Answered step by step

Verified Expert Solution

Question

1 Approved Answer

World Wide Paper company 2006 How to calculate IRR and NPV? Please Show Work!!! Worldwide Paper Company In December 2006, Bob Prescott, the controller for

World Wide Paper company 2006

How to calculate IRR and NPV?

Please Show Work!!!

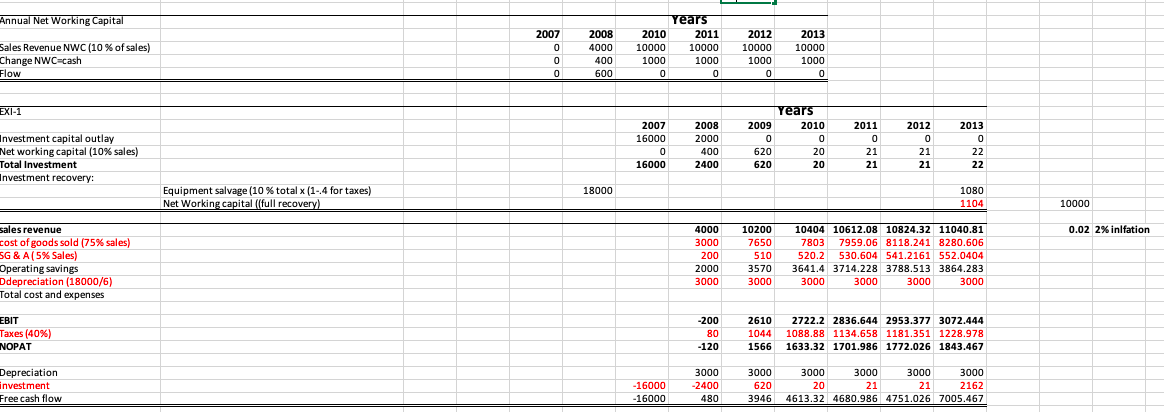

Worldwide Paper Company In December 2006, Bob Prescott, the controller for the Blue Ridge Mill, was consid- ering the addition of a new on-site longwood woodyard. The addition would have two primary benefits: to eliminate the need to purchase shortwood from an outside sup- plier and create the opportunity to sell shortwood on the open market as a new mar- ket for Worldwide Paper Company (WPC). The new woodyard would allow the Blue Ridge Mill not only to reduce its operating costs but also to increase its revenues. The proposed woodyard utilized new technology that allowed tree-length logs, called long- wood, to be processed directly, whereas the current process required shortwood, which had to be purchased from the Shenandoah Mill. This nearby mill, owned by a com- petitor, had excess capacity that allowed it to produce more shortwood than it needed for its own pulp production. The excess was sold to several different mills, including the Blue Ridge Mill. Thus adding the new longwood equipment would mean that Prescott would no longer need to use the Shenandoah Mill as a shortwood supplier and that the Blue Ridge Mill would instead compete with the Shenandoah Mill by selling on the shortwood market. The question for Prescott was whether these expected benefits were enough to justify the $18 million capital outlay plus the incremental investment in working capital over the six-year life of the investment Construction would start within a few months, and the investment outlay would be spent over two calendar years: $16 million in 2007 and the remaining $2 million in 2008. When the new woodyard began operating in 2008, it would significantly reduce the operating costs of the mill. These operating savings would come mostly from the difference in the cost of producing shortwood on-site versus buying it on the open mar- ket and were estimated to be $2.0 million for 2008 and $3.5 million per year thereafter. Prescott also planned on taking advantage of the excess production capacity afforded by the new facility by selling shortwood on the open market as soon as pos- sible. For 2008, he expected to show revenues of approximately $4 million, as the facility came on-line and began to break into the new market. He expected shortwood sales to reach $10 million in 2009 and continue at the $10 million level through 2013. Annual Net Working Capital Sales Revenue NWC (10% of sales) Change NWC cash Flow 2007 0 0 0 2008 4000 400 600 Years 2010 2011 10000 10000 1000 1000 0 0 2012 10000 1000 0 2013 10000 1000 0 EXI-1 Investment capital outlay Net working capital (10% sales) Total Investment Investment recovery: 2007 16000 0 16000 2008 2000 400 2400 Years 2009 2010 0 0 0 620 20 620 20 2011 0 21 21 2012 0 21 21 2013 0 22 22 18000 Equipment salvage (10 % total (1-4 for taxes) Net Working capital (full recovery) ( 1080 1104 10000 0.02 2% inlfation sales revenue cost of goods sold (75% sales) SG & A (5% Sales) Operating savings Ddepreciation (18000/6) Total cost and expenses 4000 3000 200 2000 3000 10200 7650 510 3570 3000 10404 10612.08 10824.32 11040.81 7803 7959.06 8118.241 8280.606 520.2 530.604 541.2161 552.0404 3641.4 3714.228 3788.513 3864.283 3000 3000 3000 3000 EBIT Taxes (40%) NOPAT -200 80 -120 2610 2722.2 2836.644 2953.377 3072.444 1044 1088.88 1134.658 1181.351 1228.978 1566 1633.32 1701.986 1772.026 1843.467 Depreciation investment Free cash flow - 16000 - 