Answered step by step

Verified Expert Solution

Question

1 Approved Answer

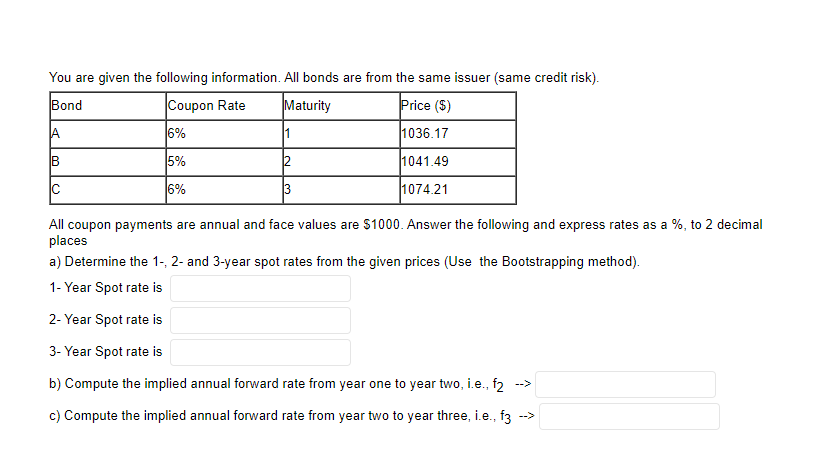

You are given the following information. All bonds are from the same issuer (same credit risk) Bond Coupon Rate Maturity Price (5) 6% 1 1036.17

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Governance And Finance Of Metropolitan Areas In Federal Systems

Authors: Enid Slack, Rupak Chattopadhyay

1st Edition

0199008973, 9780199008971