Answered step by step

Verified Expert Solution

Question

1 Approved Answer

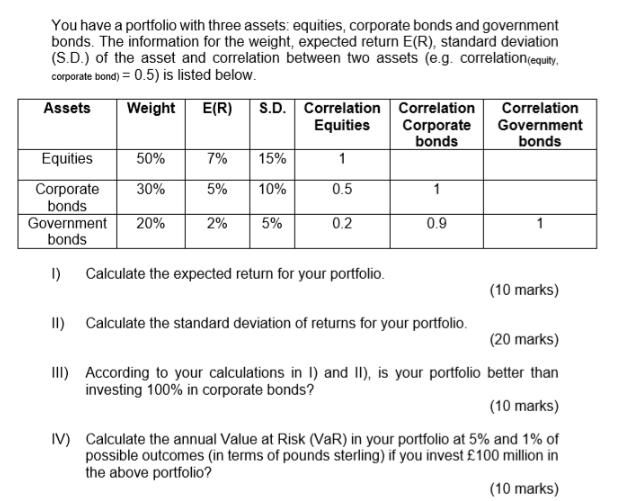

You have a portfolio with three assets: equities, corporate bonds and government bonds. The information for the weight, expected return E(R), standard deviation (S.D.)

You have a portfolio with three assets: equities, corporate bonds and government bonds. The information for the weight, expected return E(R), standard deviation (S.D.) of the asset and correlation between two assets (e.g. correlation(equity. corporate bond) = 0.5) is listed below. Assets Weight E(R) S.D. Correlation Correlation Equities Corporate bonds 1 0.5 Equities 50% Corporate 30% bonds Government 20% bonds 1) II) 7% 15% 5% 10% 2% 5% 0.2 Calculate the expected return for your portfolio. 1 0.9 Calculate the standard deviation of returns for your portfolio. Correlation Government bonds (10 marks) (20 marks) III) According to your calculations in I) and II), is your portfolio better than investing 100% in corporate bonds? (10 marks) IV) Calculate the annual Value at Risk (VaR) in your portfolio at 5% and 1% of possible outcomes (in terms of pounds sterling) if you invest 100 million in the above portfolio? (10 marks)

Step by Step Solution

★★★★★

3.46 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

Expected return of portfolio is weight average of each ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Corporate Finance

Authors: Berk, DeMarzo, Harford

2nd edition

132148234, 978-0132148238