Answered step by step

Verified Expert Solution

Question

1 Approved Answer

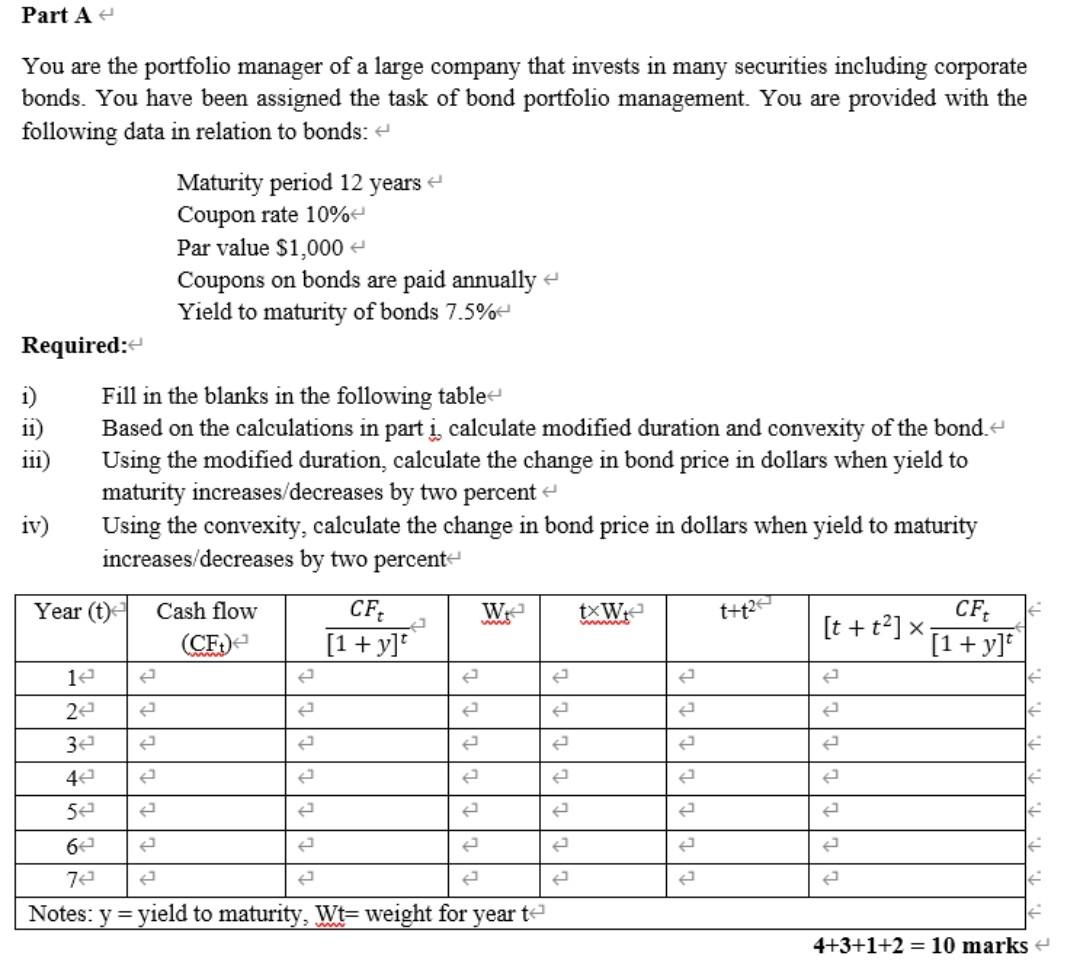

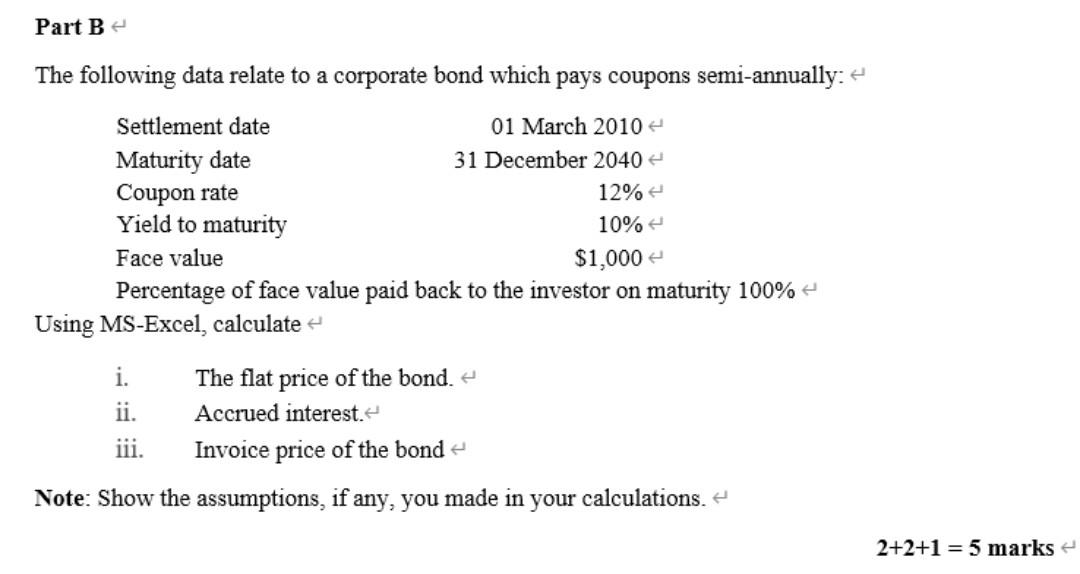

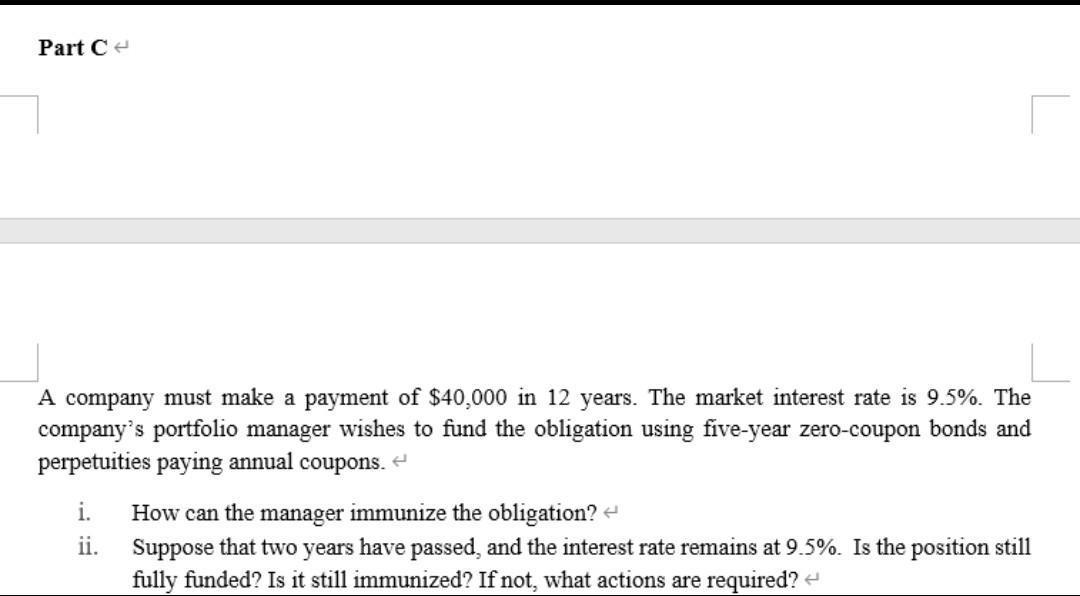

You are the portfolio manager of a large company that invests in many securities including corporate bonds. You have been assigned the task of bond

You are the portfolio manager of a large company that invests in many securities including corporate bonds. You have been assigned the task of bond portfolio management. You are provided with the following data in relation to bonds: Maturity period 12 years Coupon rate 10% Par value $1,000 Coupons on bonds are paid annually Yield to maturity of bonds 7.5% Required: i) Fill in the blanks in the following table ii) Based on the calculations in part i, calculate modified duration and convexity of the bond. iii) Using the modified duration, calculate the change in bond price in dollars when yield to maturity increases/decreases by two percent iv) Using the convexity, calculate the change in bond price in dollars when yield to maturity increases/decreases by two percent Notes: y= yield to maturity, wt= weight tor year t The following data relate to a corporate bond which pays coupons semi-annually: Using MS-Excel, calculate i. The flat price of the bond. ii. Accrued interest. iii. Invoice price of the bond Note: Show the assumptions, if any, you made in your calculations. 2+2+1=5 A company must make a payment of $40,000 in 12 years. The market interest rate is 9.5%. The company's portfolio manager wishes to fund the obligation using five-year zero-coupon bonds and perpetuities paying annual coupons. i. How can the manager immunize the obligation? ii. Suppose that two years have passed, and the interest rate remains at 9.5%. Is the position still fully