Answered step by step

Verified Expert Solution

Question

1 Approved Answer

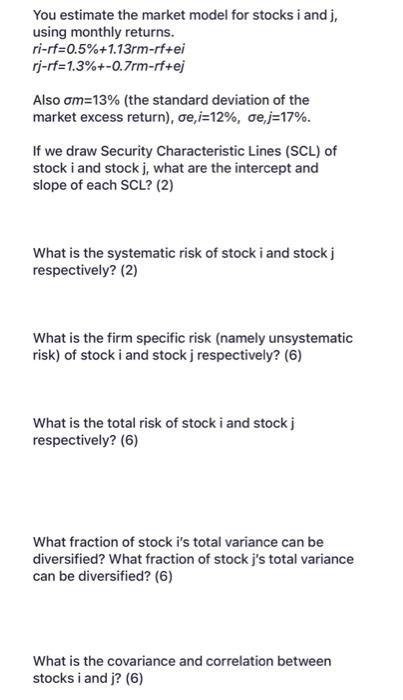

You estimate the market model for stocks i and j, using monthly returns. rirf=0.5%+1.13rmrf+ei rjrf=1.3%+0.7rmrf+ej Also m=13% (the standard deviation of the market excess return),

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

AS Accounting For AQA

Authors: David Cox,Michael Fardon

2nd Edition

1905777140, 978-1905777143