Answered step by step

Verified Expert Solution

Question

1 Approved Answer

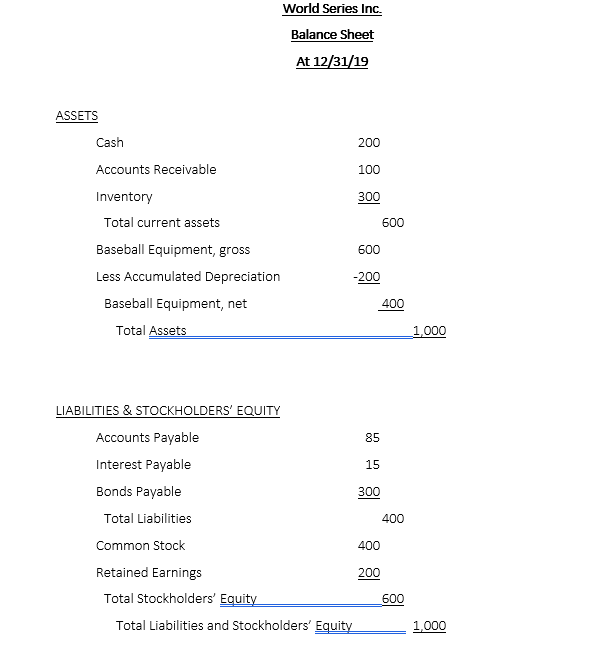

World Series Inc. Balance Sheet At 12/31/19 ASSETS begin{tabular}{ll} Cash & 200 Accounts Receivable & 100 Inventory & 300 Total current assets

