Answered step by step

Verified Expert Solution

Question

1 Approved Answer

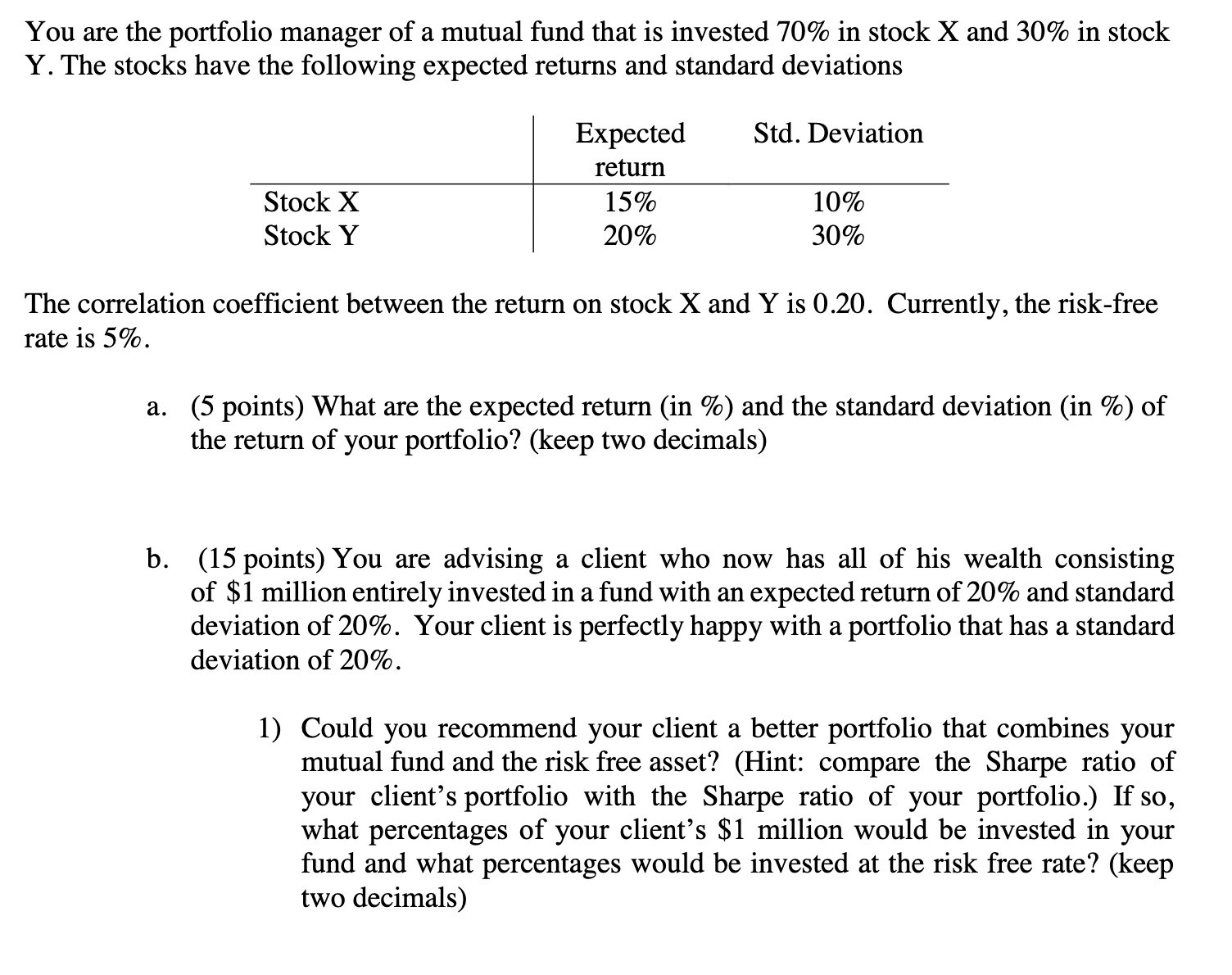

You are the portfolio manager of a mutual fund that is invested 70% in stock X and 30% in stock Y. The stocks have the

You are the portfolio manager of a mutual fund that is invested 70% in stock X and 30% in stock Y. The stocks have the following expected returns and standard deviations The correlation coefficient between the return on stock X and Y is 0.20 . Currently, the risk-free rate is 5%. a. (5 points) What are the expected return (in \%) and the standard deviation (in \%) of the return of your portfolio? (keep two decimals) b. (15 points) You are advising a client who now has all of his wealth consisting of $1 million entirely invested in a fund with an expected return of 20% and standard deviation of 20%. Your client is perfectly happy with a portfolio that has a standard deviation of 20%. 1) Could you recommend your client a better portfolio that combines your mutual fund and the risk free asset? (Hint: compare the Sharpe ratio of your client's portfolio with the Sharpe ratio of your portfolio.) If so, what percentages of your client's $1 million would be invested in your

You are the portfolio manager of a mutual fund that is invested 70% in stock X and 30% in stock Y. The stocks have the following expected returns and standard deviations The correlation coefficient between the return on stock X and Y is 0.20 . Currently, the risk-free rate is 5%. a. (5 points) What are the expected return (in \%) and the standard deviation (in \%) of the return of your portfolio? (keep two decimals) b. (15 points) You are advising a client who now has all of his wealth consisting of $1 million entirely invested in a fund with an expected return of 20% and standard deviation of 20%. Your client is perfectly happy with a portfolio that has a standard deviation of 20%. 1) Could you recommend your client a better portfolio that combines your mutual fund and the risk free asset? (Hint: compare the Sharpe ratio of your client's portfolio with the Sharpe ratio of your portfolio.) If so, what percentages of your client's $1 million would be invested in your Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Passive Income Stacking Handbook How To Reach Financial Freedom Faster Regardless Of Your Age Or Situation

Authors: Mark Walters

1st Edition

0578530171, 978-0578530178