Answered step by step

Verified Expert Solution

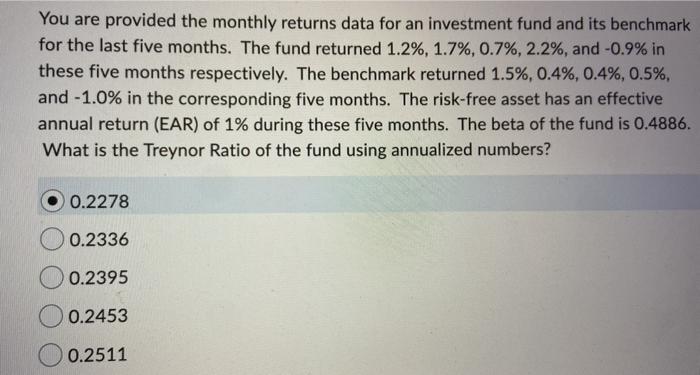

Question

1 Approved Answer

You are provided the monthly returns data for an investment fund and its benchmark for the last five months. The fund returned 1.2%, 1.7%, 0.7%,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Lecture Notes In Introduction To Corporate Finance Volume 1

Authors: Ivan E Brick

1st Edition

9813149892, 9789813149892