Answered step by step

Verified Expert Solution

Question

1 Approved Answer

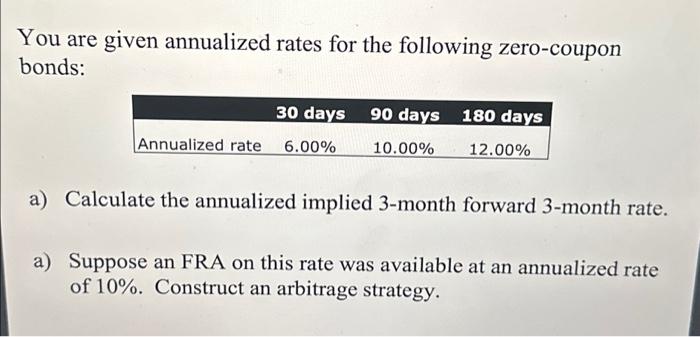

You are given annualized rates for the following zero-coupon bonds: 30 days 90 days 180 days Annualized rate 6.00% 10.00% 12.00% a) Calculate the annualized

You are given annualized rates for the following zero-coupon bonds: 30 days 90 days 180 days Annualized rate 6.00% 10.00% 12.00% a) Calculate the annualized implied 3-month forward 3-month rate. a) Suppose an FRA on this rate was available at an annualized rate of 10%. Construct an arbitrage strategy.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Euro A Challenge And Opportunity For Financial Markets Routledge International Studies In Money And Banking

Authors: Michael Artis , Elizabeth Hennessy, Axel Weber

1st Edition

0415217105, 978-0415217101