections and other related information). Perelman's vision was "to transform the company into an integrated entertainment and sports content company prominent in all forms of media, print, electronic publishing, toys and games." In the future, Marvel would operate theme restaurants, own a movie studio, and produce entertainment software and on-line applications. The projections assumed "modest" growth for Marvel and "significant" growth for Toy Biz due to new media exposure. In addition, the projections assumed that Marvel would exist as a stand-alone entity filing its own federal and state income tax returns, and that the deal would close on March 31, 1997. Under this scenario, Marvel's secured and unsecured creditors would be paid in full. Based on this analysis, Bear Stearns concluded that Marvel was worth more as a going concern because of (i) increased administrative costs associated with Chapter 7 Liquidation, (il) lower asset values in liquidation because of a 'forced sale," fill lower asset values for key parts of business due to exit of key employees and loss of customers, and (iv) the amount of claims which would need to be satished on an absolute priority basis in a liquidation." Besides showing that the reorganisation yielded equal or greater value to all classes of claimants, the Andrews Group had to show that the plan was feasible (the "feasibility test") In other words, that it was not likely to be followed by liquidation or another reorganization. Convincing the court that a company with a debt-to total capital ratio of 557, ($805.4 million in total debt and $1074 million in equity) might not be easy even though the company would initially have considerable cash balances. The Vote on March 7" The vote on March 7" would pit Carl Icahn against Ronald Perelman, Because Perelman had filed for bankruptcy, he no longer needed the unanimous support debtholders that was required for out of-count settlement. He did, however, need a majority (51% by number and two thirds by dollar amount of the claimants in each creditor class to vote for the plan. Even if he were unable to secure thewe votes, them was still a chance that the bankruptcy judge would approve the plan Judge Falick Wvel.pdf - + This document is witharmed for use only by Mary Wondt In Spring 2023 Financing Now Ventures . Merge at Purdue University, 2023, Bankruptcy and Restructuring at Marvel Entertainment Group could approve such a plan provided it did not discriminate unfairly against non-accepting creditor classes and provided it was fair and equitable to all classes. As the days went by, tempers began to rise on both sides, A lawyer representing the bondholders challenged Bear Stearns conclusions. "How objective is a valuation if investment bankers have a financial interest in the outcome (a reference to the $1 million contingency fee Bear Stearns would receive if Perelman's plan succeeded)?"What bothered people the most was Perelman's valuation. One analyst commented, "People thought he'd buy in at a discount, but no one expected it would be this dramatic."" To which Howard Gittis, the Vice Chairman of Andrews Group responded, Bondholders ought to be thankful that Ron is willing to put up $365 million in cash to save this company."I With a little more than a month to go before the confirmation hearing, It was unclear whether enough creditors would vote for Perelman's plan.X Search Results | Course Hero X M Inbox (138) - b ts/Marvel.pdf + + 0 A | T / 9 Months Ending For the Years Ended December 31. Sept 19% 1995 1974 1493 1992 Assets Current Assets: $35.9 $37 0 $18.1 $17.0 $10 6 Accounts receivable, net 257.2 240.0 189.5 77.9 Inventories 99.1 82.4 51.0 23.2 16.3 Differed income taxes 32.5 50.4 7.J 8.3 121 Income the ricohable 18.2 24.0 Prepaid expenses and other 582 429 31.0 22 Tell current msets 501.1 477.3 208 0 132 5 1104 Property, planit and equipment, net 87.7 71.3 39.7 124 109 Goodwill and offer Intangible, net 595.7 803 6 433.6 289.0 302.0 Inwhatment in and advances to unconsolidated 32 32 2016 Defamed charges and other 57.6 139 167 $1,2604 $1.2130 Liabilities and Stockholders' Equity Accounts parable 595 8 $1048 5149 Accrued mpegnippy and other 170.1 Shon-to borrowings 287 Current portion of long-term debt 625 8 20 2 45.1 Toul current Inbites 9204 200 4 11-13 581.3 384.1 2012 21.Q Toul Lation 977.0 3553 Minority interest In Toy Bar 102 0 Potholder' Equity Prefered stock, 1.01 parvabie, 30 000,000 whim autofired, none higed Common stock to 1 par value: 260,000 009 warm authorized, 101 702 084 and 100 035,124 shares hound ard outwording on Dec. 11, 108 and 1094, 10 10 1.0 47.0 Total Mockholdin' caly 2410 12 W X IIBankruptcy and Restructuring at Marvel Entertainment Group 298-059 Exhibit 5 Marvel Entertainment Group, Inc.