funded? Is it still immunized? If not, what actions are required? You are the portfolio manager of a large company that invests in many securities including corporate bonds. You have been assigned the task of bond portfolio management. You are provided with the following data in relation to bonds: Maturity period 12 years Coupon rate 10% Par value $1,000 Coupons on bonds are paid annually Yield to maturity of bonds 7.5% Required: i) Fill in the blanks in the following table ii) Based on the calculations in part i, calculate modified duration and convexity of the bond. iii) Using the modified duration, calculate the change in bond price in dollars when yield to maturity increases/decreases by two percent iv) Using the convexity, calculate the change in bond price in dollars when yield to maturity increases/decreases by two percent Notes: y= yield to maturity, wt= weight tor year t The following data relate to a corporate bond which pays coupons semi-annually: Using MS-Excel, calculate i. The flat price of the bond. ii. Accrued interest. iii. Invoice price of the bond Note: Show the assumptions, if any, you made in your calculations. 2+2+1=5 A company must make a payment of $40,000 in 12 years. The market interest rate is 9.5%. The company's portfolio manager wishes to fund the obligation using five-year zero-coupon bonds and perpetuities paying annual coupons. i. How can the manager immunize the obligation? ii. Suppose that two years have passed, and the interest rate remains at 9.5%. Is the position still fully funded? Is it still immunized? If not, what actions are required

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Critical Handbook Of Money Laundering Policy Analysis And Myths

Authors: Petrus C. Van Duyne, Jackie H. Harvey, Liliya Y. Gelemerova

1st Edition

1137523972, 978-1137523976