Answered step by step

Verified Expert Solution

Question

1 Approved Answer

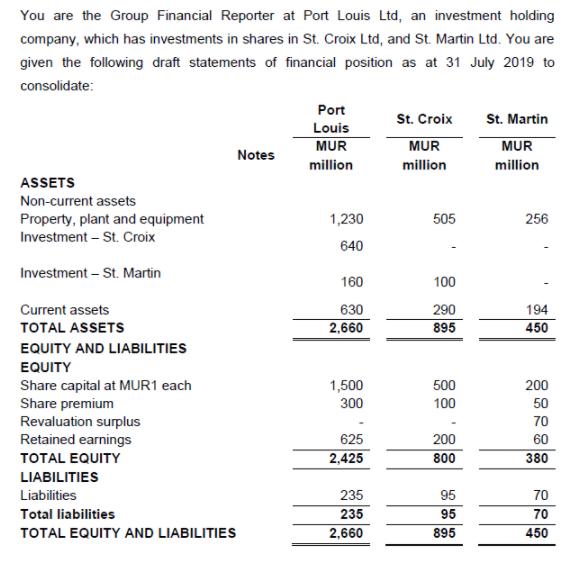

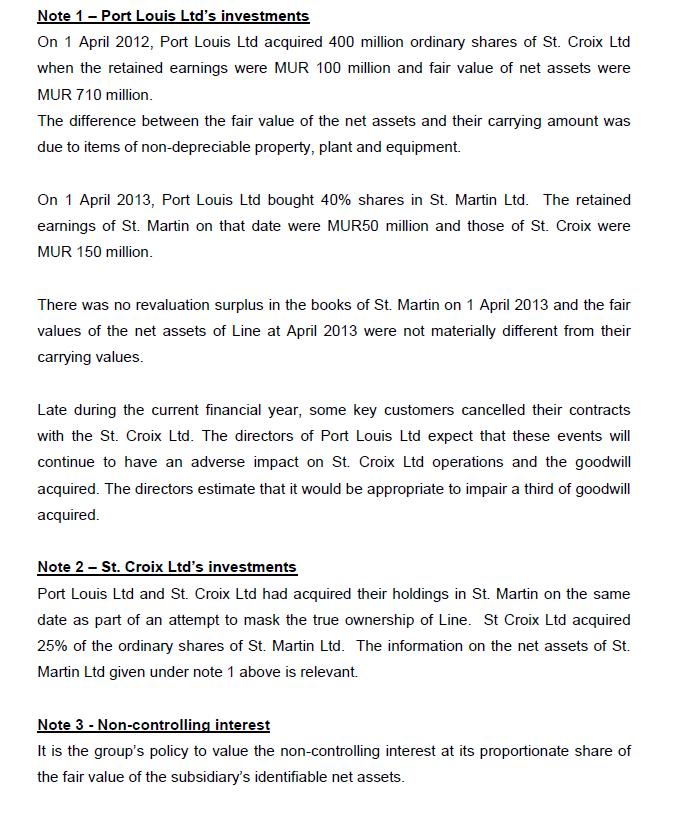

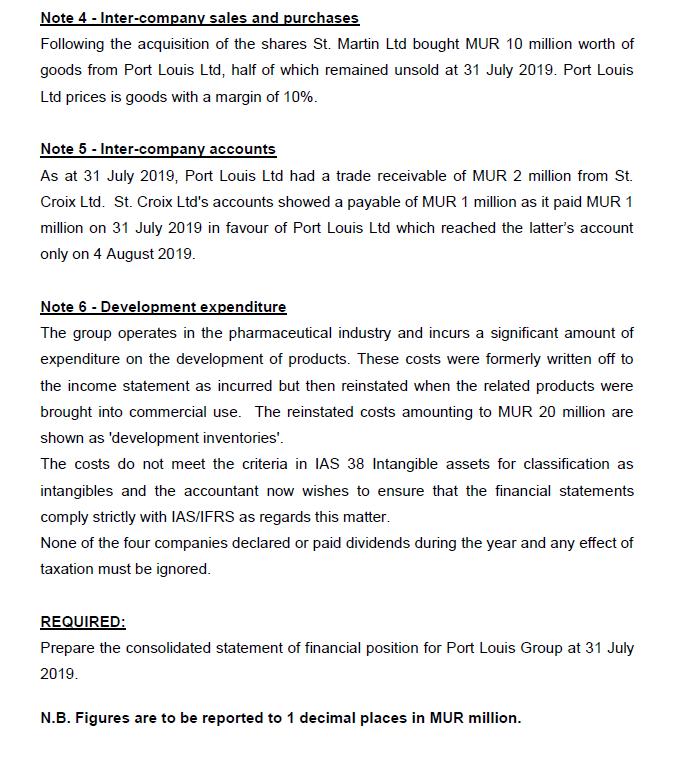

You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and

You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment St. Croix 1,230 505 256 640 Investment St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million. You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment St. Croix 1,230 505 256 640 Investment St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million. You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment St. Croix 1,230 505 256 640 Investment St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million. You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment St. Croix 1,230 505 256 640 Investment St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million.

Step by Step Solution

★★★★★

3.47 Rating (160 Votes )

There are 3 Steps involved in it

Step: 1

PgNo1 Consolidated Statement of financial Position for Post Louis Gsup at 31071...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Management and Cost Accounting

Authors: Colin Drury

8th edition

978-1408041802, 1408041804, 978-1408048566, 1408048566, 978-1408093887