Answered step by step

Verified Expert Solution

Question

1 Approved Answer

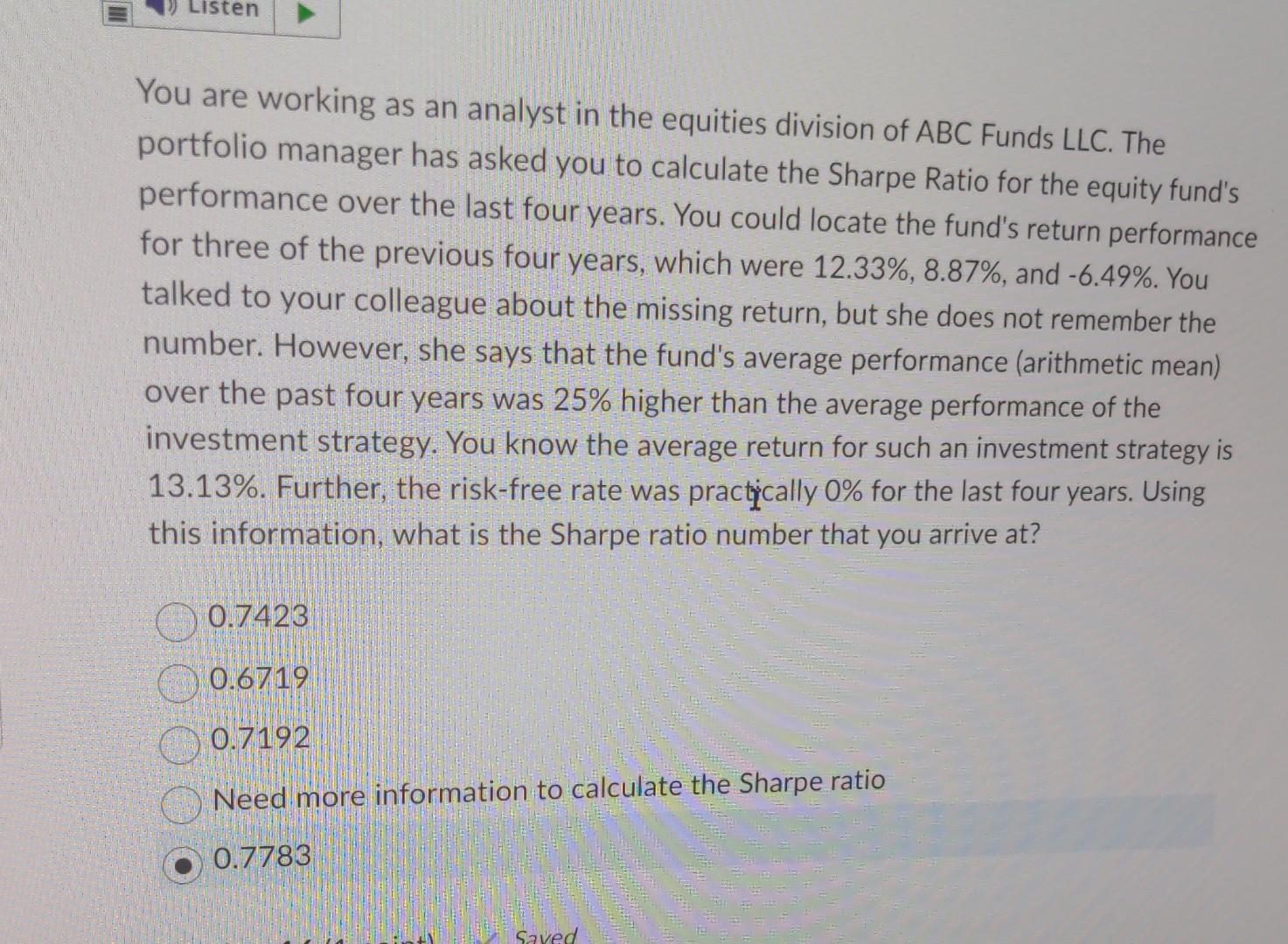

You are working as an analyst in the equities division of ABC Funds LLC. The portfolio manager has asked you to calculate the Sharpe Ratio

You are working as an analyst in the equities division of ABC Funds LLC. The portfolio manager has asked you to calculate the Sharpe Ratio for the equity fund's performance over the last four years. You could locate the fund's return performance for three of the previous four years, which were 12.33%,8.87%, and 6.49%. You talked to your colleague about the missing return, but she does not remember the number. However, she says that the fund's average performance (arithmetic mean) over the past four years was 25% higher than the average performance of the investment strategy. You know the average return for such an investment strategy is 13.13%. Further, the risk-free rate was practically 0% for the last four years. Using this information, what is the Sharpe ratio number that you arrive at? \begin{tabular}{|l|} \hline 0.7423 \\ \hline 0.6719 \\ \hline 0.7192 \\ \hline \end{tabular} Need more information to calculate the Sharpe ratio 0.7783

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financing Large Projects Using Project Finance Techniques And Practices

Authors: Fouzul Khan, Robert Parra

1st Edition

9780131016347