You, CPA, work as a consultant on various engagements. Your client, Over The Edge Ltd. (OTE), has grown from a small custom snowboard manufacturer

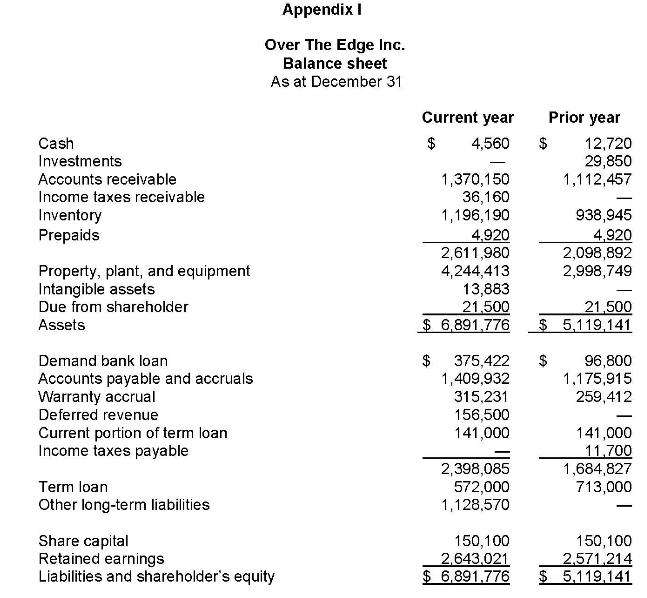

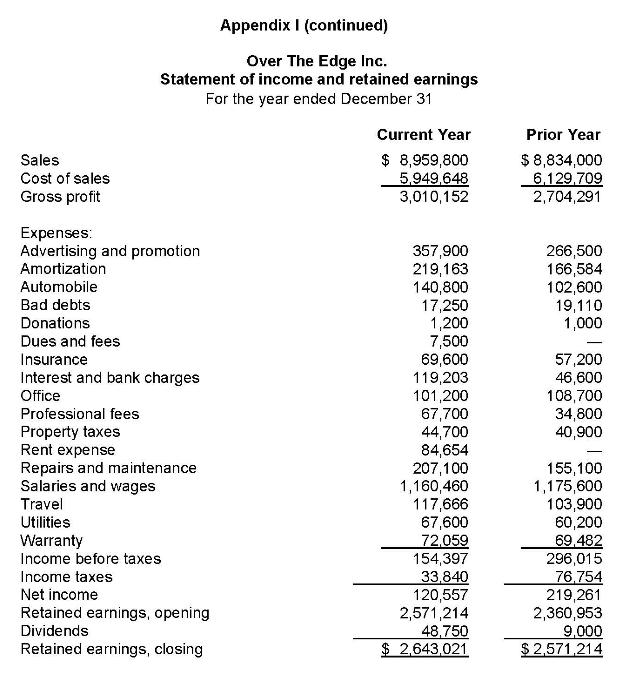

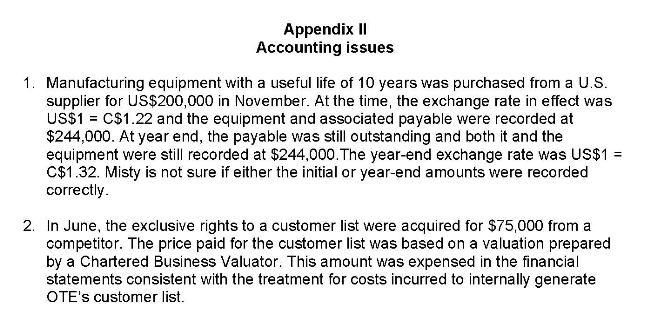

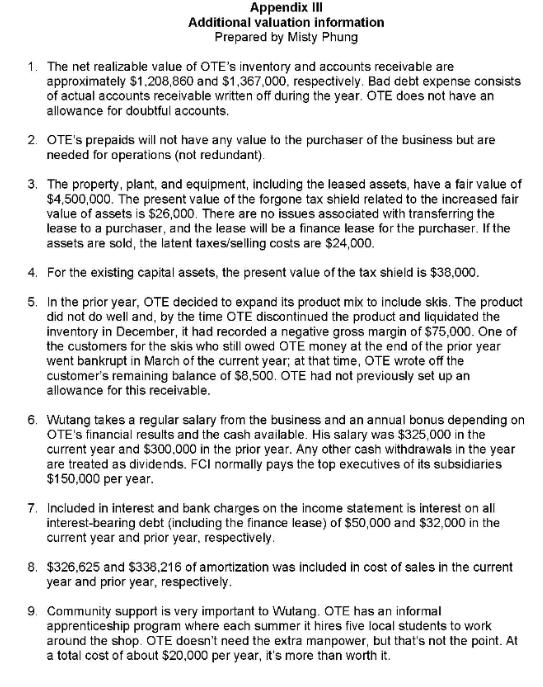

You, CPA, work as a consultant on various engagements. Your client, Over The Edge Ltd. (OTE), has grown from a small custom snowboard manufacturer servicing the local market to a multinational success. Recently, OTE's snowboards were used by a gold medallist in the Winter Olympics! It's Monday morning, and you are meeting with the company's owner and sole shareholder, Wutang Pan. Also in attendance is Misty Phung, OTE's VP of finance. Wutang tells you: Fun Consolidators Inc. (FCI), a public company and the largest competitor in the industry, has expressed an interest in acquiring OTE. It has made three similar acquisitions in the past two years- two of which were closed and manufacturing was moved to the United States. The other is operated consistent with pre-acquisition. I hadn't been thinking about selling the company, but things have progressed very quickly with FCI. I'm getting older and I have worked hard for a long time building the business. While my children are still quite young, I don't anticipate that any of them will become involved with the business. So, this might be the right time to sell. As you know, the snowboard industry is cyclical, but it is at its peak right now. I'm very proud to say that OTE has been named one of the "10 Best Small Businesses to Work for" for the past three years. The award is based on financial performance, customer surveys, and employee satisfaction. I have a very dedicated and loyal staff. Many of the staff members are like family to me. In the past seven years, we have not had to lay off any of our employees. Misty then jumps in: OTE operates in a stable industry and the results for the company were relatively consistent over the past five years. The December 31 year-end statements are provided in Appendix I. There are a few outstanding accounting issues that may impact them, which I have included in Appendix II. I also put together a memo for you with some information on non-recurring or unusual items incurred by OTE. I will email it to you (Appendix III). Our weighted average capitalization rate is 12%. In this case, I want you to assume that the present value of the tax shield associated with capital reinvestments is about 10% of the amount spent, which is projected to be $100,000 per year. As FCI is public, it would not be able to claim a small business deduction for OTE. I would say that FCI could expect to pay corporate tax at the rate of 30%. Wutang concludes: I'd like to make sure I understand what my company is worth before the offer is received. Task #1 Prepare an analysis of the accounting issues described in