-Consolidated Statement of Operations ($ millions) 9 Months Ending For the Years Ended December 31, Sept. 1996 1995 199- 1993 1992 1991 Net revenues $581.2 $829.3 $514.8 $415.2 $223.8 $115.1 Cost of sales 372.4 538.3 275.3 215.3 112.6 58.2 SGLA expenses 168.0 231.3 119.7 85.3 43.4 21.4 Restructuring charges 25.0 Amortization of goodwill, intangibles and deferred charges 32 4 29.6 10.9 10.1 21 Interest expense, net 42.7 43.2 165 14.6 Other income 19.8 14.3 1.7 Equity in net income of unconsolidated subs, (0.6) 1.7 102 1.5 (Loss) Income before provision for (15.1) (22.0) 104.3 14.4 567 29 9 Income taxes, minority interest and extrordinary Provision for income taxes 0.7) 57 42 5 28.4 24.1 13.4 (Lois) Income before minority Inforest (14.4) 127.7) 618 560 16.5 hand extrordinary item Minonty interest in earnings of Toy Bar 15.5 17.4 (Loss) Income before Saltordinary 127.9) 145.1) 61.8 32.6 Extraordinary Ham, not of taxes 3.31 104) Hel Dows) Income ($27.0) 1548.41 Lomoj earrings por share: Flout Income butera extraordinary 150. 48 Eximordinary Rem That goods) Income 150.401 Thelighted brorage member of common 1019 X IMarvel.pal - + Bankruptcy and Restructuring at Marvel Entertainment Group Exhibit 6 Marvel Public Debt at the Time of the Reorganization Plan Promised Collateral Percent of Percent of Face Interest Market Price on" Shares old New Issue Value Rate 1/31/97 (millions) Shares Shares Marvel Holdings $517.4 11.25% $0.774 $0.175 48.04 47 2% 9.1% senior scoured discount notes Marvel Parent Holdings $251.7 11.875% $0.781 50.140 20.0 19.6% 3.8% senior secured discount notes Marvel Ill Holdings $125 0 9.1285 $0.090 50. 139 9.1% sector secured notes Total $894.1 773 75.9% 14.6% Bombing Marvel Entertainment Group, Inc. Distance Statement Printing to First Amarided Joint Plan of Keorganization, Wilmington Delaware, January 28, 1987. "Market prices are quoted per dollar of face value. Total number of existing ["(d") than was 101 8 million Total murder of post resugariration ("New") shares was 526.8 million. " Merval i beddings held an additional ? ") million shares of Marvel plock for other eneditions. X IIits/Marvel.pdf + | |AT Exhibit 7 Liquidation Analysis (5 millions) Gross proceeds from disposition of operating assets" $447.0 Chapter 7 costs Transaction costs 4.5 Case related administrative expenses" 6.0 Towl Chapter 7 coats 105 Net proceeds from disposition of openting assets 436.5 Less Parini debt 152.1 Not products available for other crednors 244 4 Net proceeds available for other creditors from sale of Toy Biz shares! 124.7 Total not proceeds available for other creditors 369 1 Secured claims" 535 4 Percent recovery against socured claims (mainly debt) Progoods available for other claims 04.1 Percent recovery against other administrative claims Unsecured deficiency claims 1483 Percent recovery against unsecured delicaency claims Proceeds rivallable for common equity shareholders 50.0 Bargaininga, Wilmington, Delaware, January 28, I97. w xExhibit 8 Marvel Entertainment Group, Inc.-Projected Pro Forma Consolidated Balance Sheet Proposed Proposed Projected Projected Toy Biz Bank Debt Pro Forma as Fre-confirmation Investment Agreement Reorganized ASSETS Current assets: Cash 13.3 $33 5" $52.09 98.8 Accounts receivable, net 210 0 210.0 Inventories, net 77.5 77.5 Deferred Income taxes 40.1 48.562 Income tax receivable 11.1 11.1 Prepaid expenses and other 550 55.0 Total current assets $ 407.0 $ 541.0 Property. plant and equipment, net TA. 7 Goodwill and other intangibles, not 317.4 202 30 5157 Deferred charges and other 65.5 Total assets $ 850.0 $1.2153 LIABILITIES AND STOCKHOLDERS' EQUITY Current Labilities: Accounts payable $99.4 Accord expenses and other 143.1 10.00.1 153.1 Short-tom borrowings 40 0 40.0 DIP financing 50 0 (50.0) Current portion of long-term dobe 635.4 (624.719 107 Total carron! lablies 867.8 3032 20 0 524,7d 7547 110.0 Other long-term Labilities (1.7)5 Towl Habiting $1.017.G $1.105 9 Minority Interest in Toy Bar $ 109.0 Comman work 1.0 Additional pald in capital 1.0 90. 