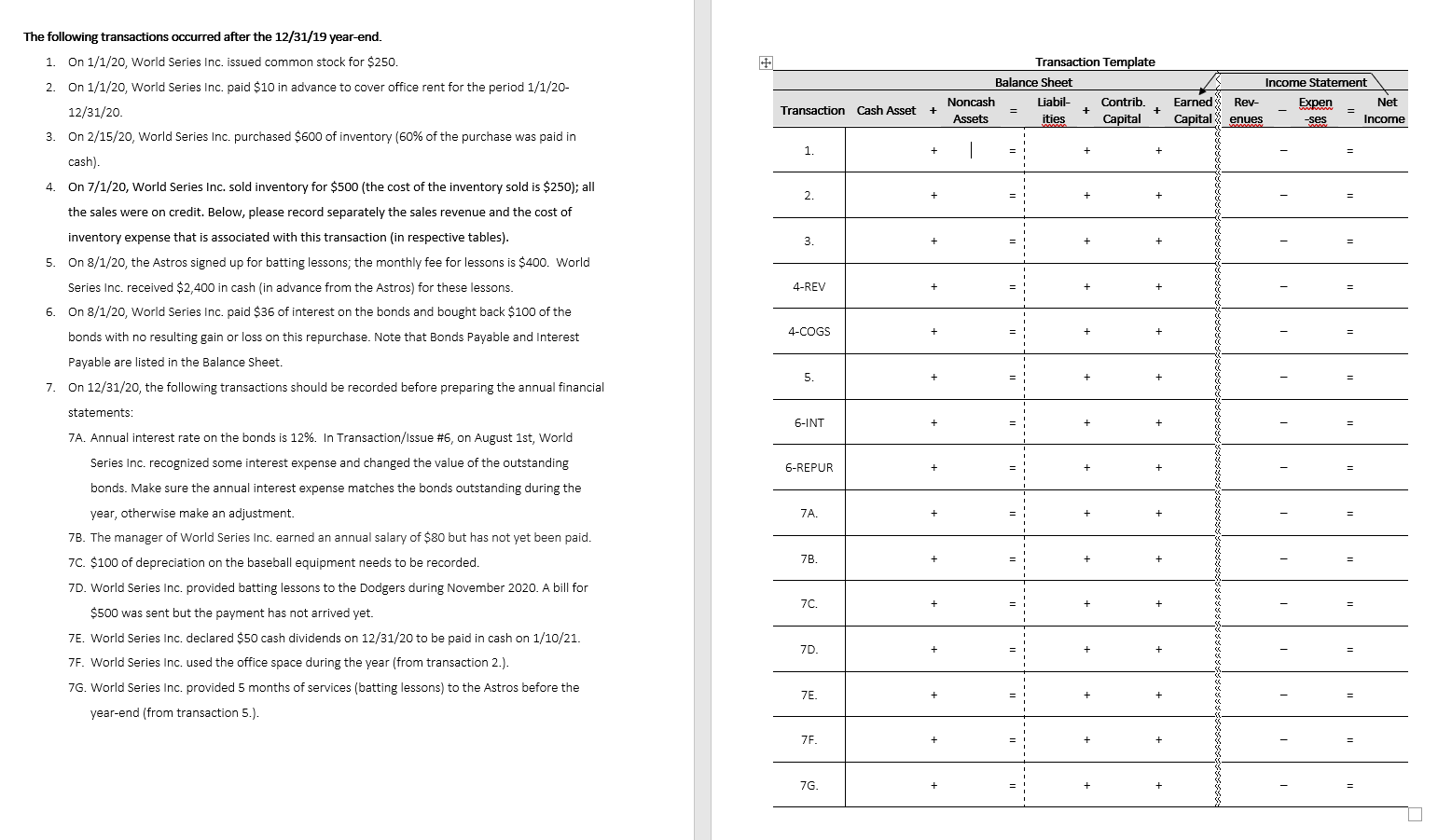

World Series Inc. Balance Sheet At 12/31/19 ASSETS \begin{tabular}{ll} Cash & 200 \\ Accounts Receivable & 100 \\ Inventory & 300 \\ Total current assets & 600 \\ Baseball Equipment, gross & 600 \\ Less Accumulated Depreciation & 200 \\ Baseball Equipment, net & 400 \\ Total Assets \end{tabular} LIABILITIES&STOCKHOLDERSEQUITY \begin{tabular}{lc} Accounts Payable & 85 \\ Interest Payable & 15 \\ Bonds Payable & 300 \\ Total Liabilities & 400 \\ Common Stock & 400 \\ Retained Earnings & 200 \\ Total Stockholders' Equity \end{tabular} Total Liabilities and Stockholders' Equity 1,000 The following transactions occurred after the 12/31/19 year-end. 1. On 1/1/20, World Series Inc. issued common stock for $250. 2. On 1/1/20, World Series Inc. paid $10 in advance to cover office rent for the period 1/1/20 12/31/20. 3. On 2/15/20, World Series Inc. purchased $600 of inventory ( 60% of the purchase was paid in cash). 4. On 7/1/20, World Series Inc. sold inventory for $500 (the cost of the inventory sold is $250 ); all the sales were on credit. Below, please record separately the sales revenue and the cost of inventory expense that is associated with this transaction (in respective tables). 5. On 8/1/20, the Astros signed up for batting lessons; the monthly fee for lessons is $400. World Series Inc. received $2,400 in cash (in advance from the Astros) for these lessons. 6. On 8/1/20, World Series Inc. paid $36 of interest on the bonds and bought back $100 of the bonds with no resulting gain or loss on this repurchase. Note that Bonds Payable and Interest Payable are listed in the Balance Sheet. 7. On 12/31/20, the following transactions should be recorded before preparing the annual financial statements: 7A. Annual interest rate on the bonds is 12%. In Transaction/Issue \#6, on August 1st, World Series Inc. recognized some interest expense and changed the value of the outstanding bonds. Make sure the annual interest expense matches the bonds outstanding during the year, otherwise make an adjustment. 7B. The manager of World Series Inc. earned an annual salary of $80 but has not yet been paid. 7C. $100 of depreciation on the baseball equipment needs to be recorded. 7D. World Series Inc. provided batting lessons to the Dodgers during November 2020. A bill for $500 was sent but the payment has not arrived yet. 7E. World Series Inc. declared $50 cash dividends on 12/31/20 to be paid in cash on 1/10/21. 7F. World Series Inc. used the office space during the year (from transaction 2.). 