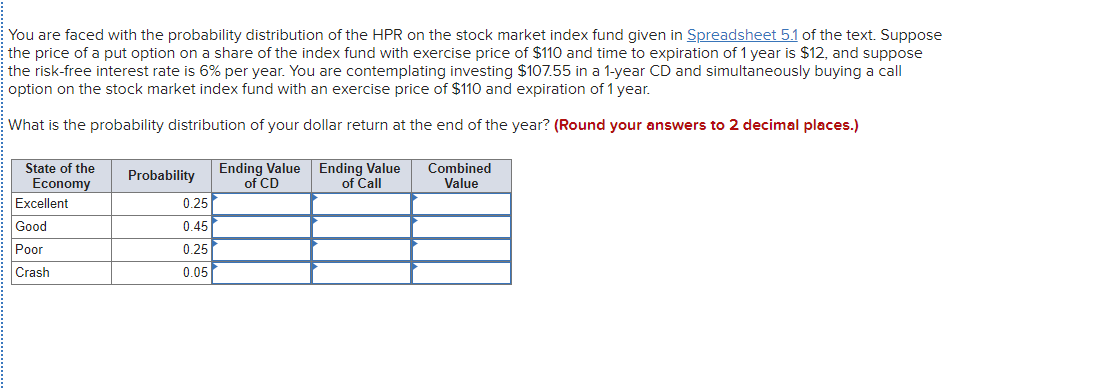

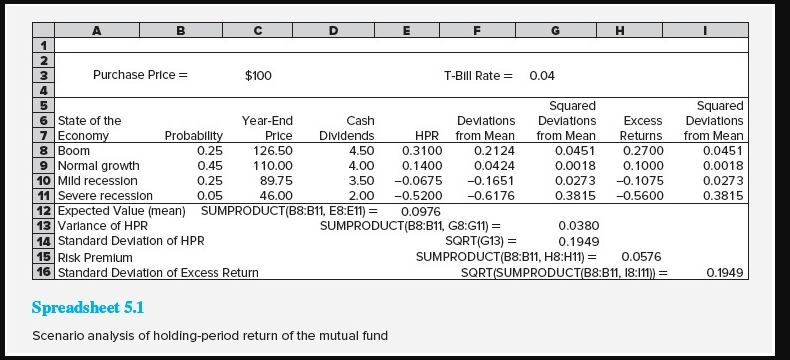

You are faced with the probability distribution of the HPR on the stock market index fund given in Spreadsheet 5.1 of the text. Suppose the price of a put option on a share of the index fund with exercise price of $110 and time to expiration of 1 year is $12, and suppose the risk-free interest rate is 6% per year. You are contemplating investing $107.55 in a 1-year CD and simultaneously buying a call option on the stock market index fund with an exercise price of $110 and expiration of 1 year. What is the probability distribution of your dollar return at the end of the year? (Round your answers to 2 decimal places.) Probability Ending Value of CD Ending Value of Call Combined Value State of the Economy Excellent Good Poor 0.25 0.45 0.25 0.05 Crash B H 1 2 3 Purchase Price = $100 T-Bill Rate = 0.04 4 5 Squared 6 State of the Year-End Cash Deviations Devlations Excess 7 Economy Probability Price Dividends HPR from Mean from Mean Returns 8 Boom 0.25 126.50 4.50 0.3100 0.2124 0.0451 0.2700 9 Normal growth 0.45 110.00 4.00 0.1400 0.0424 0.0018 0.1000 10 Mild recession 0.25 89.75 3.50 -0.0675 -0.1651 0.0273 -0.1075 11 Severe recession 0.05 46.00 2.00 -0.5200 -0.6176 0.3815 -0.5600 12 Expected Value (mean) SUMPRODUCT(B8:B11, E8:E11) = 0.0976 13 Varlance of HPR SUMPRODUCT(B8:B11, G8:G11) = 0.0380 14 Standard Deviation of HPR SQRT(G13) = 0.1949 15 Risk Premlum SUMPRODUCT(B8:B11, H8:H11) = 0.0576 16 Standard Deviation of Excess Return SQRT(SUMPRODUCT(88:B11, 18:111) = Squared Deviations from Mean 0.0451 0.0018 0.0273 0.3815 0.1949 Spreadsheet 5.1 Scenario analysis of holding-period return of the mutual fund You are faced with the probability distribution of the HPR on the stock market index fund given in Spreadsheet 5.1 of the text. Suppose the price of a put option on a share of the index fund with exercise price of $110 and time to expiration of 1 year is $12, and suppose the risk-free interest rate is 6% per year. You are contemplating investing $107.55 in a 1-year CD and simultaneously buying a call option on the stock market index fund with an exercise price of $110 and expiration of 1 year. What is the probability distribution of your dollar return at the end of the year? (Round your answers to 2 decimal places.) Probability Ending Value of CD Ending Value of Call Combined Value State of the Economy Excellent Good Poor 0.25 0.45 0.25 0.05 Crash B H 1 2 3 Purchase Price = $100 T-Bill Rate = 0.04 4 5 Squared 6 State of the Year-End Cash Deviations Devlations Excess 7 Economy Probability Price Dividends HPR from Mean from Mean Returns 8 Boom 0.25 126.50 4.50 0.3100 0.2124 0.0451 0.2700 9 Normal growth 0.45 110.00 4.00 0.1400 0.0424 0.0018 0.1000 10 Mild recession 0.25 89.75 3.50 -0.0675 -0.1651 0.0273 -0.1075 11 Severe recession 0.05 46.00 2.00 -0.5200 -0.6176 0.3815 -0.5600 12 Expected Value (mean) SUMPRODUCT(B8:B11, E8:E11) = 0.0976 13 Varlance of HPR SUMPRODUCT(B8:B11, G8:G11) = 0.0380 14 Standard Deviation of HPR SQRT(G13) = 0.1949 15 Risk Premlum SUMPRODUCT(B8:B11, H8:H11) = 0.0576 16 Standard Deviation of Excess Return SQRT(SUMPRODUCT(88:B11, 18:111) = Squared Deviations from Mean 0.0451 0.0018 0.0273 0.3815 0.1949 Spreadsheet 5.1 Scenario analysis of holding-period return of the mutual fund