Appendix II. OTE reports its financial statements in accordance with IFRS. Task #2 a) In Excel, prepare a capitalized cash flow valuation for OTE, using the information provided in the appendixes. b) In Excel, prepare an adjusted net asset valuation for OTE using the financial statements and information attached. Unless otherwise noted, assume that the carrying value of the assets approximates fair market value. c) In Word, prepare a memo comparing the two valuation approaches. Summarize your results from the calculations and explain why there is a difference in the two valuations. Appendix I Over The Edge Inc. Balance sheet As at December 31 Current year Prior year Cash 12,720 29,850 1,112,457 $ 4,560 $ Investments Accounts receivable 1,370,150 36,160 1,196,190 4,920 2,611,980 4,244,413 13,883 21,500 $ 6,891,776 Income taxes receivable Inventory Prepaids 938,945 4,920 2,098,892 2,998,749 Property, plant, and equipment Intangible assets Due from shareholder 21,500 $ 5,119,141 Assets Demand bank loan $ 375,422 $ Accounts payable and accruals Warranty accrual Deferred revenue 1,409,932 315,231 156,500 96,800 1,175,915 259,412 - Current portion of term loan Income taxes payable 141,000 141,000 11,700 1,684,827 713,000 2,398,085 572,000 1,128,570 Term loan Other long-term liabilities - Share capital Retained earnings Liabilities and shareholder's equity 150,100 2,643,021 $ 6,891.776 150,100 2,571.214 $ 5,119,141 Appendix I (continued) Over The Edge Inc. Statement of income and retained earnings For the year ended December 31 Current Year Prior Year Sales Cost of sales $ 8,959,800 5,949,648 3,010,152 $8,834,000 6,129,709 2,704,291 Gross profit Expenses: Advertising and promotion Amortization 357,900 219,163 140,800 17,250 1,200 7,500 69,600 119,203 101,200 67,700 44,700 84,654 207,100 1,160,460 117,666 67,600 72.059 154,397 33,840 120,557 2,571,214 48,750 $ 2,643,021 266,500 166,584 102,600 19,110 1,000 Automobile Bad debts Donations Dues and fees 57,200 46,600 108,700 34,800 40,900 Insurance Interest and bank charges Office Professional fees Property taxes Rent expense Repairs and maintenance Salaries and wages 155,100 1,175,600 103,900 60,200 69.482 296,015 76,754 219,261 2,360,953 9,000 $2,571,214 Travel Utilities Warranty Income before taxes Income taxes Net income Retained earnings, opening Dividends Retained earnings, closing Appendix II Accounting issues 1. Manufacturing equipment with a useful life of 10 years was purchased from a U.S. supplier for US$200,000 in November. At the time, the exchange rate in effect was US$1 = C$1.22 and the equipment and associated payable were recorded at $244,000. At year end, the payable was still outstanding and both it and the equipment were still recorded at $244,000.The year-end exchange rate was US$1 = C$1.32. Misty is not sure if either the initial or year-end amounts were recorded correctly. %3D 2. In June, the exclusive rights