Answered step by step

Verified Expert Solution

Question

1 Approved Answer

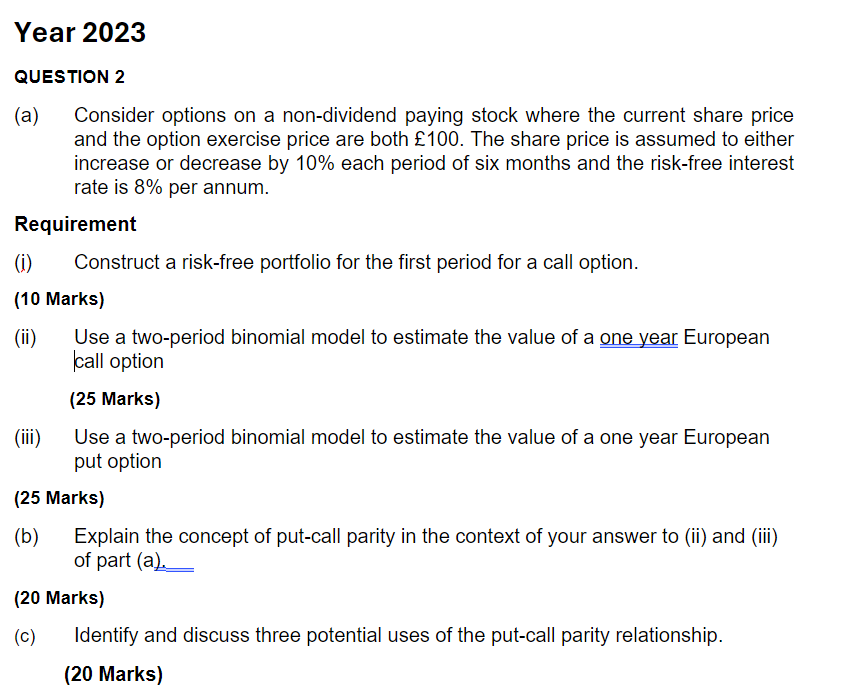

Year 2 0 2 3 QUESTION 2 ( a ) Consider options on a non - dividend paying stock where the current share price and

Year

QUESTION

a Consider options on a nondividend paying stock where the current share price

and the option exercise price are both The share price is assumed to either

increase or decrease by each period of six months and the riskfree interest

rate is per annum.

Requirement

i Construct a riskfree portfolio for the first period for a call option.

Marks

ii Use a twoperiod binomial model to estimate the value of a one year European

call option

Marks

iii Use a twoperiod binomial model to estimate the value of a one year European

put option

Marks

b Explain the concept of putcall parity in the context of your answer to ii and iii

of part a

Marks

c Identify and discuss three potential uses of the putcall parity relationship.

Marks

I have attached the solutions, please provide a step by step method to achieve the solutions seen attached, thanks.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment Analysis And Portfolio Management

Authors: Frank K. Reilly, Keith C. Brown

6th Edition

003025809X, 978-3540014386