16000 3000 -2400 480 3000 620 3946 3000 3000 3000 3000 20 21 21 2162 4613.32 4680.986 4751.026 7005.467 Worldwide Paper Company In December 2006, Bob Prescott, the controller for the Blue Ridge Mill, was consid- ering the addition of a new on-site longwood woodyard. The addition would have two primary benefits: to eliminate the need to purchase shortwood from an outside sup- plier and create the opportunity to sell shortwood on the open market as a new mar- ket for Worldwide Paper Company (WPC). The new woodyard would allow the Blue Ridge Mill not only to reduce its operating costs but also to increase its revenues. The proposed woodyard utilized new technology that allowed tree-length logs, called long- wood, to be processed directly, whereas the current process required shortwood, which had to be purchased from the Shenandoah Mill. This nearby mill, owned by a com- petitor, had excess capacity that allowed it to produce more shortwood than it needed for its own pulp production. The excess was sold to several different mills, including the Blue Ridge Mill. Thus adding the new longwood equipment would mean that Prescott would no longer need to use the Shenandoah Mill as a shortwood supplier and that the Blue Ridge Mill would instead compete with the Shenandoah Mill by selling on the shortwood market. The question for Prescott was whether these expected benefits were enough to justify the $18 million capital outlay plus the incremental investment in working capital over the six-year life of the investment Construction would start within a few months, and the investment outlay would be spent over two calendar years: $16 million in 2007 and the remaining $2 million in 2008. When the new woodyard began operating in 2008, it would significantly reduce the operating costs of the mill. These operating savings would come mostly from the difference in the cost of producing shortwood on-site versus buying it on the open mar- ket and were estimated to be $2.0 million for 2008 and $3.5 million per year thereafter. Prescott also planned on taking advantage of the excess production capacity afforded by the new facility by selling shortwood on the open market as soon as pos- sible. For 2008, he expected to show revenues of approximately $4 million, as the facility came on-line and began to break into the new market. He expected shortwood sales to reach $10 million in 2009 and continue at the $10 million level through 2013. Annual Net Working Capital Sales Revenue NWC (10% of sales) Change NWC cash Flow 2007 0 0 0 2008 4000 400 600 Years 2010 2011 10000 10000 1000 1000 0 0 2012 10000 1000 0 2013 10000 1000 0 EXI-1 Investment capital outlay Net working capital (10% sales) Total Investment Investment recovery: 2007 16000 0 16000 2008 2000 400 2400 Years 2009 2010 0 0 0 620 20 620 20 2011 0 21 21 2012 0 21 21 2013 0 22 22 18000 Equipment salvage (10 % total (1-4 for taxes) Net Working capital (full recovery) ( 1080 1104 10000 0.02 2% inlfation sales revenue cost of goods sold (75% sales) SG & A (5% Sales) Operating savings Ddepreciation (18000/6) Total cost and expenses 4000 3000 200 2000 3000 10200 7650 510 3570 3000 10404 10612.08 10824.32 11040.81 7803 7959.06 8118.241 8280.606 520.2 530.604 541.2161 552.0404 3641.4 3714.228 3788.513 3864.283 3000 3000 3000 3000 EBIT Taxes (40%) NOPAT -200 80 -120 2610 2722.2 2836.644 2953.377 3072.444 1044 1088.88 1134.658 1181.351 1228.978 1566 1633.32 1701.986 1772.026 1843.467 Depreciation investment Free cash flow - 16000 - 16000 3000 -2400 480 3000 620 3946 3000 3000 3000 3000 20 21 21 2162 4613.32 4680.986 4751.026 7005.467Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Real Estate Finance

Authors: Walt Huber, Levin P. Messick

5th Edition

0916772438, 9780916772437