Answered step by step

Verified Expert Solution

Question

1 Approved Answer

You are the manager of a portfolio consisting of three bonds in equal par amounts of $1,000,000 each. The first table below shows the market

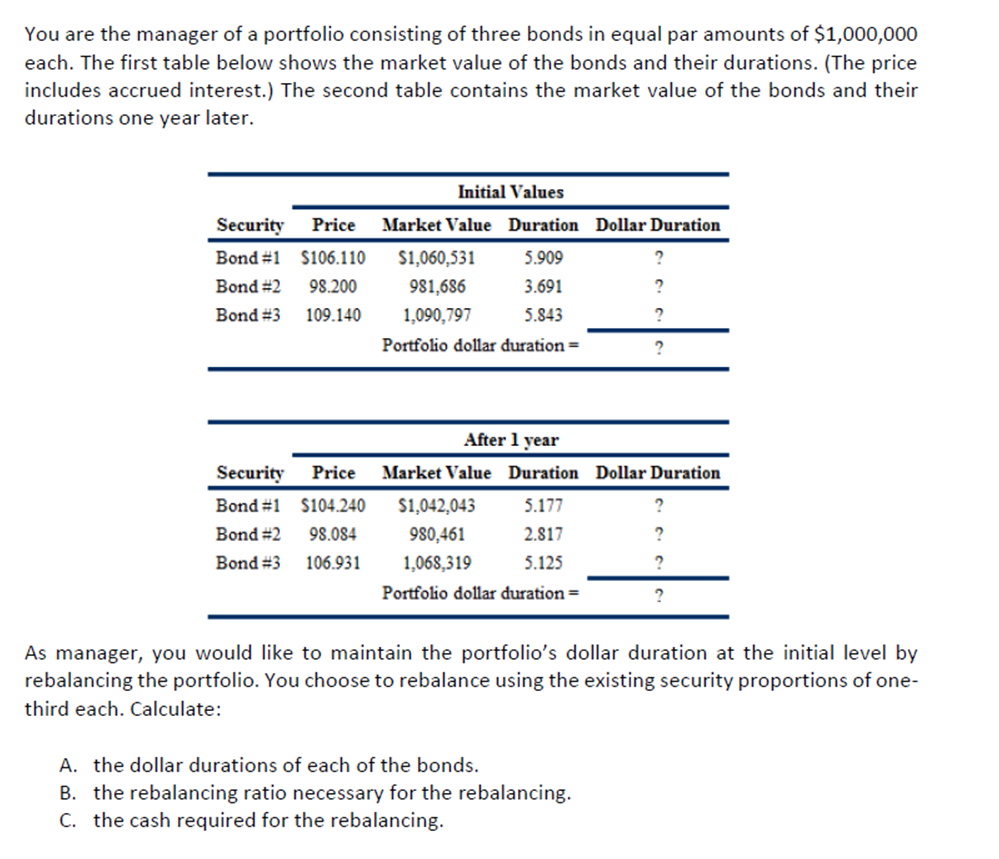

You are the manager of a portfolio consisting of three bonds in equal par amounts of $1,000,000 each. The first table below shows the market value of the bonds and their durations. (The price includes accrued interest.) The second table contains the market value of the bonds and their durations one year later. \begin{tabular}{lcccc} \hline & \multicolumn{4}{c}{ Initial Values } \\ \cline { 2 - 5 } Security & Price & Market Value & Duration & Dollar Duration \\ \hline Bond #1 & $106.110 & $1,060,531 & 5.909 & ? \\ Bond #2 & 98.200 & 981,686 & 3.691 & ? \\ Bond #3 & 109.140 & 1,090,797 & 5.843 & ? \\ \hline & & Portfolio dollar duration = & ? \\ \hline \end{tabular} As manager, you would like to maintain the portfolio's dollar duration at the initial level by rebalancing the portfolio. You choose to rebalance using the existing security proportions of onethird each. Calculate: A. the dollar durations of each of the bonds. B. the rebalancing ratio necessary for the rebalancing. C. the cash required for the rebalancing

You are the manager of a portfolio consisting of three bonds in equal par amounts of $1,000,000 each. The first table below shows the market value of the bonds and their durations. (The price includes accrued interest.) The second table contains the market value of the bonds and their durations one year later. \begin{tabular}{lcccc} \hline & \multicolumn{4}{c}{ Initial Values } \\ \cline { 2 - 5 } Security & Price & Market Value & Duration & Dollar Duration \\ \hline Bond #1 & $106.110 & $1,060,531 & 5.909 & ? \\ Bond #2 & 98.200 & 981,686 & 3.691 & ? \\ Bond #3 & 109.140 & 1,090,797 & 5.843 & ? \\ \hline & & Portfolio dollar duration = & ? \\ \hline \end{tabular} As manager, you would like to maintain the portfolio's dollar duration at the initial level by rebalancing the portfolio. You choose to rebalance using the existing security proportions of onethird each. Calculate: A. the dollar durations of each of the bonds. B. the rebalancing ratio necessary for the rebalancing. C. the cash required for the rebalancing Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Legaltech Book

Authors: Susanne Chishti ,Sophia Adams Bhatti ,Akber Datoo ,Drago Indjic

1st Edition

1119574277, 978-1119574279