Question

You are analyzing two call options on the same stock. The stock price is currently at $100 a share; the risk-free interest rate is 0.04.

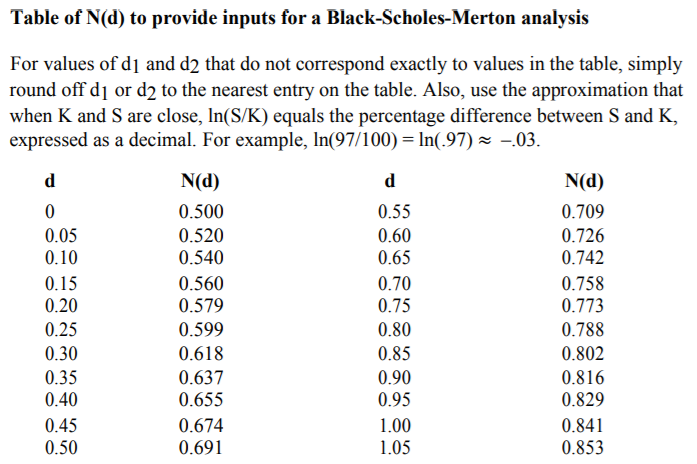

You are analyzing two call options on the same stock. The stock price is currently at $100 a share; the risk-free interest rate is 0.04. The maturity of both options is T = 1 year. Option A has a strike price of K = 100; option B has a strike price of K = 95. For parts of this question you must use the N(d) table at the end of the exam.

You believe the Black-Scholes-Merton equation is the correct option pricing model. Yet despite your confidence that the appropriate volatility of the stock is s = .20, you observe option A selling for $11 and option B selling for $12.

a. Is the implied volatility of Option A more or less than 20%? What about that of option B?

b. Determine a delta-neutral position in the two calls that will exploit their apparent mispricing. Specifically, which option will you buy? Which will you sell? In what ratio? Continue to use s = .20 to compute deltas.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dealing In Traded Options

Authors: Richard Hexton

1st Edition

0131985574, 978-0131985575