Answered step by step

Verified Expert Solution

Question

1 Approved Answer

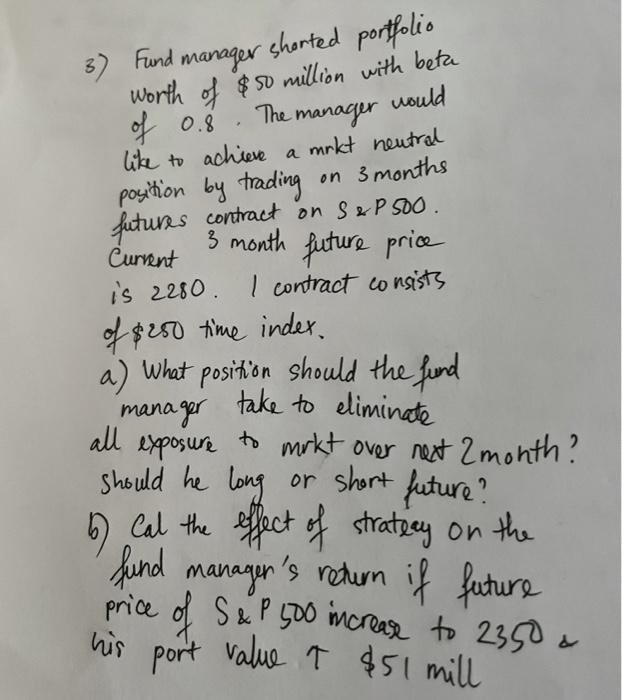

worth of $50 million with beta Fund shorted portfolio I manager The manager - of 0.8 would like to achieve a mrkt neutral position by

worth of $50 million with beta Fund shorted portfolio I manager The manager - of 0.8 would like to achieve a mrkt neutral position by trading on 3 months futures contract on S&P 500 Current is 2280. I contract consists 3 month future price of $250 time index. a) What position should the fund manager all exposure to mrkt over next 2 month? should he long or short Cal the effect of strateay on the take to eliminate or short future? fund manager's return if future price of S&P 500 increase to 2350 his port value o $51 mill worth of $50 million with beta Fund shorted portfolio I manager The manager - of 0.8 would like to achieve a mrkt neutral position by trading on 3 months futures contract on S&P 500 Current is 2280. I contract consists 3 month future price of $250 time index. a) What position should the fund manager all exposure to mrkt over next 2 month? should he long or short Cal the effect of strateay on the take to eliminate or short future? fund manager's return if future price of S&P 500 increase to 2350 his port value o $51 mill

worth of $50 million with beta Fund shorted portfolio I manager The manager - of 0.8 would like to achieve a mrkt neutral position by trading on 3 months futures contract on S&P 500 Current is 2280. I contract consists 3 month future price of $250 time index. a) What position should the fund manager all exposure to mrkt over next 2 month? should he long or short Cal the effect of strateay on the take to eliminate or short future? fund manager's return if future price of S&P 500 increase to 2350 his port value o $51 mill worth of $50 million with beta Fund shorted portfolio I manager The manager - of 0.8 would like to achieve a mrkt neutral position by trading on 3 months futures contract on S&P 500 Current is 2280. I contract consists 3 month future price of $250 time index. a) What position should the fund manager all exposure to mrkt over next 2 month? should he long or short Cal the effect of strateay on the take to eliminate or short future? fund manager's return if future price of S&P 500 increase to 2350 his port value o $51 mill

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Global Finance And Development

Authors: David Hudson

1st Edition

0415436354, 978-0415436359