Answered step by step

Verified Expert Solution

Question

1 Approved Answer

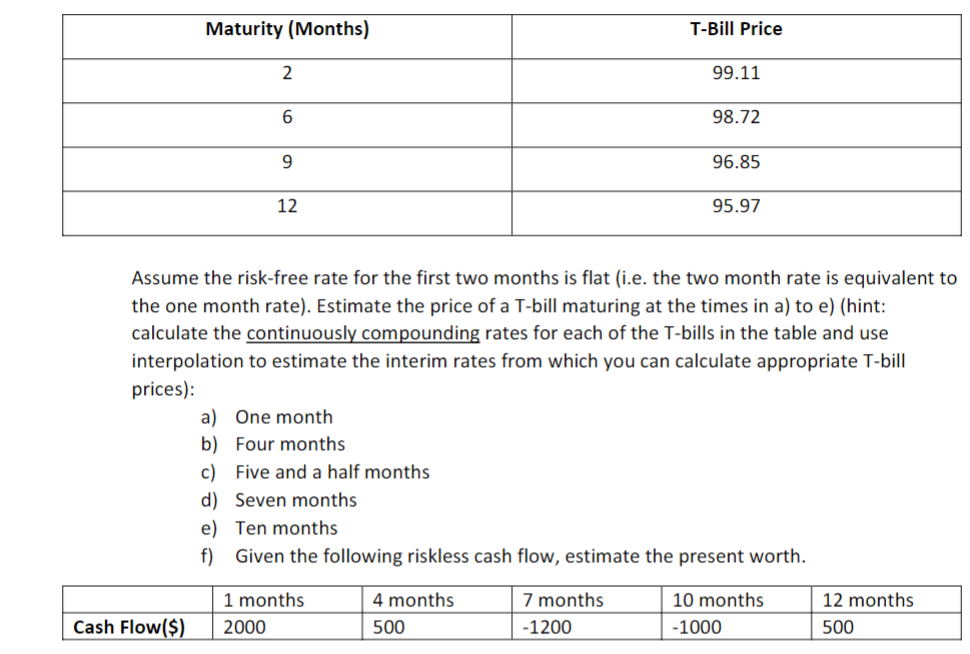

You are given the following price data for T-bills. Assume the risk-free rate for the first two months is flat (i.e. the two month rate

You are given the following price data for T-bills.

Assume the risk-free rate for the first two months is flat (i.e. the two month rate is equivalent to the one month rate). Estimate the price of a T-bill maturing at the times in a) to e) (hint: calculate the continuously compounding rates for each of the T-bills in the table and use interpolation to estimate the interim rates from which you can calculate appropriate T-bill prices): a) One month b) Four months c) Five and a half months d) Seven months e) Ten months f) Given the following riskless cash flow, estimate the present worth

Assume the risk-free rate for the first two months is flat (i.e. the two month rate is equivalent to the one month rate). Estimate the price of a T-bill maturing at the times in a) to e) (hint: calculate the continuously compounding rates for each of the T-bills in the table and use interpolation to estimate the interim rates from which you can calculate appropriate T-bill prices): a) One month b) Four months c) Five and a half months d) Seven months e) Ten months f) Given the following riskless cash flow, estimate the present worth Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Global Finance

Authors: Robert Holton

1st Edition

0415619165, 978-0415619165