Answered step by step

Verified Expert Solution

Question

1 Approved Answer

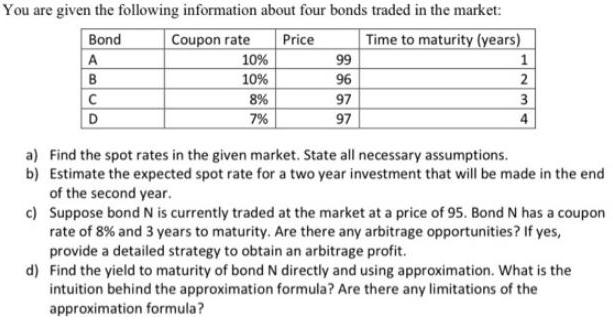

You are given the following information about four bonds traded in the market: Coupon rate Time to maturity (years) Bond A Price 10% 99

You are given the following information about four bonds traded in the market: Coupon rate Time to maturity (years) Bond A Price 10% 99 1 B 10% 96 2 C D 8% 97 3 7% 97 4 a) Find the spot rates in the given market. State all necessary assumptions. b) Estimate the expected spot rate for a two year investment that will be made in the end of the second year. c) Suppose bond N is currently traded at the market at a price of 95. Bond N has a coupon rate of 8% and 3 years to maturity. Are there any arbitrage opportunities? If yes, provide a detailed strategy to obtain an arbitrage profit. d) Find the yield to maturity of bond N directly and using approximation. What is the intuition behind the approximation formula? Are there any limitations of the approximation formula?

Step by Step Solution

★★★★★

3.43 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

A use following formula to find spot rate Present value of bond Coupon11r n Coupon2 1r n Coupon K 1r ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Finance

Authors: Scott Besley, Eugene F. Brigham

6th edition

9781305178045, 1285429648, 1305178041, 978-1285429649