7G. World Series Inc. provided 5 months of services (batting lessons) to the Astros before the year-end (from transaction 5.). World Series Inc. Balance Sheet At 12/31/19 ASSETS \begin{tabular}{ll} Cash & 200 \\ Accounts Receivable & 100 \\ Inventory & 300 \\ Total current assets & 600 \\ Baseball Equipment, gross & 600 \\ Less Accumulated Depreciation & 200 \\ Baseball Equipment, net & 400 \\ Total Assets \end{tabular} LIABILITIES&STOCKHOLDERSEQUITY \begin{tabular}{lc} Accounts Payable & 85 \\ Interest Payable & 15 \\ Bonds Payable & 300 \\ Total Liabilities & 400 \\ Common Stock & 400 \\ Retained Earnings & 200 \\ Total Stockholders' Equity \end{tabular} Total Liabilities and Stockholders' Equity 1,000 The following transactions occurred after the 12/31/19 year-end. 1. On 1/1/20, World Series Inc. issued common stock for $250. 2. On 1/1/20, World Series Inc. paid $10 in advance to cover office rent for the period 1/1/20 12/31/20. 3. On 2/15/20, World Series Inc. purchased $600 of inventory ( 60% of the purchase was paid in cash). 4. On 7/1/20, World Series Inc. sold inventory for $500 (the cost of the inventory sold is $250 ); all the sales were on credit. Below, please record separately the sales revenue and the cost of inventory expense that is associated with this transaction (in respective tables). 5. On 8/1/20, the Astros signed up for batting lessons; the monthly fee for lessons is $400. World Series Inc. received $2,400 in cash (in advance from the Astros) for these lessons. 6. On 8/1/20, World Series Inc. paid $36 of interest on the bonds and bought back $100 of the bonds with no resulting gain or loss on this repurchase. Note that Bonds Payable and Interest Payable are listed in the Balance Sheet. 7. On 12/31/20, the following transactions should be recorded before preparing the annual financial statements: 7A. Annual interest rate on the bonds is 12%. In Transaction/Issue \#6, on August 1st, World Series Inc. recognized some interest expense and changed the value of the outstanding bonds. Make sure the annual interest expense matches the bonds outstanding during the year, otherwise make an adjustment. 7B. The manager of World Series Inc. earned an annual salary of $80 but has not yet been paid. 7C. $100 of depreciation on the baseball equipment needs to be recorded. 7D. World Series Inc. provided batting lessons to the Dodgers during November 2020. A bill for $500 was sent but the payment has not arrived yet. 7E. World Series Inc. declared $50 cash dividends on 12/31/20 to be paid in cash on 1/10/21. 7F. World Series Inc. used the office space during the year (from transaction 2.). 7G. World Series Inc. provided 5 months of services (batting lessons) to the Astros before the year-end (from transaction 5.)

