Question

You are running the FX trading desk at a large, high-gradeinvestment bank. You have the following rates available to you: Assume that there are no

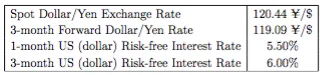

You are running the FX trading desk at a large, high-gradeinvestment bank. You have the following rates available to you:

Assume that there are no transaction costs, and that you caneither buy or sell at these exchange rates. Also, the interestrates above are quoted in annualized, continuously-compounded form,and are the same for borrowing or lending

(a) What must the 3-month Japanese interest rate be, if there isno arbitrage?

(b) Suppose that the annualized, continuously compounded 3-monthyen in- terest rate is 1.0%. What would you do? Provide precisedetails.

Spot Dollar/Yen Exchange Rate. 3-month Forward Dollar/Yen Rate 1-month US (dollar) Risk-free Interest Rate 3-month US (dollar) Risk-free Interest Rate 120.44 /S 119.09 /S 5.50% 6.00%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Part a No Arbitrage Condition In the absence of arbitrage the following equation must hold 1 USD 1month interest rate Spot DollarYen Exchange Rate 3mo...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Accounting

Authors: Paul M. Fischer, William J. Tayler, Rita H. Cheng

11th edition

538480289, 978-0538480284