Answered step by step

Verified Expert Solution

Question

1 Approved Answer

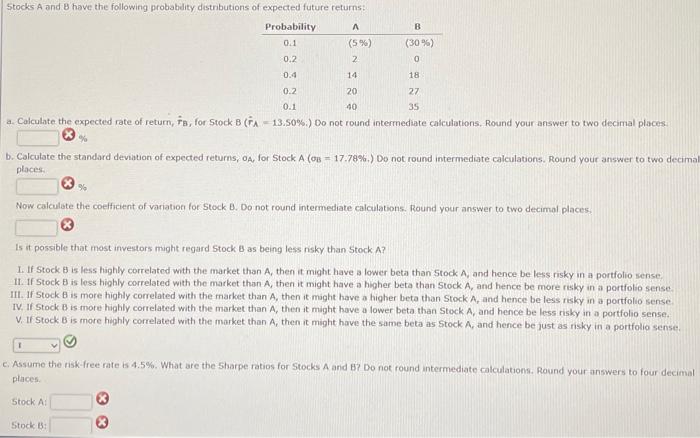

Will upvote correct answers . I need help solving subparts a. - c. a. Calculate the expected rate of return, rB, for Stock B(rA=13.50% )

Will upvote correct answers . I need help solving subparts a. - c.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance In Theory And Practice

Authors: Holley Ulbrich

2nd Edition

041558597X, 978-0415585972