You are an actuary in the SPIA product department at SLIC. Your boss, Lou Condor, VP-SPIA Product, is interested in examining the emerging mortality improvement

You are an actuary in the SPIA product department at SLIC. Your boss, Lou Condor, VP-SPIA Product, is interested in examining the emerging mortality improvement experience. Lou has asked you to join a special project team evaluating SLIC's possible responses. Refer to section 3.9 of the Case Study. (a) (1 point) Describe what SLIC's response(s) could be to the observed mortality improvement on the SPIA product. SLIC's CFO, Pierre LeGrouse, has expressed concern with the mortality improvement study received from the large consulting firm. He is skeptical of the increase in mortality improvement for older ages in light of emerging population mortality improvement declines. Pierre recommends a new SPIA mortality improvement assumption based on US population mortality improvement data with an experience observation period of the past 5 years. This new assumption contains much lower mortality improvement rates and includes negative mortality improvement for ages 30-45. Pierre also suggests extending his mortality improvement assumption to all of SLIC's products. (b) (3 points) Critique Pierre's recommended assumption for the SPIA product. (c) (2 points) Describe three considerations for using Pierre's recommended assumption for all other SLIC products. Lyon has two annuity acquisition targets that would be managed by SLIC if acquired: 1) Target 1: AnnCo, an SPDA writer that has a strong sales-oriented culture 2) Target 2: SPIA block to manage in combination with SLIC's small existing block (d) (3 points) (i) Explain two pros and two cons of acquiring each target. (ii) Recommend which target to pursue. Justify your recommendation.

