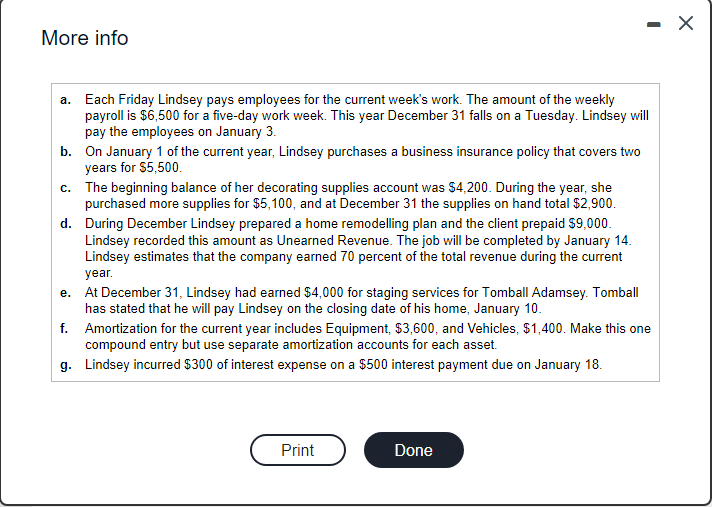

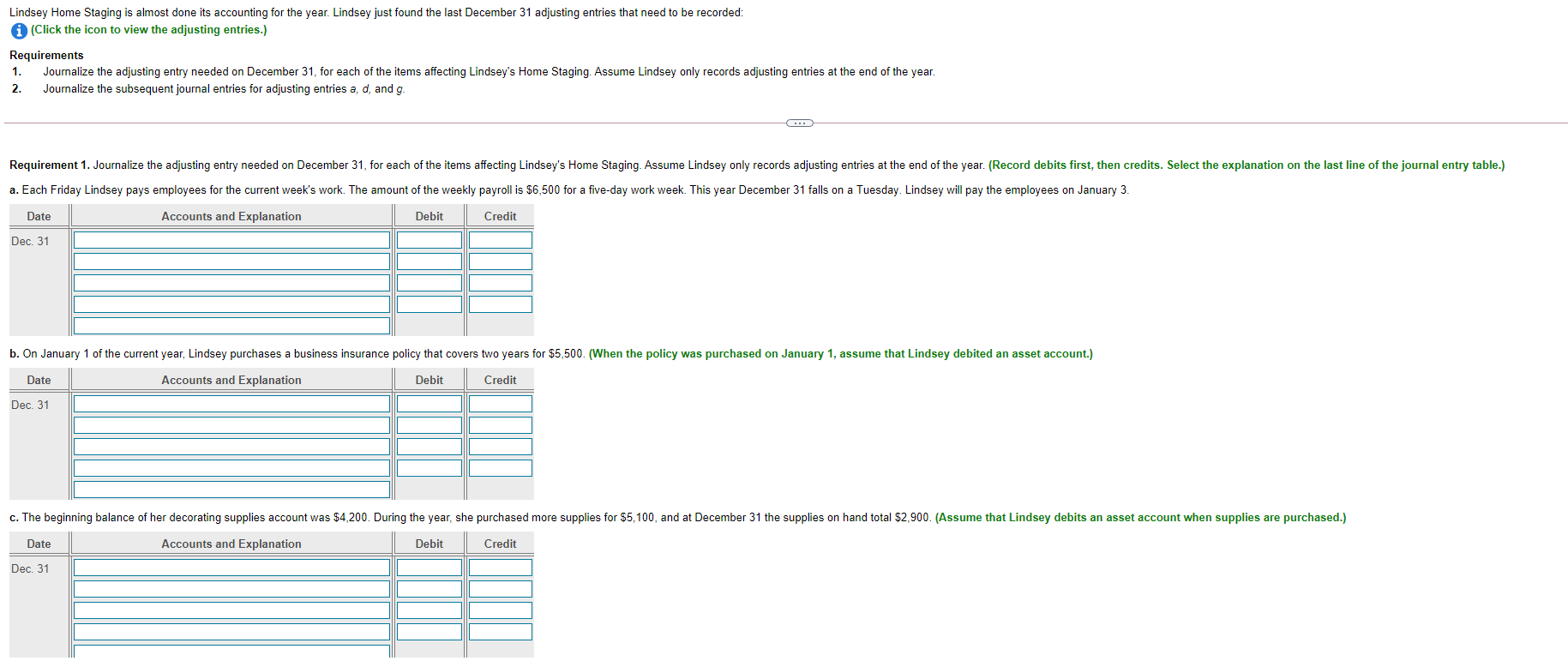

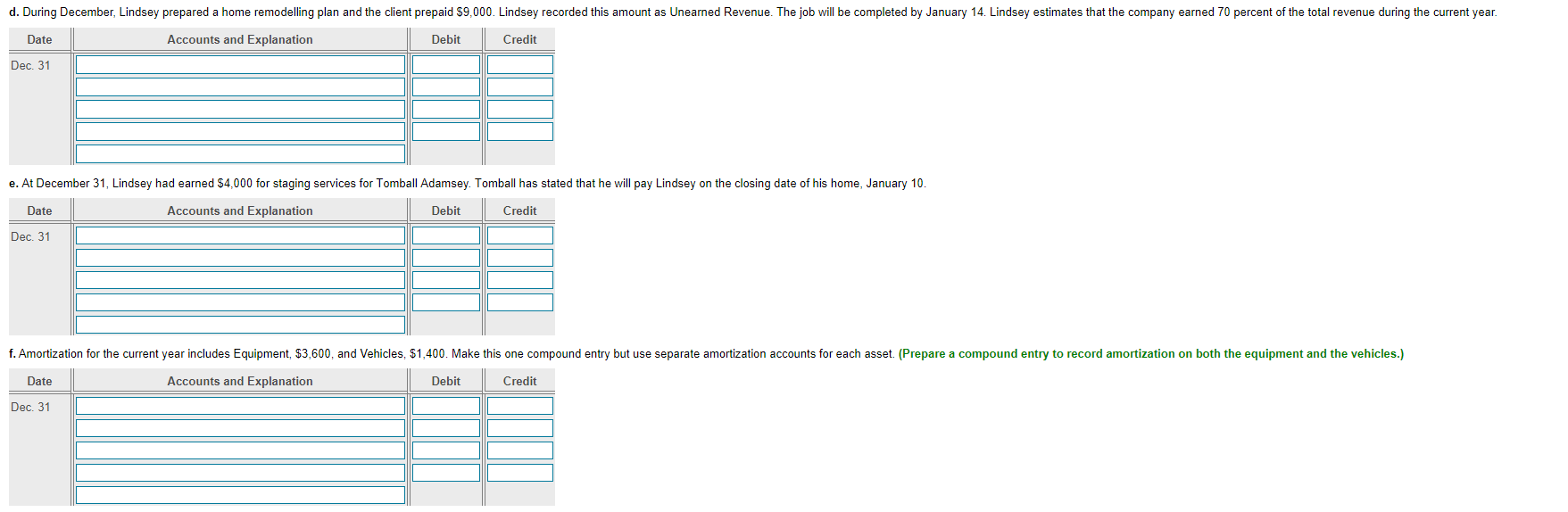

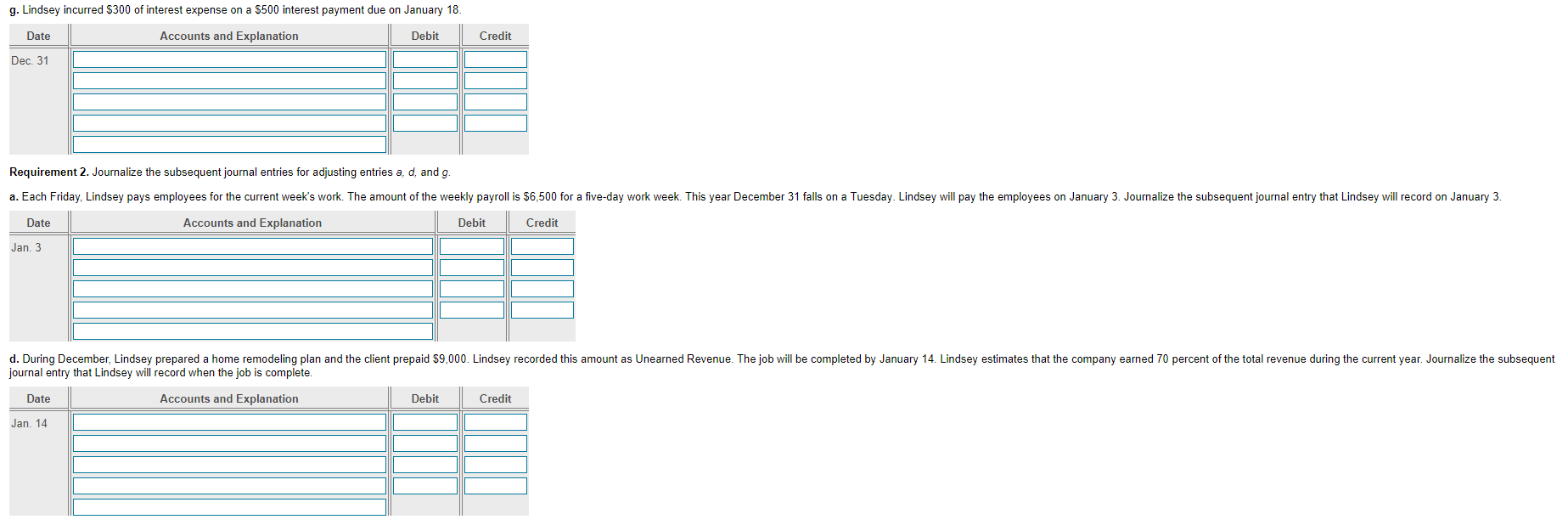

- X More info a. Each Friday Lindsey pays employees for the current week's work. The amount of the weekly payroll is $6,500 for a five-day work week. This year December 31 falls on a Tuesday. Lindsey will pay the employees on January 3. b. On January 1 of the current year, Lindsey purchases a business insurance policy that covers two years for $5,500 C. The beginning balance of her decorating supplies account was $4,200. During the year, she purchased more supplies for $5,100, and at December 31 the supplies on hand total $2,900. d. During December Lindsey prepared a home remodelling plan and the client prepaid $9,000. Lindsey recorded this amount as Unearned Revenue. The job will be completed by January 14. Lindsey estimates that the company earned 70 percent of the total revenue during the current year. e. At December 31, Lindsey had earned $4,000 for staging services for Tomball Adamsey. Tomball has stated that he will pay Lindsey on the closing date of his home, January 10. f. Amortization for the current year includes Equipment, $3,600, and Vehicles, $1,400. Make this one compound entry but use separate amortization accounts for each asset. g. Lindsey incurred $300 of interest expense on a $500 interest payment due on January 18. Print Done Lindsey Home Staging is almost done its accounting for the year. Lindsey just found the last December 31 adjusting entries that need to be recorded: (Click the icon to view the adjusting entries.) Requirements 1. Journalize the adjusting entry needed on December 31, for each of the items affecting Lindsey's Home Staging. Assume Lindsey only records adjusting entries at the end of the year. 2. Journalize the subsequent journal entries for adjusting entries a, d, and g. .. Requirement 1. Journalize the adjusting entry needed on December 31, for each of the items affecting Lindsey's Home Staging. Assume Lindsey only records adjusting entries at the end of the year. (Record debits first, then credits. Select the explanation on the last line of the journal entry table.) a. Each Friday Lindsey pays employees for the current week's work. The amount of the weekly payroll is $6,500 for a five-day work week. This year December 31 falls on a Tuesday. Lindsey will pay the employees on January 3. Date Accounts and Explanation Debit Credit Dec. 31 b. On January 1 of the current year, Lindsey purchases a business insurance policy that covers two years for $5,500. (When the policy was purchased on January 1, assume that Lindsey debited an asset account.) Date Accounts and Explanation Debit Credit Dec. 31 c. The beginning balance of her decorating supplies account was $4,200. During the year, she purchased more supplies for $5,100, and at December 31 the supplies on hand total $2,900. (Assume that Lindsey debits an asset account when supplies are purchased.) Accounts and Explanation Debit Credit Date Dec. 31 d. During December, Lindsey prepared a home remodelling plan and the client prepaid $9,000. Lindsey recorded this amount as Unearned Revenue. The job will be completed by January 14. Lindsey estimates that the company earned 70 percent of the total revenue during the current year. Date Accounts and Explanation Debit Credit Dec. 31 e. At December 31, Lindsey had earned $4,000 for