Answered step by step

Verified Expert Solution

Question

1 Approved Answer

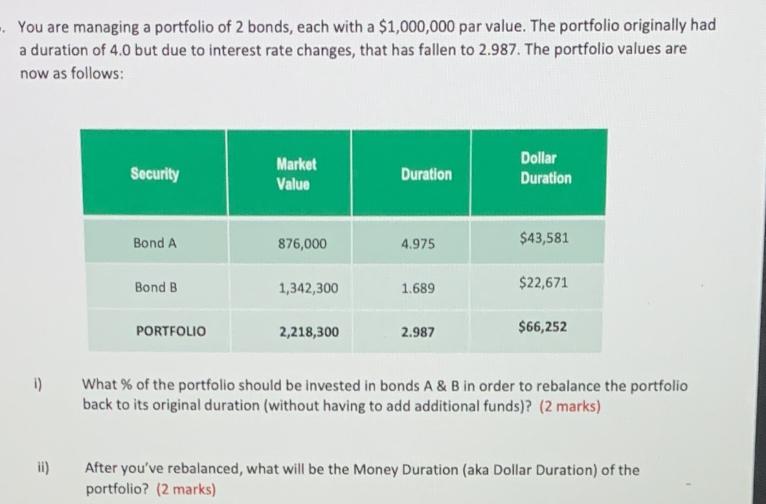

- You are managing a portfolio of 2 bonds, each with a $1,000,000 par value. The portfolio originally had a duration of 4.0 but

- You are managing a portfolio of 2 bonds, each with a $1,000,000 par value. The portfolio originally had a duration of 4.0 but due to interest rate changes, that has fallen to 2.987. The portfolio values are now as follows: 1) ii) Security Bond A Bond B PORTFOLIO Market Value 876,000 1,342,300 2,218,300 Duration 4.975 1.689 2.987 Dollar Duration $43,581 $22,671 $66,252 What % of the portfolio should be invested in bonds A & B in order to rebalance the portfolio back to its original duration (without having to add additional funds)? (2 marks) After you've rebalanced, what will be the Money Duration (aka Dollar Duration) of the portfolio? (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To rebalance the portfolio back to its original duration without adding additional funds we need to ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516