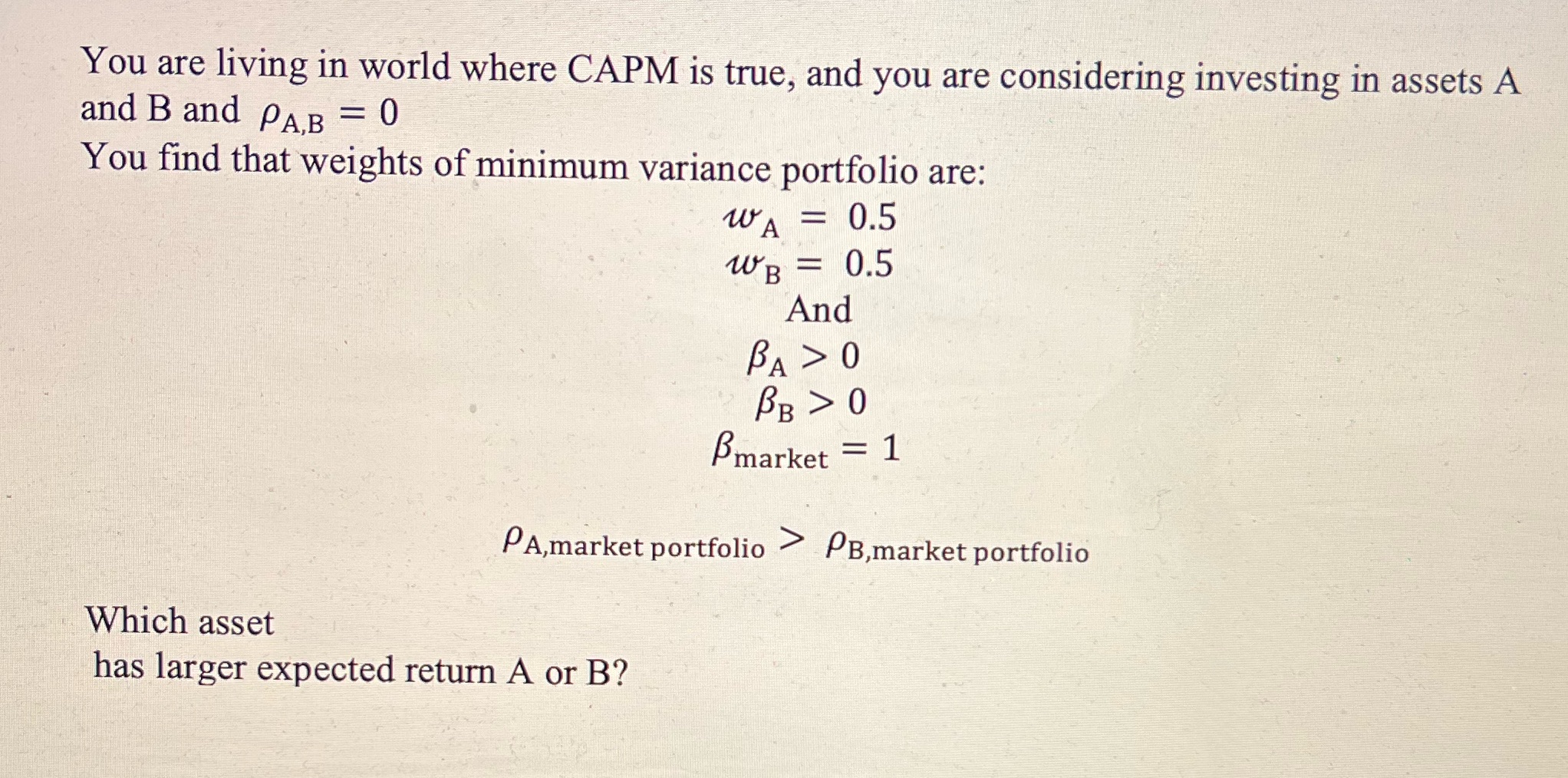

You are living in world where CAPM is true, and you are considering investing in assets A and B and PA,B = 0 You

You are living in world where CAPM is true, and you are considering investing in assets A and B and PA,B = 0 You find that weights of minimum variance portfolio are: WA = 0.5 Which asset WB = 0.5 And BA > 0 BB > 0 market = 1 PA,market portfolio > PB,market portfolio has larger expected return A or B?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

SOLUTION Since the CAPM is true we can use the CAPM equation to find t...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Robert L Sexton

5th Edition

978-1439040249, 1439040249