Answered step by step

Verified Expert Solution

Question

1 Approved Answer

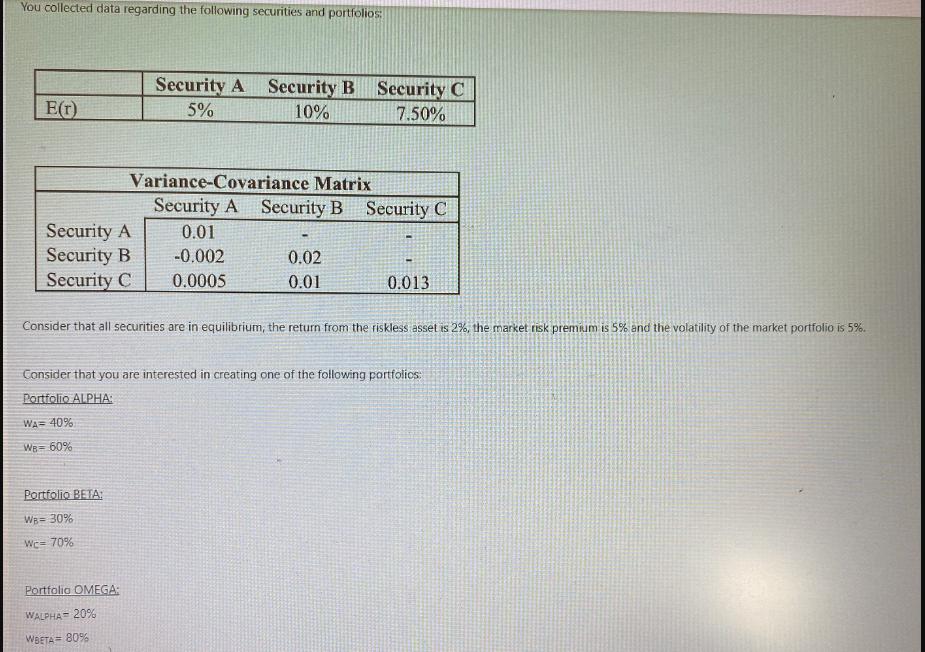

You collected data regarding the following securities and portfolios: E(r) Security Security B Security C WA= 40% WB= 60% Security A Security B Security

You collected data regarding the following securities and portfolios: E(r) Security Security B Security C WA= 40% WB= 60% Security A Security B Security C 5% 10% 7.50% Variance-Covariance Matrix Security A Security B Security C 0.01 -0.002 0.0005 Portfolio BETA: WB = 30% Wc-70% Consider that all securities are in equilibrium, the return from the riskless asset is 2%, the market risk premium is 5% and the volatility of the market portfolio is 5%. Portfolio OMEGA: WALPHA= 20% WBETA= 80% 0.02 0.01 Consider that you are interested in creating one of the following portfolics: Portfolio ALPHA: 0.013

Step by Step Solution

★★★★★

3.48 Rating (165 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the expected return and standard deviation of each portfolio we can use the following f...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516