Answered step by step

Verified Expert Solution

Question

1 Approved Answer

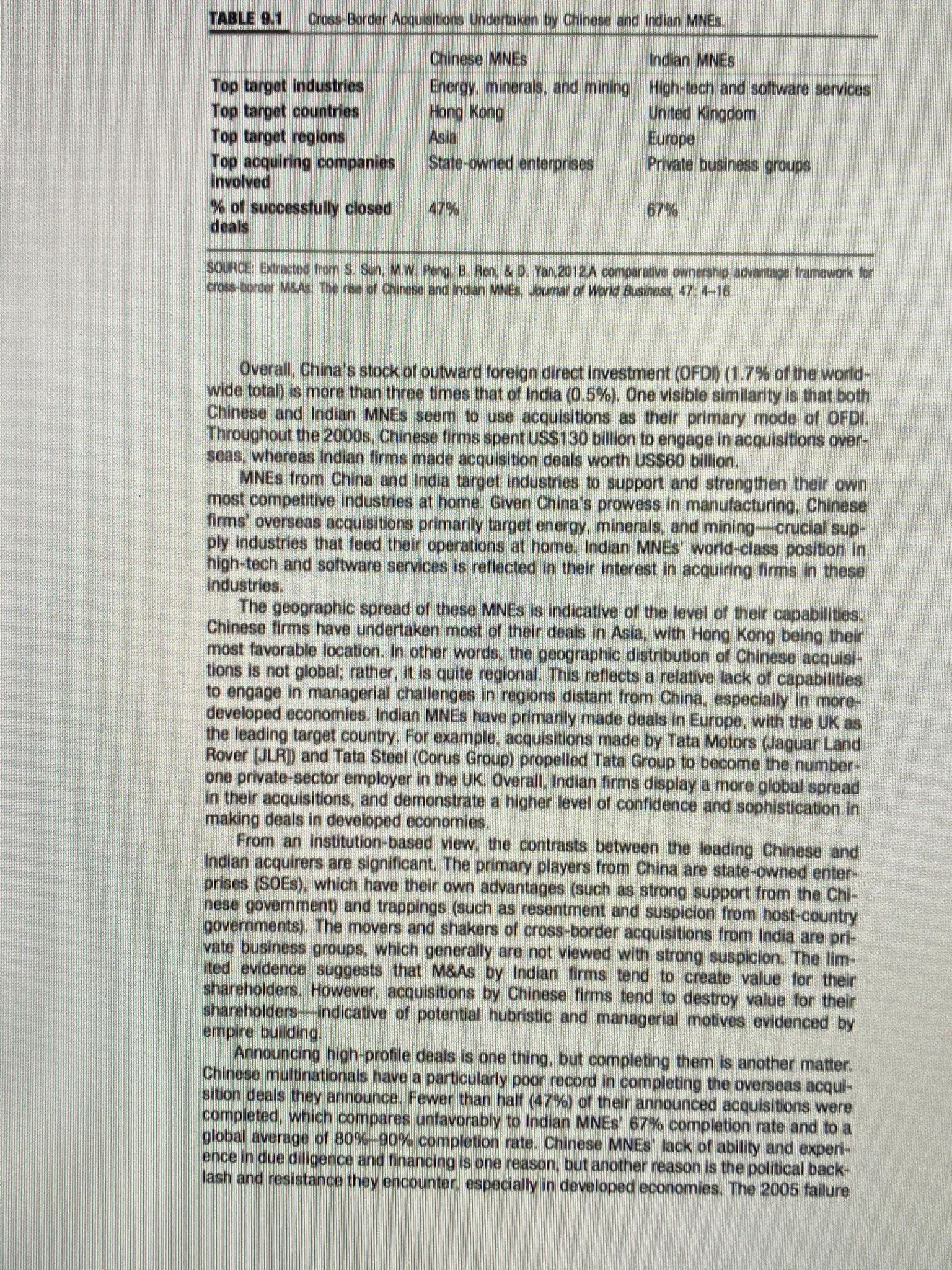

Why have firms from emerging economies such as China and India significantly expanded their international footprint? Why do they focus on industries related to their

- Why have firms from emerging economies such as China and India significantly expanded their international footprint?

- Why do they focus on industries related to their existing areas of excellence?

- Why are they interested in using acquisitions as a mode of entry?

- How successful (or terrible) have their acquisitions been?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Marketing & Export Management

Authors: Gerald Albaum, Edwin Duerr

7th edition

273743880, 978-8131791189, 8131791181, 978-0273743880