Answered step by step

Verified Expert Solution

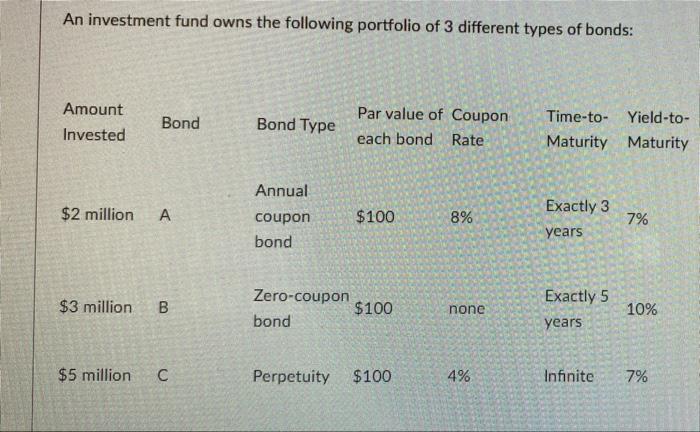

Question

1 Approved Answer

Without considering the convexity effect, what is the approximate percentage portfolio's value change if the portfolio's yield decreases by 50 basis points? Use the formula

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance A Quantitative Introduction Volume 2

Authors: Piotr Staszkiewicz, Lucia Staszkiewicz

1st Edition

0128027975, 978-0128027974