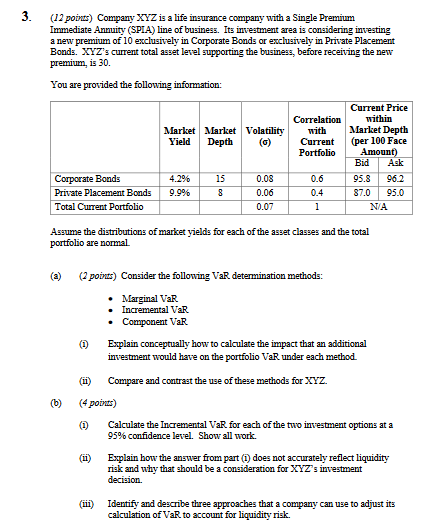

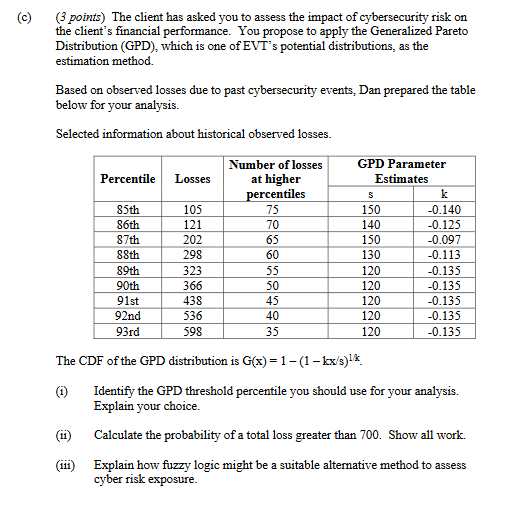

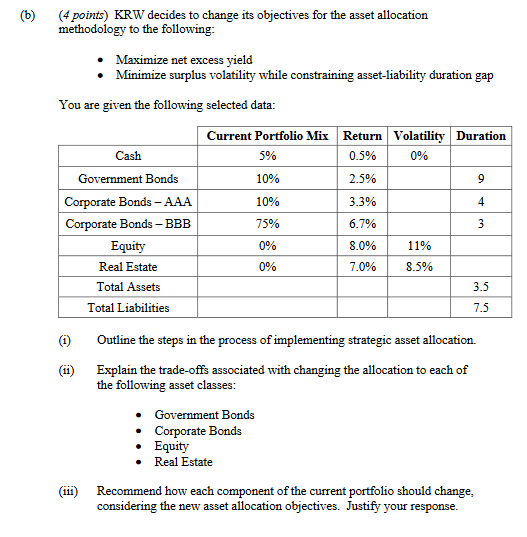

\f\f{Spartans} Energetix's GUI companies all use the same model for evaluating external risks. The model was developed by Energetix and is run independently by each GUI in its Risk Management Department. Refer to section Ell. ll of the lCase Study. You are provided an overview of the External Risk Model fEthrI): I The scenarios used in the model are evaluated and updated every two years i The model engine is evaluated and updated every four years by the department within Energetia that built the model e Model inputs {interest rates: market share: commodity prices, etc.) are updated quarterly 1' Model output is compared to the prior quarter's output to ensure reasonableness The following scenarios are used in the EXRM: The temperature drops ve degrees below the lowest recorded temperature for a period often days within a given year 2 State regulatory change in Colorado that increases GUI expenses by 10% but does not allow for an increase in rates charged 3 Supply of natural gas drops by 20% for a period of one year {a} {2 points} ElevI must include the following types of scenarios in the model: - Global Scenario II MultiEvent Scenario in Synthetic Scenario \f1. (7 points) You are a senior analyst at JMR, an advisory firm specializing in cyber security consulting. You are working on a project for a client who would like to gain a better understanding of methods for modeling cyber risks. (a) (2 points) Your junior analyst, Dan, has identified the following risk metrics: VaR Total Exposure Standard Deviation CTE Average Discuss advantages and disadvantages of using each of these risk metrics. (b ) (2 points) Upon further research, Dan suggests that Extreme Value Theory (EVT) might be a more appropriate solution to model cyber risks. For that proposal, Dan drafts the following presentation slide outlining certain EVT aspects for the client. Extreme Value Theory (EVT): EVT is a tool to help measure tail risk better than VaR. VaR assumes normal distribution Specifically, EVT can help quantify both the maximum of your experience data, and the frequency of values above the maximum. EVT uses historical data; VaR does not. This type of modeling can respond to fat-tailed distributions better than VaR, which is based on a normal distribution, and therefore can be a better predictor of extreme values. EVT accentuates agency issues compared to traditional VaR. EVT is a coherent risk measure unlike VaR. Critique the statements made by Dan.(c) (3 points) The client has asked you to assess the impact of cybersecurity risk on the client's financial performance. You propose to apply the Generalized Pareto Distribution (GPD), which is one of EVT's potential distributions, as the estimation method. Based on observed losses due to past cybersecurity events, Dan prepared the table below for your analysis. Selected information about historical observed losses. Number of losses GPD Parameter Percentile Losses at higher Estimates percentiles k 85th 105 75 150 -0.140 86th 121 70 140 -0.125 87th 202 65 150 -0.097 88th 298 60 130 -0.113 89th 323 55 120 -0.135 90th 366 50 120 -0.135 91st 438 45 120 -0.135 92nd 536 40 120 -0.135 93rd 598 35 120 -0.135 The CDF of the GPD distribution is G(x) =1 - (1 -kx/3)lk (i) Identify the GPD threshold percentile you should use for your analysis. Explain your choice. (ii) Calculate the probability of a total loss greater than 700. Show all work. (iii) Explain how fuzzy logic might be a suitable alternative method to assess cyber risk exposure.2. [12 points} KR'W is a regional annuity carrier based in the US. that specializes in the following products: Ir Fixed deferred annuities It Single premium immediate annuities You are an actuary reporting to KRWs CED. You are provided with the following information regarding ERIE-"s ERJM practice. I. Risk management reports risk metrics including economic capital EEC}, asset liability duration and regulatory riskbased capital ratio ever].r six months to senior management 11. Capital levels are primarily based on regulatory capital requirements and are allocated by product line 111. Current AIM and asset allocation are driven by cash ow matching IV. Sensitivities on liability discount rate and mortality are performed annually by the valuation department HEW is interested in improving its overall rial: management framework. (a) {2 points} Evaluate each of KRW's four current ERl'r-i praeIioec given its current product portfolio. \f(c) (4 points) KRW's management decides to incorporate EC as a metric for its strategic asset allocation process. Its CFO recommends using the following shocks to derive individual EC values: Decrease mortality rates by 10% for all ages and durations . Lower discount rate to 1% flat for all durations . Reduce the lapse rate to 0% for the first 5 durations The CFO suggests that aggregate capital levels would be determined by summing the resultant capital values produced by each shock. (1) Evaluate the appropriateness of the CFO's recommendations for the entire portfolio of KRW's existing products. (ii) Describe key considerations related to the implementation of the following alternative modeling methods: Stochastic Analysis . Sensitivity Analysis (iii) Additionally, KRW is looking into introducing a new traditional life product. Evaluate whether the shocks recommended by the CFO would be appropriate for the portfolio after adding the new product line. (d) (2 points) Recommend how KRW could mitigate financial risks using product design and asset allocation

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance