Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Words are clear to see. Thanks Exercise 2 Let Sx denote the price of a give stock on the kth day (k > 1) and

Words are clear to see. Thanks

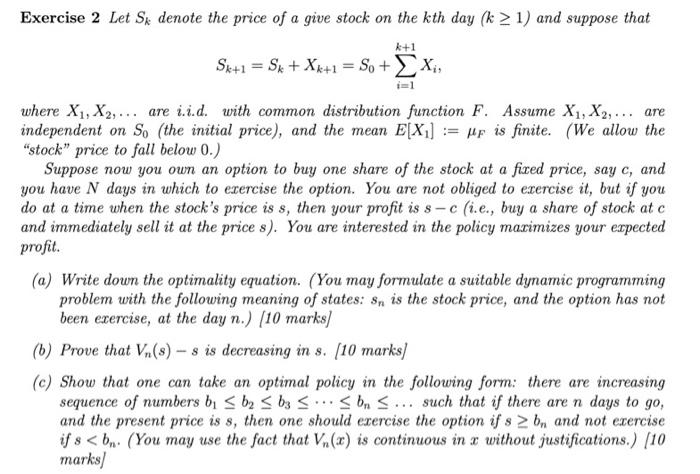

Exercise 2 Let Sx denote the price of a give stock on the kth day (k > 1) and suppose that k+1 S+1 = Sx + Xx+1 = So + x, where X1, X2,... are i.i.d. with common distribution function F. Assume X1, X2,... are independent on S, (the initial price), and the mean E[X] := up is finite. (We allow the "stock" price to fall below 0.) Suppose now you own an option to buy one share of the stock at a fixed price, say c, and you have N days in which to exercise the option. You are not obliged to exercise it, but if you do at a time when the stock's price is s, then your profit is s - c (i.e., buy a share of stock at c and immediately sell it at the price 8). You are interested in the policy marimizes your expected profit. (a) Write down the optimality equation. (You may formulate a suitable dynamic programming problem with the following meaning of states: sm is the stock price, and the option has not been exercise, at the day n.) (10 marks] (6) Prove that Vn(8) - s is decreasing in s. (10 marks (c) Show that one can take an optimal policy in the following form: there are increasing sequence of numbers b. 5 b2 1) and suppose that k+1 S+1 = Sx + Xx+1 = So + x, where X1, X2,... are i.i.d. with common distribution function F. Assume X1, X2,... are independent on S, (the initial price), and the mean E[X] := up is finite. (We allow the "stock" price to fall below 0.) Suppose now you own an option to buy one share of the stock at a fixed price, say c, and you have N days in which to exercise the option. You are not obliged to exercise it, but if you do at a time when the stock's price is s, then your profit is s - c (i.e., buy a share of stock at c and immediately sell it at the price 8). You are interested in the policy marimizes your expected profit. (a) Write down the optimality equation. (You may formulate a suitable dynamic programming problem with the following meaning of states: sm is the stock price, and the option has not been exercise, at the day n.) (10 marks] (6) Prove that Vn(8) - s is decreasing in s. (10 marks (c) Show that one can take an optimal policy in the following form: there are increasing sequence of numbers b. 5 b2 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started