to a customer list were acquired for $75,000 from a competitor. The price paid for the customer list was based on a valuation prepared by a Chartered Business Valuator. This amount was expensed in the financial statements consistent with the treatment for costs incurred to internally generate OTE's customer list. Appendix II Additional valuation information Prepared by Misty Phung 1. The net realizable value of OTE's inventory and accounts receivable are approximately $1.208,860 and $1,367,000, respectively. Bad debt expense consists of actual accounts receivable written off during the year. OTE does not have an allowance for doubtful accounts. 2. OTE's prepaids will not have any value to the purchaser of the business but are needed for operations (not redundant). 3. The property, plant, and equipment, including the leased assets, have a fair value of $4,500,000. The present value of the forgone tax shield related to the increased fair value of assets is $26,000. There are no issues associated with transferring the lease to a purchaser, and the lease will be a finance lease for the purchaser. If the assets are sold, the latent taxes/selling costs are $24,000. 4. For the existing capital assets, the present value of the tax shield is $38,000. 5. In the prior year, OTE decided to expand its product mix to include skis. The product did not do well and, by the time OTE discontinued the product and liquidated the inventory in December, it had recorded a negative gross margin of $75,000. One of the customers for the skis who still owed OTE money at the end of the prior year went bankrupt in March of the current year; at that time, OTE wrote off the customer's remaining balance of $8,500. OTE had not previously set up an allowance for this receivable. 6. Wutang takes a regular salary from the business and an annual bonus depending on OTE's financial results and the cash available. His salary was $325,000 in the current year and $300,000 in the prior year. Any other cash withdrawals in the year are treated as dividends. FCI normally pays the top executives of its subsidiaries $150,000 per year. 7. Included in interest and bank charges on the income statement is interest on all interest-bearing debt (including the finance lease) of $50,000 and $32,000 in the current year and prior year, respectively. 8. $326,625 and $338.216 of amortization was included in cost of sales in the current year and prior year, respectively. 9. Community support is very important to Wutang. OTE has an informal apprenticeship program where each summer it hires five local students to work around the shop. OTE doesn't need the extra manpower, but that's not the point. At a total cost of about $20,000 per year, it's more than worth it.

Step by Step Solution

3.40 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: James M. Wahlen, Jefferson P. Jones, Donald Pagach

3rd edition

9781337909402, 978-1337788281