1 1341.7) Tol Intition Brel 1 060.0ments/Marvel.pdf + | |AT Exhibit 8 (continued) Projected Pro Forma Consolidated Balance Sheet Proposed Toy Biz Investment: Marvel will Issue approximately 427 million of common shares to Androws Group Incorporated in consideration for $365 million in gush or, at the option of Andrews Group, Inc., an equal value of shares of Class A common stock of Toy Biz or a combination of the foregoing. The shares of Toy Biz common stock to be so transferred would be valued on the basis of the costs to Andrews of noquiring Toy Biz common stock. Notes to the Projected Pro Forma Consolidated Balance Sheet (a) The pro forma balance sheet reflects the following increase In cash from the proposed acquisition: Total equity investment by Andrews $365.0 Cash paid upon noquisition for outstanding Toy Biz Class A common stock (326 83 options for Toy Biz Class A common stock (5.0] Toy Biz preferred stock convertible in Class A common stock (17) Estimated foes and expenses related to the noquishon Increase in cash b) The excess of purchase price over the net asort of Toy Fix riot owned by Marvel for "Minority Interest in Toy Car") at the projected date of noquittion is determined as felkwei: Cath paid upon noquisition for Toy Biz Class A common stock $376.8 I Liability for Toy Diz protemed stock 1.7 Promissory note assumed by Marvel 20 0 Lishiny related to achievement of Toy Biz's 1997 operating plan (1) Limited took and expenses related to the soquestion 30 Total purchase price Less minority Interest in Toy Bar and redeemed polened Mock 110 7) 648.51 Excessjol purchase price over net itity py $302 3 Not (1) An additional $10 million will be paid @ Toy Bic's actual opening mouits second the Toy Bur projections Included within thewe consolidated projectors by $10 million, Shoe the net cash cited would booty be nero no provisions for this add banal payment have bow included within thewe projections. Mate 21: Since the acquisition of Toy Biz should mable Marvel Is via Its NOIS GAAP request inat goodwill and other intangibles related to the Toy Bir acquiton be reduced As the suite year protections intome that Toy Biz opening to with will enable to utilization of War HOLs, Tha presentation reflects his adjustment. The actual adjustment made upon The soquestion of Toy But Note Ij: The projections hect amonlawton of this amount assuming a unghad Up of 40 pan. Hel The pro forma balance sheet reflects the following incompass in cash from the proposed bank debt agreement $1190 Payment of Lees to banks and other w X IIvel.pdf + For the Years Ended December 31, At Closing 3/31/97 1997 1998 2000 2001 COME STATEMENT Net revenues $929.8 $1,128.3 $1.155.0 $1.200.6 $1 247.5 Cost of sales 550.4 647.2 666.9 694.9 724 2 Gross profit 379.4 481.1 480 9 505.7 523.3 SGLA expense 262 4 305.4 313.4 324.5 336 0 Depreciation and amortization 34.5 43.4 44 1 44 8 45.9 Operating income 82 5 132.3 131.4 136.4 1414 Reorganization expense 6.7 Amortization of goodwill 30.5 21.8 21.5 21.2 215 Interest expense, net 71.0 56.6 Toy Biz performance plan expenses 55.0 Equity in net (loss) income in unconsolidated subsidiaries (0.1) 02) 22 3.2 4.4 [Loss) income before taxes (25.8) 42.3 (7 5) 57.4 67.7 Provision for Income taxes 69 24,8 4.6 20.8 34. 1 (Loans] before minonty interest 132.7 17.5 (12.1) 27.6 3316 Minority Interest in Toy Biz 3.0 Net (loss) income (35.7) 17.5 (12 1) 27.6 33.6 CASH FLOW DATA Provision for deferred taxes 508 Undistributed comings in 02 (2:2) 13.2) 4.41 brookwood subakclarins Minority interest In Toy Biz earnings 3.0 Change In net working capital (75 4) (11.5] 44 3 (42 0) 20 Capital expenditures (67.41 (47.4) (48 71 BALANCE SHEET DATA Cash balance $2.0 Goodwill and other intangbies 510.7 404.0 485.1 145 2 425 4 Total BANKS 1,2133 1213 5 1,234.5 1.2006 95.0 0128 1700 Ffinanced kane Him cibi Total copit Wilmington Delaware, Jarainly ha, Verynts/ Marvel.pat + Bankruptcy and Restructuring at Marvel Entertainment Group Exhibit 10 Selected Financial Market Data January 31, 1997 Yields on U.S. Treasury Bills, Notes, and Bonds 3 month 5.04% 6 month 5.10 1-year 5 62 2-year 5-year 10-year 1 0 your inflation Indexed bonds" 3.33 30 your 6.85 Yields on Long-term Corporate Bonds An F.6 Interest Rates Federal Funds 5.18 3-month Commercial Paper 5.45 3 month Certificate of Deposit S.A Prima Rate Marvel Entertainment Group Awet Beta The equity late god to cobuling the al lots na minand ming daily des him W

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance