Answered step by step

Verified Expert Solution

Question

1 Approved Answer

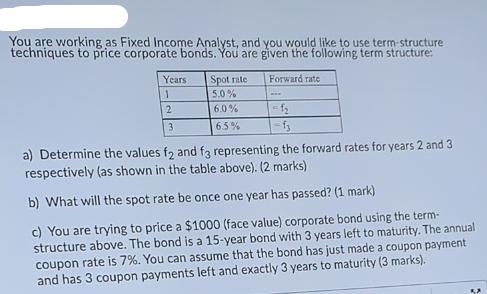

You are working as Fixed Income Analyst, and you would like to use term-structure techniques to price corporate bonds. You are given the following

You are working as Fixed Income Analyst, and you would like to use term-structure techniques to price corporate bonds. You are given the following term structure: Years 1 2 3 Spot rate 5.0% 6.0% 6.5% Forward rate www =1 fj a) Determine the values f2 and f3 representing the forward rates for years 2 and 3 respectively (as shown in the table above). (2 marks) b) What will the spot rate be once one year has passed? (1 mark) c) You are trying to price a $1000 (face value) corporate bond using the term- structure above. The bond is a 15-year bond with 3 years left to maturity. The annual coupon rate is 7%. You can assume that the bond has just made a coupon payment and has 3 coupon payments left and exactly 3 years to maturity (3 marks).

Step by Step Solution

★★★★★

3.46 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

a To determine the forward rates we can use the relationship between spot rates and forward rates 1 s22 1 s11 f2 1 s33 1 s11 f21 f3 Given the spot rat...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

15th edition

1337671002, 978-1337395250