Answered step by step

Verified Expert Solution

Question

1 Approved Answer

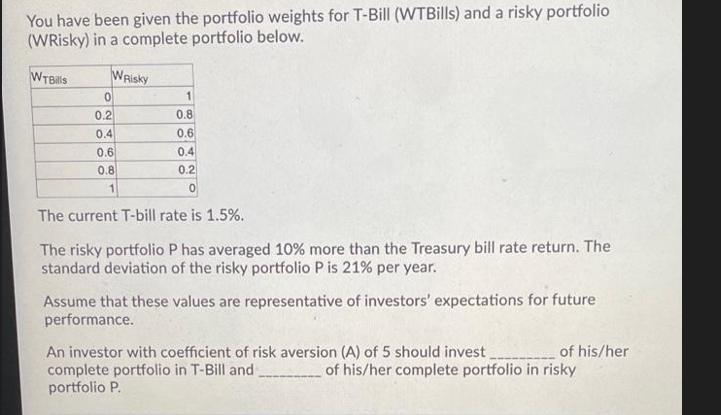

You have been given the portfolio weights for T-Bill (WTBills) and a risky portfolio (WRisky) in a complete portfolio below. WTBills Whisky 1 0.8

You have been given the portfolio weights for T-Bill (WTBills) and a risky portfolio (WRisky) in a complete portfolio below. WTBills Whisky 1 0.8 0.6 0.4 0.2 0 The current T-bill rate is 1.5%. 0 0.2 0.4 0.6 0.8 The risky portfolio P has averaged 10% more than the Treasury bill rate return. The standard deviation of the risky portfolio P is 21% per year. Assume that these values are representative of investors' expectations for future performance. An investor with coefficient of risk aversion (A) of 5 should invest complete portfolio in T-Bill and portfolio P. of his/her of his/her complete portfolio in risky

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Okay lets solve this stepbystep Tbill rate 15 Expected return of risk...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing The Art and Science of Assurance Engagements

Authors: Alvin A. Arens, Randal J. Elder, Mark S. Beasley, Joanne C. Jones

13th Canadian edition

133405508, 978-0133405507