World Series Inc. Balance Sheet At 12/31/19 ASSETS \begin{tabular}{ll} Cash & 200 \\ Accounts Receivable & 100 \\ Inventory & 300 \\ Total current assets & 600 \\ Baseball Equipment, gross & 600 \\ Less Accumulated Depreciation & 200 \\ Baseball Equipment, net & 400 \\ Total Assets \end{tabular} LIABILITIES&STOCKHOLDERSEQUITY \begin{tabular}{lc} Accounts Payable & 85 \\ Interest Payable & 15 \\ Bonds Payable & 300 \\ Total Liabilities & 400 \\ Common Stock & 400 \\ Retained Earnings & 200 \\ Total Stockholders' Equity \end{tabular} Total Liabilities and Stockholders' Equity 1,000 The following transactions occurred after the 12/31/19 year-end. 1. On 1/1/20, World Series Inc. issued common stock for $250. 2. On 1/1/20, World Series Inc. paid $10 in advance to cover office rent for the period 1/1/20 12/31/20. 3. On 2/15/20, World Series Inc. purchased $600 of inventory ( 60% of the purchase was paid in cash). 4. On 7/1/20, World Series Inc. sold inventory for $500 (the cost of the inventory sold is $250 ); all the sales were on credit. Below, please record separately the sales revenue and the cost of inventory expense that is associated with this transaction (in respective tables). 5. On 8/1/20, the Astros signed up for batting lessons; the monthly fee for lessons is $400. World Series Inc. received $2,400 in cash (in advance from the Astros) for these lessons. 6. On 8/1/20, World Series Inc. paid $36 of interest on the bonds and bought back $100 of the bonds with no resulting gain or loss on this repurchase. Note that Bonds Payable and Interest Payable are listed in the Balance Sheet. 7. On 12/31/20, the following transactions should be recorded before preparing the annual financial statements: 7A. Annual interest rate on the bonds is 12%. In Transaction/Issue \#6, on August 1st, World Series Inc. recognized some interest expense and changed the value of the outstanding bonds. Make sure the annual interest expense matches the bonds outstanding during the year, otherwise make an adjustment. 7B. The manager of World Series Inc. earned an annual salary of $80 but has not yet been paid. 7C. $100 of depreciation on the baseball equipment needs to be recorded. 7D. World Series Inc. provided batting lessons to the Dodgers during November 2020. A bill for $500 was sent but the payment has not arrived yet. 7E. World Series Inc. declared $50 cash dividends on 12/31/20 to be paid in cash on 1/10/21. 7F. World Series Inc. used the office space during the year (from transaction 2.). 7G. World Series Inc. provided 5 months of services (batting lessons) to the Astros before the year-end (from transaction 5.). World Series Inc. Balance Sheet At 12/31/19 ASSETS \begin{tabular}{ll} Cash & 200 \\ Accounts Receivable & 100 \\ Inventory & 300 \\ Total current assets & 600 \\ Baseball Equipment, gross & 600 \\ Less Accumulated Depreciation & 200 \\ Baseball Equipment, net & 400 \\ Total Assets \end{tabular} LIABILITIES&STOCKHOLDERSEQUITY \begin{tabular}{lc} Accounts Payable & 85 \\ Interest Payable & 15 \\ Bonds Payable & 300 \\ Total Liabilities & 400 \\ Common Stock & 400 \\ Retained Earnings & 200 \\ Total Stockholders' Equity \end{tabular} Total Liabilities and Stockholders' Equity 1,000 The following transactions occurred after the 12/31/19 year-end. 1. On 1/1/20, World Series Inc. issued common stock for $250. 2. On 1/1/20, World Series Inc. paid $10 in advance to cover office rent for the period 1/1/20 12/31/20. 3. On 2/15/20, World Series Inc. purchased $600 of inventory ( 60% of the purchase was paid in cash). 4. On 7/1/20, World Series Inc. sold inventory for $500 (the cost of the inventory sold is $250 ); all the sales were on credit. Below, please record separately the sales revenue and the cost of inventory expense that is associated with this transaction (in respective tables). 5. On 8/1/20, the Astros signed up for batting lessons; the monthly fee for lessons is $400. World Series Inc. received $2,400 in cash (in advance from the Astros) for these lessons. 6. On 8/1/20, World Series Inc. paid $36 of interest on the bonds and bought back $100 of the bonds with no resulting gain or loss on this repurchase. Note that Bonds Payable and Interest Payable are listed in the Balance Sheet. 7. On 12/31/20, the following transactions should be recorded before preparing the annual financial statements: 7A. Annual interest rate on the bonds is 12%. In Transaction/Issue \#6, on August 1st, World Series Inc. recognized some interest expense and changed the value of the outstanding bonds. Make sure the annual interest expense matches the bonds outstanding during the year, otherwise make an adjustment. 7B. The manager of World Series Inc. earned an annual salary of $80 but has not yet been paid. 7C. $100 of depreciation on the baseball equipment needs to be recorded. 7D. World Series Inc. provided batting lessons to the Dodgers during November 2020. A bill for $500 was sent but the payment has not arrived yet. 7E. World Series Inc. declared $50 cash dividends on 12/31/20 to be paid in cash on 1/10/21. 7F. World Series Inc. used the office space during the year (from transaction 2.). 7G. World Series Inc. provided 5 months of services (batting lessons) to the Astros before the year-end (from transaction 5.) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: J. David Spiceland, James Sepe, Mark Nelson

6th edition

978-0077328894, 71313974, 9780077395810, 77328892, 9780071313971, 77395816, 978-0077400163