Answered step by step

Verified Expert Solution

Question

1 Approved Answer

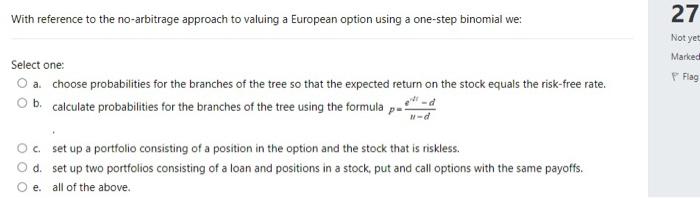

With reference to the no-arbitrage approach to valuing a European option using a one-step binomial we: 27 Not yet Marked Flag Select one: O a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Pocket CIO The Guide To Successful IT Asset Management Get To Grips With The Fundamentals Of IT Asset Management Software Asset Management And Software License Compliance Audits With This Guide

Authors: Phara Estime McLachlan

1st Edition

1783001003, 978-1783001002