staging services for Tomball Adamsey. Tomball has stated that he will pay Lindsey on the closing date of his home, January 10. Date Accounts and Explanation Debit Credit Dec. 31 f. Amortization for the current year includes Equipment, $3,600, and Vehicles, $1,400. Make this one compound entry but use separate amortization accounts for each asset. (Prepare a compound entry to record amortization on both the equipment and the vehicles.) Date Accounts and Explanation Debit Credit Dec. 31 g. Lindsey incurred $300 of interest expense on a $500 interest payment due on January 18 Date Accounts and Explanation Debit Credit Dec. 31 Requirement 2. Journalize the subsequent journal entries for adjusting entries a, d, and g. a. Each Friday, Lindsey pays employees for the current week's work. The amount of the weekly payroll is $6,500 for a five-day work week. This year December 31 falls on a Tuesday. Lindsey will pay the employees on January 3. Journalize the subsequent journal entry that Lindsey will record on January 3. Date Accounts and Explanation Debit Credit Jan. 3 d. During December , Lindsey prepared a home remodeling plan and the client prepaid $9,000. Lindsey recorded this amount as Unearned Revenue. The job will be completed by January 14. Lindsey estimates that the company earned 70 percent of the total revenue during the current year. Journalize the subsequent journal entry that Lindsey will record when the job is complete. Date Accounts and Explanation Debit Credit Jan. 14 g. Lindsey incurred $300 of interest expense on a $500 interest payment due on January 18. Journalize the subsequent journal entry that Lindsey will record on January 18 Date Accounts and Explanation Debit Credit Jan. 18