Answered step by step

Verified Expert Solution

Question

1 Approved Answer

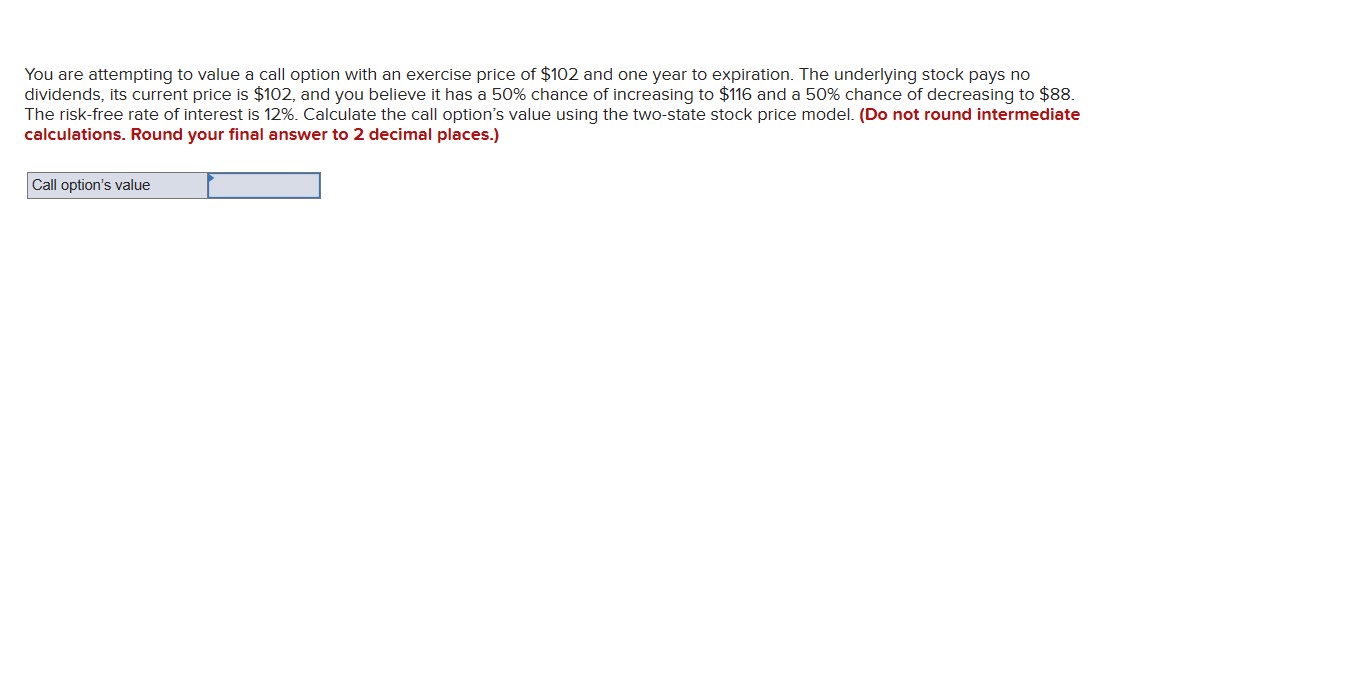

You are attempting to value a call option with an exercise price of $ 1 0 2 and one year to expiration. The underlying stock

You are attempting to value a call option with an exercise price of $ and one year to expiration. The underlying stock pays no

dividends, its current price is $ and you believe it has a chance of increasing to $ and a chance of decreasing to $

The riskfree rate of interest is Calculate the call option's value using the twostate stock price model. Do not round intermediate

calculations. Round your final answer to decimal places.

Call option's value

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Financing Growth

Authors: Kenneth H. Marks, Larry E. Robbins, Gonzalo Fernandez, John P. Funkhouser, D. L. Williams

2nd Edition