Answered step by step

Verified Expert Solution

Question

1 Approved Answer

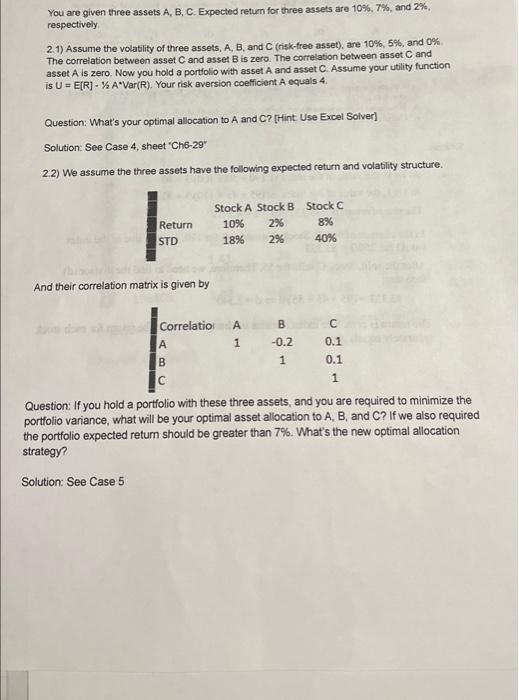

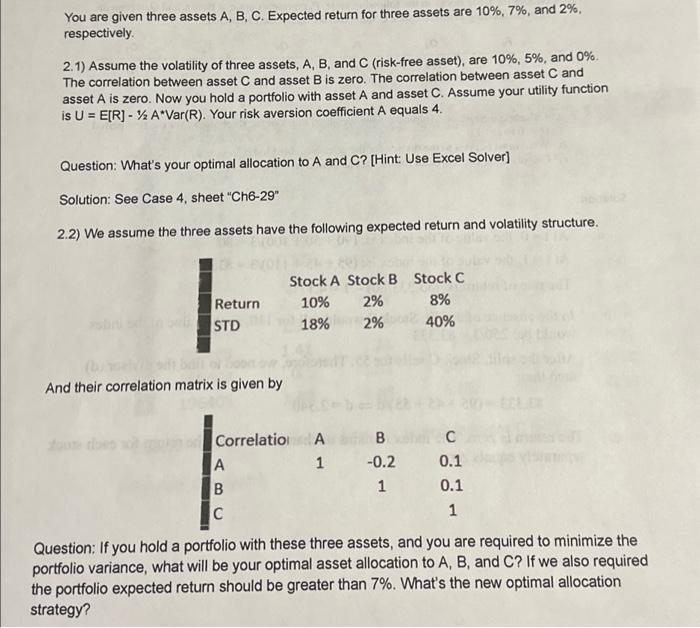

You are given three assets A, B, C. Expected return for three assets are 10%, 7%, and 2%, respectively. 2.1) Assume the volatility of three

You are given three assets A, B, C. Expected return for three assets are 10%, 7%, and 2%, respectively. 2.1) Assume the volatility of three assets, A, B, and C (risk-free asset), are 10%, 5%, and 0%. The correlation between asset C and asset B is zero. The correlation between asset C and asset A is zero. Now you hold a portfolio with asset A and asset C. Assume your utility function is U = E[R] - 12 A*Var(R). Your risk aversion coefficient A equals 4. Question: What's your optimal allocation to A and C? [Hint: Use Excel Solver] Solution: See Case 4, sheet "Ch6-29" 2.2) We assume the three assets have the following expected return and volatility structure. EXODE Return STD (b) toelvibodi bril os boonow And their correlation matrix is given by Solution: See Case 5 Correlatione A A 1 A B Stock A Stock B Stock C 10% 2% 8% 18% 2% 40% C B -0.2 1 C 0.1 0.1 1 Mide pil Question: If you hold a portfolio with these three assets, and you are required to minimize the portfolio variance, what will be your optimal asset allocation to A, B, and C? If we also required the portfolio expected return should be greater than 7%. What's the new optimal allocation strategy?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance A Contemporary Application Of Theory To Policy

Authors: David N Hyman

8th Edition

0324259700, 978-0324259704