Answered step by step

Verified Expert Solution

Question

1 Approved Answer

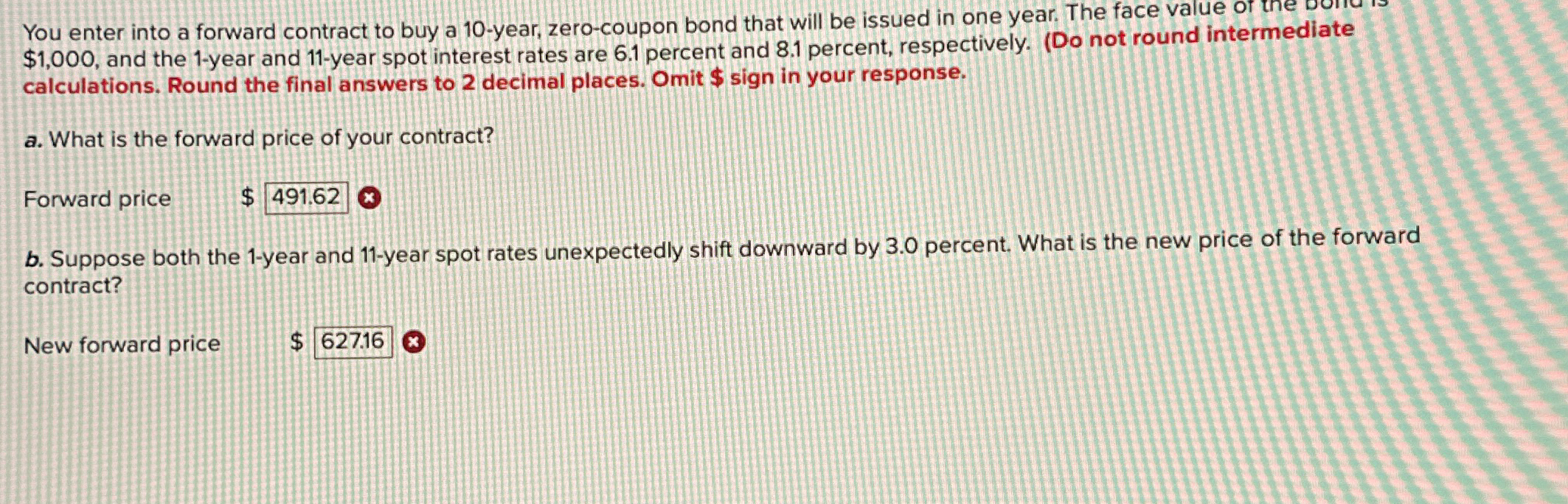

You enter into a forward contract to buy a 1 0 - year, zero - coupon bond that will be issued in one year. The

You enter into a forward contract to buy a year, zerocoupon bond that will be issued in one year. The face value of the $ and the year and year spot interest rates are percent and percent, respectively. Do not round intermediate calculations. Round the final answers to decimal places. Omit $ sign in your response.

a What is the forward price of your contract?

Forward price

$

b Suppose both the year and year spot rates unexpectedly shift downward by percent. What is the new price of the forward contract?

New forward price

$

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

7 Money Rules For Life How To Take Control Of Your Financial Future

Authors: Mary Hunt

1st Edition

0800722531, 978-0800722531