Question

You are given the historical annual returns on the common stock of two companies Zeniba and Yubaba. Calculate the average (mean) return and standard deviation

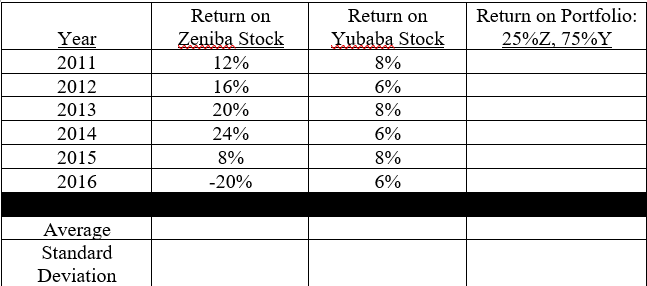

You are given the historical annual returns on the common stock of two companies Zeniba and Yubaba. Calculate the average (mean) return and standard deviation of the returns for each company. Now assume that you create a portfolio consisting of 25% Zeniba and 75% Yubaba. What would the return on the portfolio have been in each year? What would have been the average return on the portfolio over this period? What would have been the standard deviation of the portfolio returns? Would diversification have reduced risk in this case? Why or why not?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Research In Finance

Authors: John W. Kensinger

1st Edition

0857245414, 978-0857245410